Chiến lược Slow RSI quá mua quá bán

Tổng quan

Chiến lược RSI chậm quá mua quá bán mở ra cơ hội giao dịch mới bằng cách kéo dài chu kỳ xem lại của RSI, giảm độ biến động của đường RSI. Chiến lược này cũng có thể áp dụng cho các chỉ báo kỹ thuật khác như MACD.

Nguyên lý chiến lược

Ý tưởng cốt lõi của chiến lược là kéo dài độ dài chu kỳ xem lại của RSI, mặc định là 500 chu kỳ, sau đó làm mượt đường RSI bằng SMA với chu kỳ mặc định là 250. Điều này giúp giảm đáng kể độ biến động của đường RSI, làm chậm tốc độ phản ứng của RSI, từ đó tạo ra các cơ hội giao dịch mới.

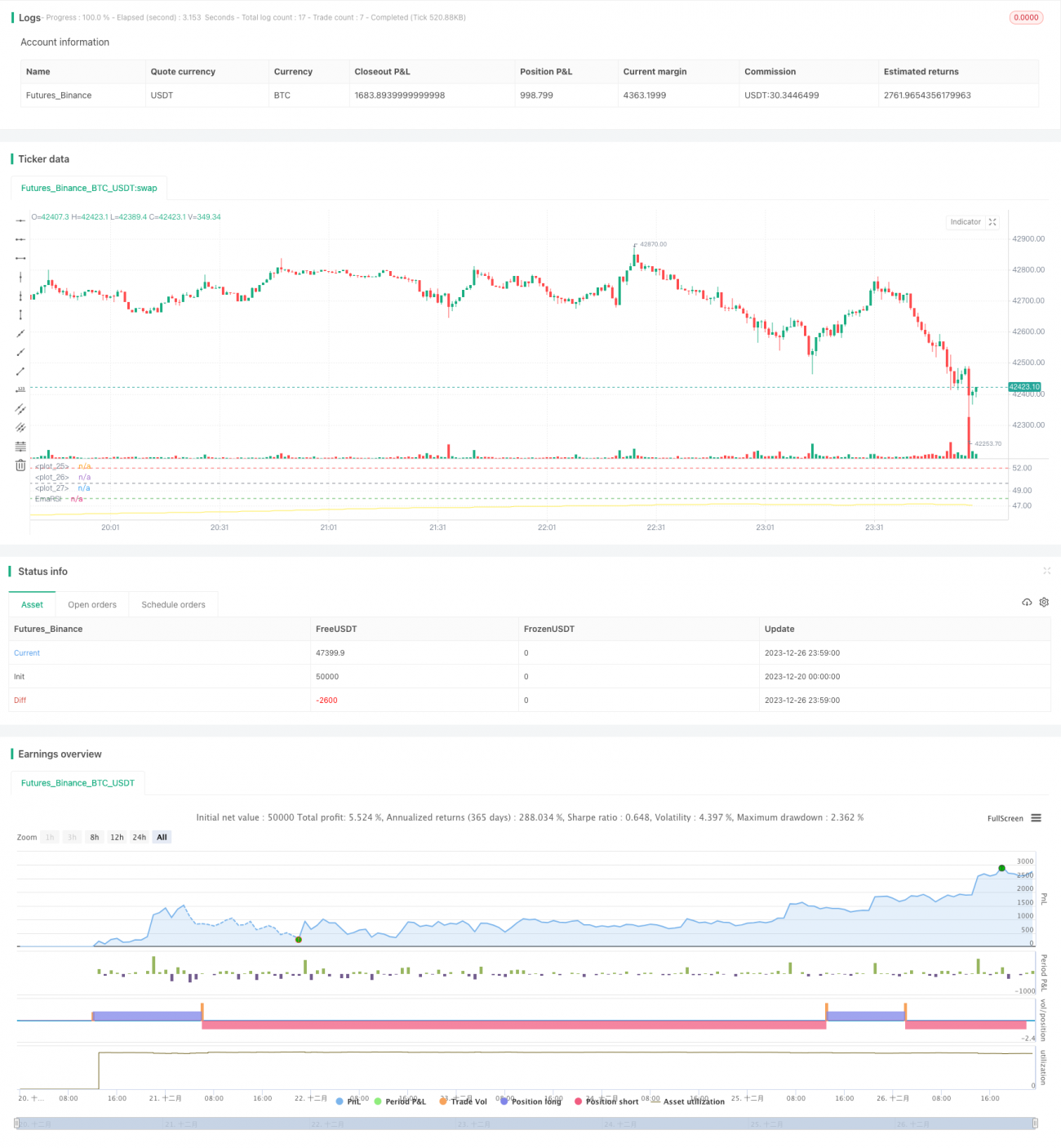

Chu kỳ xem lại quá dài làm suy yếu độ biến động của đường RSI, do đó tiêu chuẩn xác định quá mua quá bán cũng cần được điều chỉnh. Chiến lược đặt ngưỡng quá mua tùy chỉnh là 52 và ngưỡng quá bán là 48. Khi RSI có trọng số vượt lên trên ngưỡng quá bán, tín hiệu mở vị thế mua được phát ra; khi phá vỡ xuống dưới ngưỡng quá mua, tín hiệu mở vị thế bán được phát ra.

Ưu điểm của chiến lược

- Tính sáng tạo cao, mở ra hướng tư duy giao dịch mới nhờ kéo dài chu kỳ

- Giảm đáng kể tín hiệu nhiễu, tăng tính ổn định

- Có thể tùy chỉnh ngưỡng quá mua quá bán, thích ứng với các thị trường khác nhau

- Có thể nhồi lệnh tăng dần, nâng cao tỷ suất lợi nhuận

Rủi ro của chiến lược

- Chu kỳ quá dài có thể bỏ lỡ cơ hội ngắn hạn

- Cần kiên nhẫn chờ đợi cơ hội vào lệnh

- Thiết lập ngưỡng quá mua quá bán không phù hợp có thể làm tăng thua lỗ

- Có rủi ro bị đánh chênh lệch

Giải pháp:

- Rút ngắn chu kỳ một cách phù hợp, tăng tần suất giao dịch

- Áp dụng phương pháp vào lệnh theo từng đợt để phân tán rủi ro

- Tối ưu hóa tham số ngưỡng để phù hợp với các môi trường thị trường khác nhau

- Đặt điểm cắt lỗ để tránh thua lỗ lớn

Hướng tối ưu hóa chiến lược

- Tối ưu hóa tham số RSI để tìm tổ hợp chu kỳ tốt nhất

- Kiểm tra các tham số chu kỳ làm mượt SMA khác nhau

- Tối ưu hóa tham số quá mua quá bán để khớp với các thị trường khác nhau

- Thêm chiến lược cắt lỗ để kiểm soát thua lỗ từng lệnh

Kết luận

Chiến lược RSI chậm quá mua quá bán đã thành công mở ra hướng tư duy giao dịch mới bằng cách kéo dài chu kỳ và sử dụng đường trung bình để hạn chế biến động. Với việc tối ưu hóa tham số và kiểm soát rủi ro đầy đủ, chiến lược này có khả năng đạt được lợi nhuận vượt trội ổn định và hiệu quả. Nhìn chung, chiến lược có tính sáng tạo cao và giá trị ứng dụng lớn.

/*backtest

start: 2023-12-20 00:00:00

end: 2023-12-27 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Wilder was a very influential man when it comes to TA. However, I'm one to always try to think outside the box.

// While Wilder recommended that the RSI be used only with a 14 bar lookback period, I on the other hand think there is a lot to learn from RSI if one simply slows down the lookback period

// Same applies for MACD.- 1