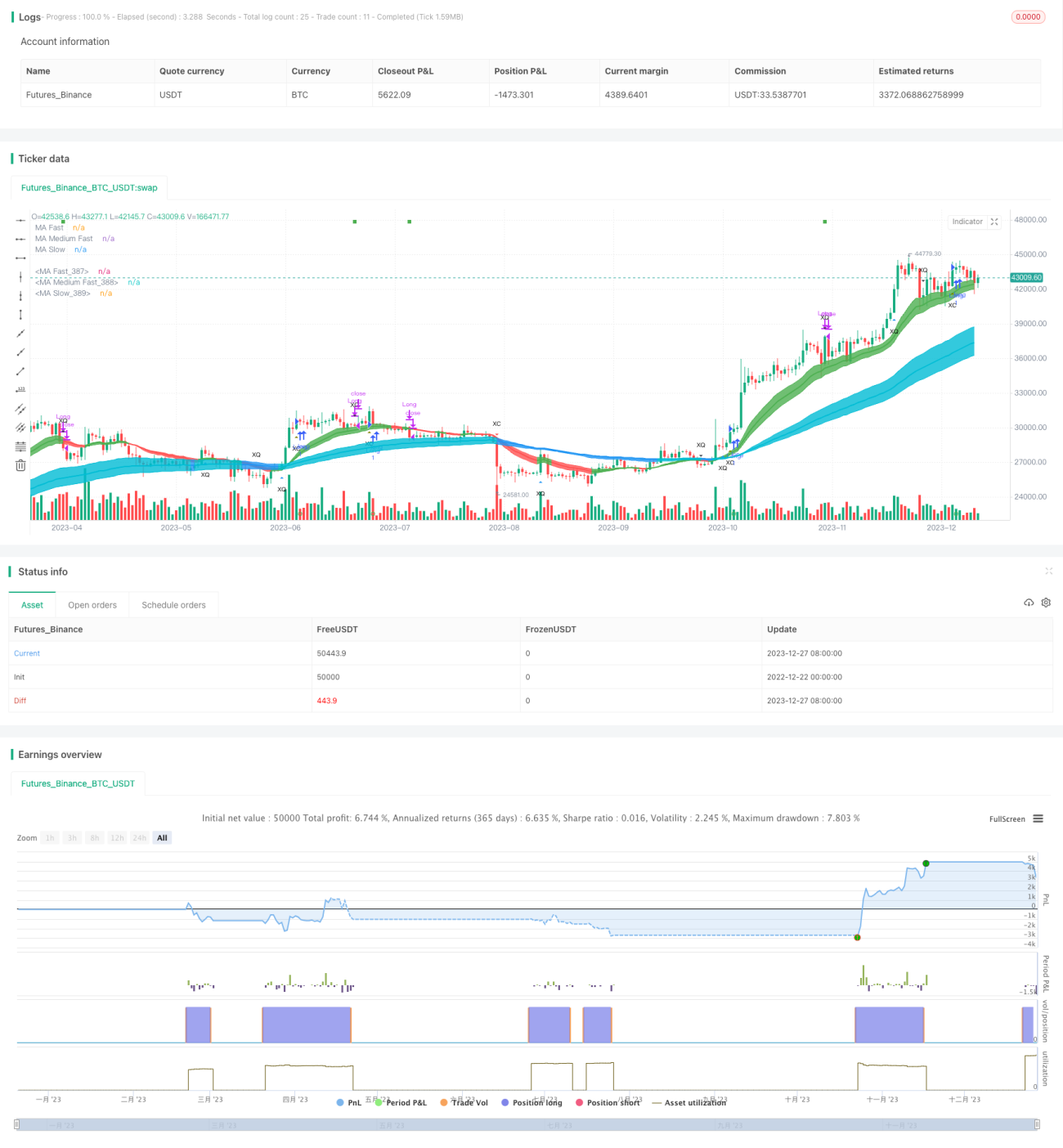

Chiến lược theo dõi xu hướng dựa trên QQE và MA

Tổng quan

Chiến lược này là một chiến lược giao dịch theo xu hướng dựa trên chỉ báo QQE (Định lượng định tính ước tính) và đường trung bình động. Nó xác định hướng xu hướng thông qua sự giao nhau của chỉ báo QQE nhanh và bộ lọc hướng của đường trung bình động, tạo ra tín hiệu mua và bán.

Chiến lược này có thể chọn ba loại giao nhau của chỉ báo QQE để xác định tín hiệu: (1) Đường RSI làm mịn giao nhau với trục 0; (2) Đường RSI làm mịn giao nhau với đường QQE nhanh; (3) Đường RSI làm mịn thoát khỏi kênh ngưỡng RSI. Mặc định sử dụng loại giao nhau thứ ba để mở lệnh và loại giao nhau thứ hai để đóng lệnh.

Tín hiệu mua và bán có thể chọn có cần lọc thêm bằng đường trung bình động hay không: giá đóng cửa phải cao hơn (thấp hơn) đường trung bình động nhanh, và đường trung bình động nhanh phải cao hơn (thấp hơn) đường trung bình động chậm thì mới phát sinh tín hiệu.

Chiến lược này phù hợp để sử dụng làm chế độ tín hiệu đối sánh tín hiệu cho giao dịch tự động hóa.

Nguyên lý

Chỉ báo cốt lõi của chiến lược là QQE, công thức tính như sau:

Wilders_Period = RSILen * 2 - 1

Rsi = rsi(close,RSILen)

RSIndex = ema(Rsi, SF)

AtrRsi = abs(RSIndex - RSIndex[1])

MaAtrRsi = ema(AtrRsi, Wilders_Period)

DeltaFastAtrRsi = ema(MaAtrRsi,Wilders_Period) * QQEfactor

newshortband = RSIndex + DeltaFastAtrRsi

newlongband = RSIndex - DeltaFastAtrRsi

Trong đó RSILen là chu kỳ độ dài của RSI, SF là hệ số làm mịn của RSI. Về bản chất, QQE là một RSI đã được làm mịn. Nó tính toán dải trên và dải dưới thông qua một ATR nhanh. Khi giá vượt quá dải, nó được xác định là cơ hội mua hoặc bán.

Chiến lược này sử dụng ba loại giao nhau của QQE để nhận diện tín hiệu giao dịch:

- Đường RSI làm mịn giao nhau với trục 0 (XZ)

QQEzlong = RSIndex >= 50 ? QQEzlong + 1 : 0

QQEzshort = RSIndex < 50 ? QQEzshort + 1 : 0

- Đường RSI làm mịn giao nhau với chỉ báo QQE nhanh (XQ), giống như một tín hiệu dao động sớm

QQExlong = FastAtrRsiTL < RSIndex ? QQExlong + 1 : 0

QQExshort = FastAtrRsiTL > RSIndex ? QQExshort + 1 : 0

- Đường RSI làm mịn thoát khỏi kênh ngưỡng (XC), giống như một tín hiệu dao động xác nhận

threshhold = 10

QQEclong = RSIndex > (50 + threshhold) ? QQEclong + 1 : 0

QQEcshort = RSIndex < (50 - threshhold) ? QQEcshort + 1 : 0

Có thể chọn một hoặc nhiều trong ba loại giao nhau trên để nhận diện tín hiệu mua/bán và tín hiệu đóng lệnh.

Tín hiệu mua và bán có thể chọn có cần lọc thêm bằng đường trung bình động hay không:

// Điều kiện lọc

QQEflong = close > ma_medium và

ma_medium > ma_slow và

ma_fast > ma_medium

QQEfshort = close < ma_medium và

ma_medium < ma_slow và

ma_fast < ma_medium

Điều này giúp tránh các tín hiệu sai trong thị trường đi ngang.

Chiến lược này phù hợp cho giao dịch tự động, sử dụng các giao nhau QQE khác nhau để mở và đóng lệnh:

Tín hiệu mở lệnh = XC hoặc XQ hoặc XZ

Tín hiệu đóng lệnh = XQ hoặc XZ

Ưu điểm

Chiến lược này có các ưu điểm sau:

-

Sử dụng chỉ báo QQE để xác định xu hướng và tín hiệu giao nhau, bản thân QQE có đặc tính làm mịn khử nhiễu, có thể giảm tín hiệu sai.

-

Kết hợp bộ lọc đường trung bình động, có thể tránh thêm các tín hiệu sai trong thị trường đi ngang, nâng cao chất lượng tín hiệu.

-

Có thể chọn các giao nhau QQE khác nhau để mở và đóng lệnh, thực hiện giao dịch tự động.

-

Chỉ báo RSI làm mịn do có độ trễ nên tín hiệu mua bán sẽ không bị vẽ lại.

-

Có thể tối ưu hóa trên các khung thời gian khác nhau để tìm ra tổ hợp tham số tốt nhất.

Rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

-

Khi xu hướng đảo chiều, có thể phát sinh tín hiệu sai, cần đặt stop loss để kiểm soát rủi ro.

-

Việc thiết lập tham số không phù hợp cũng ảnh hưởng đến hiệu suất của chiến lược, cần kiểm tra và tối ưu hóa nhiều lần để tìm ra tham số tốt nhất.

-

Các loại tài sản và khung thời gian khác nhau cần được kiểm tra và tối ưu hóa riêng.

-

Giao dịch cơ giới có rủi ro sụt giảm và thua lỗ liên tiếp, cần quản lý vốn.

Các giải pháp tương ứng như sau:

-

Đặt stop loss, thoát lệnh khi lỗ đạt đến một mức nhất định.

-

Kiểm tra chi tiết các tổ hợp tham số khác nhau để tìm ra tham số tốt nhất.

-

Điều chỉnh tham số dựa trên đặc điểm của tài sản và khung thời gian.

-

Quản lý vốn tốt, vào lệnh theo từng đợt, kiểm soát khối lượng mỗi lệnh.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa theo các hướng sau:

-

Tối ưu hóa tham số QQE, bao gồm độ dài RSI, độ dài làm mịn RSI, độ dài ATR nhanh, v.v., tìm ra tổ hợp tham số tối ưu.

-

Tối ưu hóa tham số đường trung bình động, điều chỉnh chu kỳ, loại, v.v., để phù hợp nhất với chỉ báo QQE.

-

Kiểm tra các giao nhau QQE khác nhau để mở và đóng lệnh, tìm ra tổ hợp ổn định nhất.

-

Tinh chỉnh tham số theo từng loại tài sản và khung thời gian giao dịch. Giao dịch trong ngày có thể rút ngắn chu kỳ để tăng hiệu suất.

-

Thêm cơ chế stop loss. Dừng lỗ khi thua lỗ đạt đến một tỷ lệ nhất định.

-

Giảm quy mô vị thế phù hợp, kiểm tra các phương pháp quản lý vị thế khác nhau.

Tổng kết

Chiến lược này tích hợp chỉ báo QQE để xác định xu hướng và tín hiệu giao nhau, cùng với bộ lọc đường trung bình động để tạo ra tín hiệu giao dịch. Trong giao dịch thực tế, có thể điều chỉnh tham số để tối ưu hóa chất lượng tín hiệu; kết hợp với quản lý vốn chặt chẽ để kiểm soát rủi ro. Chiến lược này phù hợp để sử dụng làm chế độ tín hiệu đối sánh tín hiệu cho giao dịch tự động, cũng có thể hỗ trợ ra quyết định trong giao dịch tùy ý. Thông qua tối ưu hóa tham số và quy tắc, có thể thích ứng với nhiều môi trường thị trường hơn.

- 1