Chiến lược giao dịch Siêu xu hướng BankNifty

Tổng quan

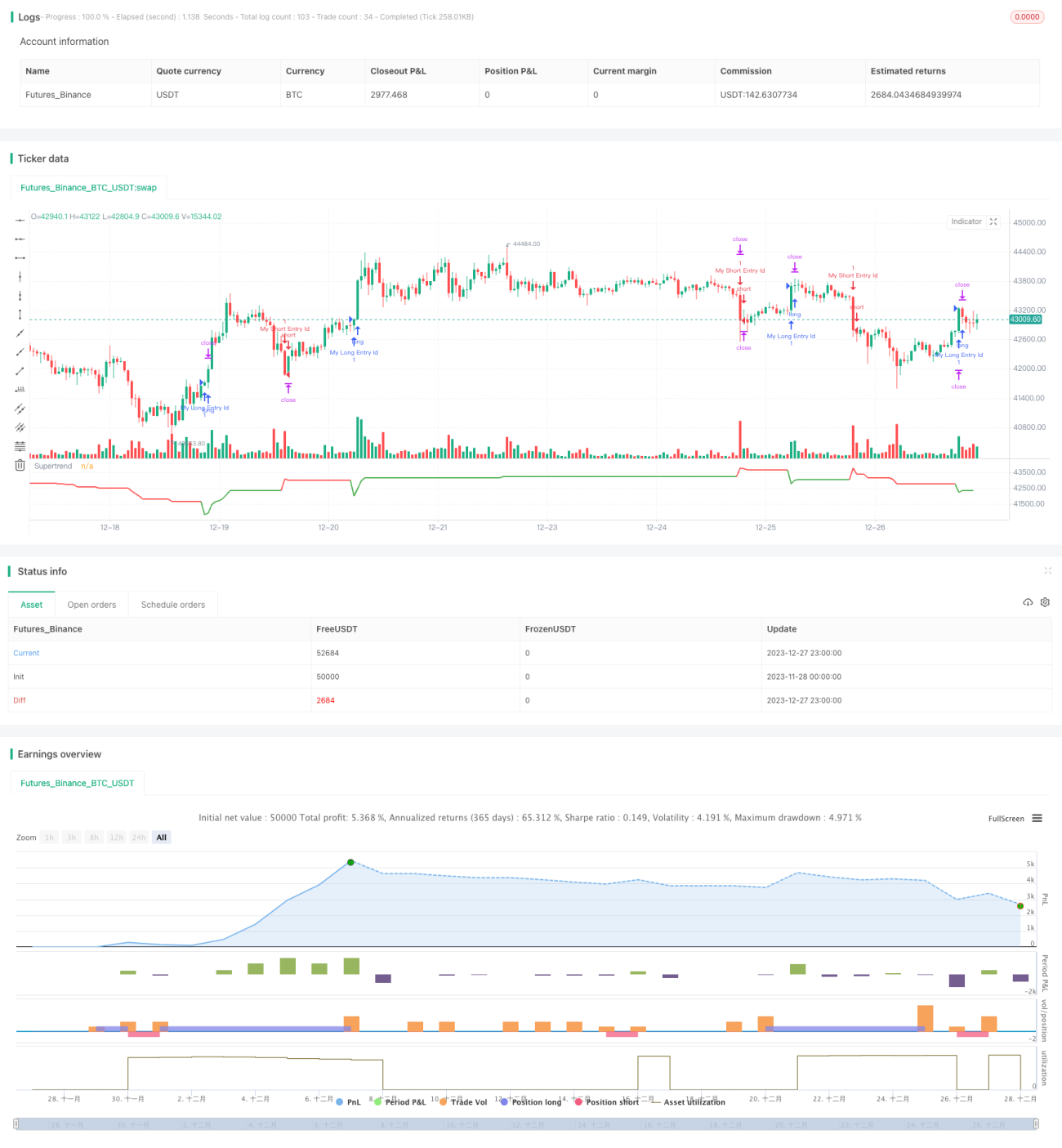

Đây là chiến lược giao dịch dựa trên chỉ báo SuperTrend trên khung nến 5 phút của BankNifty. Chiến lược này chủ yếu sử dụng chỉ báo SuperTrend để nhận diện xu hướng, kết hợp với các quy tắc về phiên giao dịch và quản lý rủi ro để thực hiện giao dịch.

Nguyên lý chiến lược

Chiến lược này trước tiên xác định các biến đầu vào như phiên giao dịch và khoảng thời gian. Phiên giao dịch được đặt theo phiên giao dịch Ấn Độ, từ 9:15 sáng đến 3:10 chiều.

Sau đó, tính toán chỉ báo SuperTrend và hướng của nó. Chỉ báo SuperTrend có thể nhận diện hướng của xu hướng.

Vào đầu mỗi phiên giao dịch, chiến lược chờ 3 cây nến hình thành trước khi xem xét vào lệnh. Điều này nhằm lọc các phá vỡ giả.

Tín hiệu long xảy ra khi hướng của chỉ báo SuperTrend thay đổi từ dưới lên trên; tín hiệu short xảy ra khi hướng của chỉ báo SuperTrend thay đổi từ trên xuống dưới.

Sau khi vào lệnh, sẽ đặt stop loss. Cả stop loss cố định (theo số điểm) và trailing stop theo phần trăm đều có thể điều chỉnh thông qua các biến đầu vào.

Khi kết thúc phiên giao dịch, chiến lược sẽ đóng tất cả các vị thế còn mở.

Lợi thế của chiến lược

Đây là một chiến lược giao dịch đơn giản sử dụng chỉ báo để nhận diện xu hướng. Chiến lược này có những lợi thế sau:

- Sử dụng chỉ báo SuperTrend để xác định hướng xu hướng, giúp nhận diện xu hướng hiệu quả.

- Kết hợp với phiên giao dịch, có thể tránh được những khoảng thời gian biến động mạnh nhất khi mở cửa và đóng cửa thị trường.

- Thiết lập trailing stop, có thể khóa lợi nhuận.

- Có nhiều tham số có thể điều chỉnh tự do thông qua biến đầu vào, tính thích ứng cao.

Rủi ro của chiến lược

Chiến lược này cũng tồn tại một số rủi ro:

- Chỉ báo SuperTrend có độ trễ, có thể bỏ lỡ thời điểm vào lệnh tốt nhất.

- Dựa vào một chỉ báo duy nhất dễ bị ảnh hưởng bởi các phá vỡ giả, tỷ lệ thắng có thể không cao.

- Không xem xét xu hướng chung của thị trường, có thể xảy ra phân kỳ với thị trường chung.

- Việc thiết lập số điểm stop loss không phù hợp có thể gây ra thua lỗ vượt quá dự kiến.

Có thể giảm thiểu những rủi ro này bằng cách tối ưu hóa các tham số của chỉ báo SuperTrend hoặc thêm các chỉ báo khác để đánh giá.

Hướng tối ưu hóa chiến lược

Chiến lược này cũng có thể được tối ưu hóa từ các khía cạnh sau:

- Thêm các chỉ báo khác để đánh giá, hình thành chiến lược giao dịch kết hợp, có thể nâng cao độ ổn định của chiến lược.

- Bổ sung đánh giá xu hướng thị trường chung, tránh phân kỳ với thị trường.

- Tối ưu hóa các tham số của chỉ báo SuperTrend, tìm ra độ dài và hệ số phù hợp nhất.

- Điều chỉnh chiến lược stop loss, ví dụ điều chỉnh dần điểm stop loss theo diễn biến xu hướng.

- Thử nghiệm các công cụ giao dịch khác nhau để tìm ra công cụ phù hợp nhất với chiến lược này.

Tổng kết

Chiến lược này là một chiến lược giao dịch dựa trên chỉ báo SuperTrend trên khung nến 5 phút của BankNifty. Nó sử dụng chỉ báo SuperTrend để xác định hướng xu hướng, kết hợp với các quy tắc về phiên giao dịch và quản lý rủi ro để giao dịch. So với các chiến lược định lượng phức tạp, chiến lược này có quy tắc đơn giản, rõ ràng, dễ hiểu và dễ thực hiện. Là một chiến lược mẫu, nó cung cấp nền tảng và hướng đi cho việc tối ưu hóa và cải tiến trong tương lai. Thông qua việc không ngừng hoàn thiện và nâng cao, hy vọng chiến lược này có thể trở thành một chiến lược giao dịch định lượng đáng tin cậy và ổn định mang lại lợi nhuận.

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("BankNifty 5min Supertrend Based Strategy, 09:15 Entry with Date Range and Risk Management")

// Session and date range input variables- 1