Chiến lược theo dõi xu hướng tăng của giao cắt vàng

Tổng quan

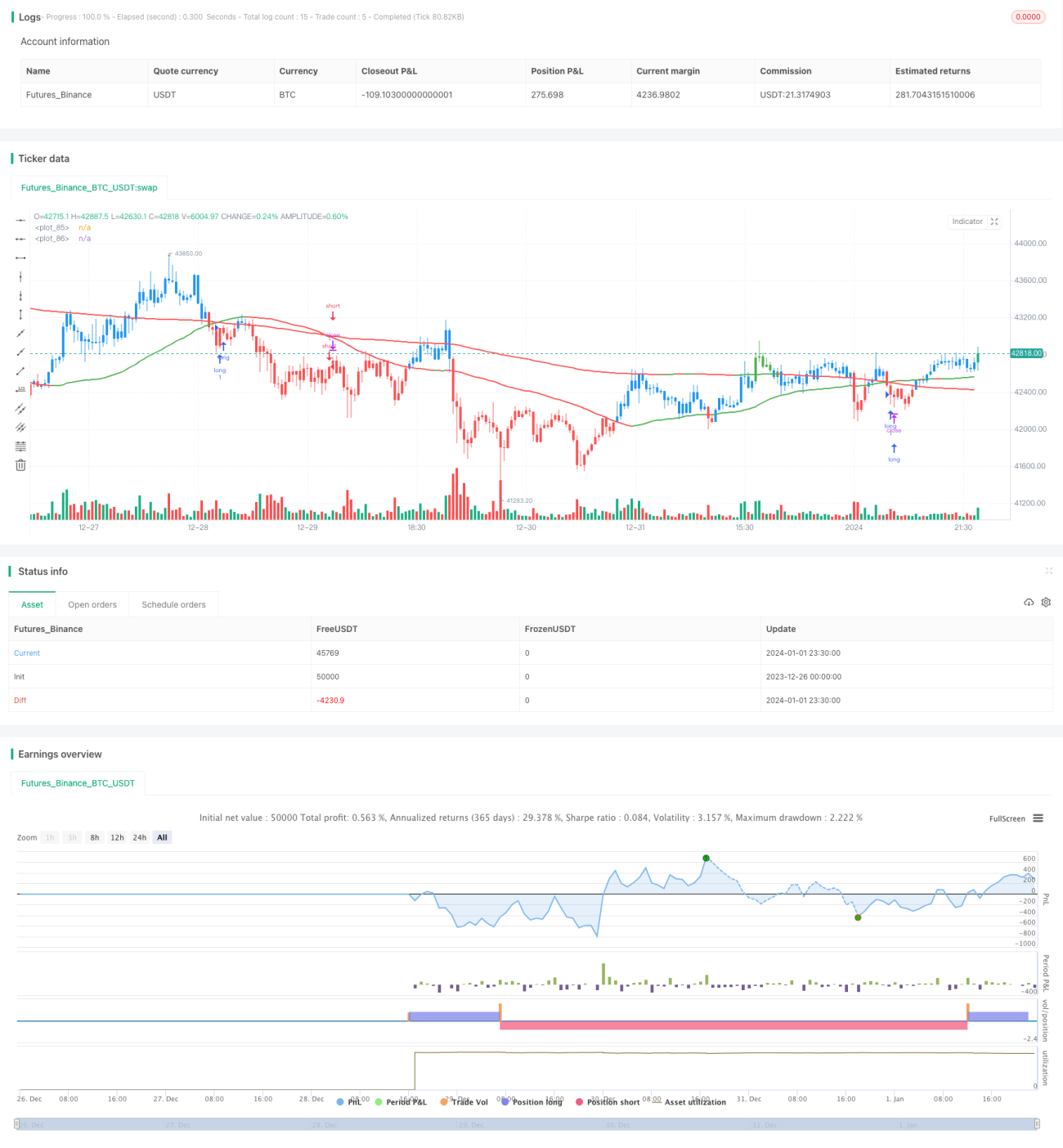

Chiến lược này được thiết kế dựa trên nguyên lý giao cắt vàng của đường trung bình động. Cụ thể, nó sử dụng hai đường trung bình động đơn giản (SMA) với chu kỳ khác nhau: đường SMA 50 chu kỳ và đường SMA 200 chu kỳ. Khi đường SMA 50 chu kỳ cắt lên trên đường SMA 200 chu kỳ, tín hiệu mua được tạo ra; khi đường SMA 50 chu kỳ cắt xuống dưới đường SMA 200 chu kỳ, tín hiệu bán được tạo ra.

Nguyên lý chiến lược

Chiến lược này được viết bằng ngôn ngữ Pine Script, logic chính như sau:

- Tính hai SMA: SMA 50 chu kỳ và SMA 200 chu kỳ.

- Xác định giao cắt vàng: khi SMA 50 chu kỳ cắt lên trên SMA 200 chu kỳ, vào lệnh mua (long).

- Xác định giao cắt tử thần: khi SMA 50 chu kỳ cắt xuống dưới SMA 200 chu kỳ, đóng vị thế.

Tầm quan trọng của việc sử dụng chỉ báo SMA ở đây là nó có thể lọc hiệu quả nhiễu của dữ liệu thị trường, nắm bắt xu hướng dài hạn. Đường SMA nhanh cắt lên trên đường SMA chậm cho thấy đà tăng ngắn hạn đã vượt qua xu hướng giảm dài hạn, tín hiệu mua được hình thành.

Ưu điểm của chiến lược

Chiến lược này có các ưu điểm sau:

- Nguyên lý đơn giản, dễ hiểu, dễ thực hiện.

- Cài đặt tham số hợp lý, có thể tùy chỉnh chu kỳ của hai SMA để thích ứng với các thị trường khác nhau.

- Được viết bằng ngôn ngữ Pine phiên bản ổn định, chạy hiệu quả.

- Cài đặt trực quan phong phú, dễ sử dụng.

Rủi ro và cách khắc phục

Chiến lược này cũng tồn tại một số rủi ro:

-

Có thể xuất hiện phá vỡ giả, khiến chiến lược tạo ra tín hiệu sai. Có thể điều chỉnh tham số của hai SMA một cách phù hợp để giảm xác suất phá vỡ giả.

-

Không thể phản ứng với thị trường ngắn hạn, chỉ phù hợp với nhà đầu tư dài hạn. Có thể rút ngắn chu kỳ của SMA nhanh một cách phù hợp.

-

Mức sụt giảm (drawdown) có thể lớn. Có thể đặt điểm dừng lỗ hoặc điều chỉnh quản lý vị thế một cách phù hợp.

Hướng tối ưu

Chiến lược này có thể tiếp tục tối ưu từ các khía cạnh sau:

-

Thêm các bộ lọc chỉ báo khác, kết hợp nhiều điều kiện mua/bán để giảm xác suất tín hiệu sai.

-

Thêm cơ chế dừng lỗ. Khi giá phá vỡ một mức nhất định, cưỡng chế dừng lỗ.

-

Tối ưu quản lý vị thế. Ví dụ tăng vị thế theo xu hướng, trailing stop, v.v. Kiểm soát mức sụt giảm và theo đuổi lợi nhuận cao hơn.

-

Tối ưu hóa tham số. Đánh giá ảnh hưởng của các tham số khác nhau đến tỷ lệ lợi nhuận/rủi ro.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược giao dịch theo xu hướng điển hình. Nó tận dụng ưu điểm của SMA, nắm bắt xu hướng dài hạn một cách đơn giản và hiệu quả. Có thể tùy chỉnh theo phong cách và tham số điều chỉnh của riêng mình. Đồng thời cũng cần lưu ý một số điểm hạn chế hiện có để tiến hành tối ưu và cải thiện thêm.

/*backtest

start: 2023-12-26 00:00:00

end: 2024-01-02 00:00:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version=4

//

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// www.tradingview.com/u/TradeFab/- 1