Chiến lược thoát lệnh Đèn chùm

Tổng quan

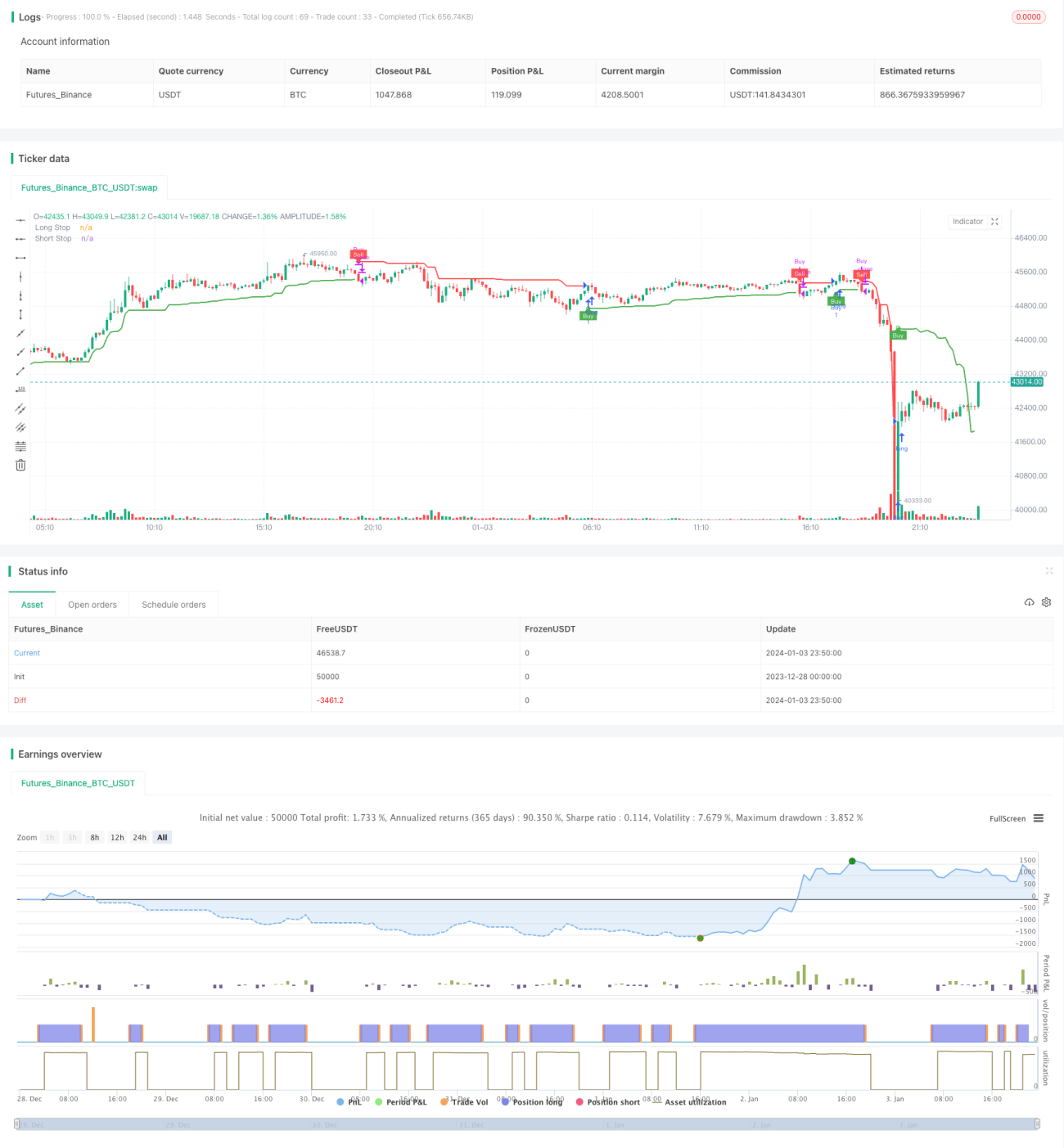

Chiến lược này sử dụng chỉ báo Đèn chùm (Chandelier Exit) để xác định hướng và sức mạnh của sự phá vỡ giá, từ đó tạo ra tín hiệu mua và bán. Nó chỉ thực hiện các lệnh mua.

Nguyên lý chiến lược

Chiến lược này dựa trên chỉ báo Đèn chùm, chỉ báo này thiết lập đường dừng lỗ dựa trên giá cao nhất, giá thấp nhất và phạm vi dao động thực trung bình (ATR). Cụ thể, chiến lược tính toán ATR 22 kỳ và nhân với một hệ số (mặc định là 3). Sau đó, dựa trên giá trị này, nó thiết lập đường dừng lỗ dài hạn và đường dừng lỗ ngắn hạn. Khi chiến lược nắm giữ vị thế mua, nếu giá phá vỡ xuống dưới đường dừng lỗ dài hạn, nó sẽ tạo ra tín hiệu bán; nếu vị thế bán, khi giá phá vỡ trên đường dừng lỗ ngắn hạn, nó sẽ tạo ra tín hiệu mua.

Chiến lược này chỉ thực hiện các lệnh mua. Cụ thể, nó tạo ra tín hiệu mua khi giá phá vỡ lên trên đường dừng lỗ dài hạn trước đó. Sau đó, nó tạo ra tín hiệu bán và đóng vị thế khi giá phá vỡ xuống dưới đường dừng lỗ ngắn hạn.

Phân tích ưu điểm

- Sử dụng chỉ báo Đèn chùm để thiết lập đường dừng lỗ động, giúp kiểm soát rủi ro hiệu quả

- Kết hợp với sự phá vỡ giá để tạo ra tín hiệu giao dịch, có thể nắm bắt được xu hướng của giá

- Chỉ thực hiện các lệnh mua, tạo ra một chiến lược tránh được sự đảo chiều ở cả hai đầu thị trường

- Thiết lập nhiều loại cảnh báo kích hoạt theo điều kiện, giúp giám sát trạng thái chiến lược ngay lập tức

Phân tích rủi ro

- Chỉ báo Đèn chùm khá nhạy cảm với biên độ dao động; nếu xuất hiện biến động giá bất thường, có thể gây ra tín hiệu sai

- Sau khi mua vào không có cài đặt cắt lỗ, không thể kiểm soát hiệu quả rủi ro thua lỗ

- Không có cơ chế chốt lời theo dõi (trailing stop), không thể khóa lợi nhuận

Giải pháp cho rủi ro:

- Kết hợp với các chỉ báo khác để lọc tín hiệu, tránh tín hiệu sai

- Cài đặt đường cắt lỗ, giới hạn tỷ lệ thua lỗ tối đa

- Thêm cơ chế chốt lời theo dõi, có thể cân nhắc điều chỉnh đường bán động hoặc thoát một phần

Hướng tối ưu hóa

- Có thể thử nghiệm các thiết lập tham số khác nhau để tối ưu hóa thời điểm mua và bán

- Có thể thêm xác nhận từ các chỉ báo khác để tránh tín hiệu sai

- Có thể cân nhắc thực hiện đồng thời cả lệnh mua và bán

- Có thể cài đặt cơ chế cắt lỗ và chốt lời

Tổng kết

Chiến lược này sử dụng đường dừng lỗ động của chỉ báo Đèn chùm để nhận diện cơ hội đảo chiều giá. Nó chỉ mua vào khi giá phá vỡ lên trên đường dừng lỗ dài hạn và bán ra khi giá phá vỡ xuống dưới đường dừng lỗ ngắn hạn, tạo ra một chiến lược đơn giản, giao dịch một chiều và tránh được sự đảo chiều ở cả hai đầu thị trường. Chiến lược này kiểm soát rủi ro hiệu quả, nhưng không có cài đặt cắt lỗ và chốt lời. Chúng ta có thể tối ưu hóa chiến lược bằng cách thêm các chỉ báo lọc và thiết lập cắt lỗ/chốt lời để làm cho nó vững chắc hơn.

- 1