Chiến lược trailing stop loss động

Tổng quan

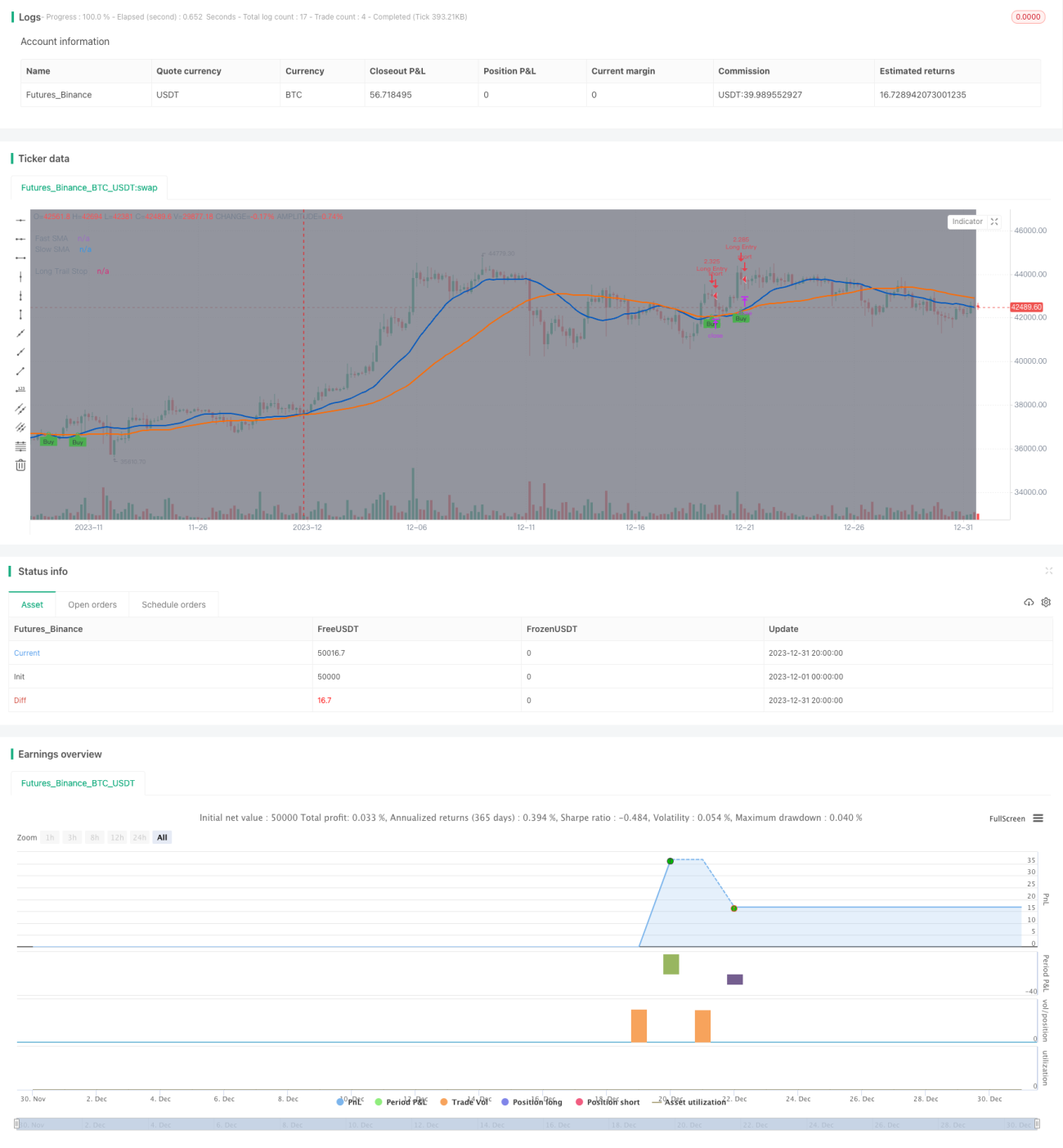

Chiến lược này xác định xu hướng thông qua sự giao cắt của đường trung bình động nhanh và đường trung bình động chậm. Khi đường trung bình động nhanh cắt lên trên đường trung bình động chậm, chiến lược sẽ mở vị thế mua (long) và thiết lập một đường dừng lỗ động để khóa lợi nhuận. Khi giá thay đổi một tỷ lệ nhất định, vị thế sẽ được đóng theo lệnh dừng lỗ.

Nguyên lý chiến lược

Chiến lược này sử dụng giao cắt vàng (golden cross) giữa đường trung bình động nhanh và đường trung bình động chậm để xác định sự bắt đầu của xu hướng tăng. Cụ thể, tính đường trung bình động đơn giản của giá đóng cửa trong một chu kỳ nhất định, so sánh giá trị của đường trung bình nhanh và đường trung bình chậm. Khi đường trung bình nhanh cắt lên trên đường trung bình chậm, xác định xu hướng tăng bắt đầu và mở vị thế mua tại thời điểm đó.

Sau khi mở vị thế mua, chiến lược không đặt dừng lỗ cố định mà sử dụng một đường dừng lỗ động để khóa lợi nhuận. Cách thiết lập đường dừng lỗ này là: Giá cao nhất * (1 - tỷ lệ dừng lỗ đã thiết lập). Nhờ đó, đường dừng lỗ sẽ tăng lên khi giá tăng và thoát lệnh khi giá giảm xuống một tỷ lệ nhất định.

Ưu điểm của phương pháp này là có thể theo đuổi xu hướng tăng vô hạn và có thể khóa lợi nhuận sau khi đạt được một mức lợi nhuận nhất định thông qua dừng lỗ.

Phân tích ưu điểm

Ưu điểm chính của chiến lược dừng lỗ động này là:

-

Có thể theo đuổi xu hướng tăng vô hạn, không bỏ lỡ các biến động lớn. Sử dụng dừng lỗ cố định dễ bị thoát lệnh ngay khi xu hướng lớn mới bắt đầu.

-

Có thể khóa lợi nhuận bằng cách thiết lập tỷ lệ dừng lỗ. Nếu chỉ theo đuổi xu hướng mà không dừng lỗ, có thể bị lỗ khi kết thúc xu hướng. Thiết lập dừng lỗ có thể khóa lợi nhuận.

-

Linh hoạt hơn so với dừng lỗ cố định. Dừng lỗ cố định chỉ có thể đặt một mức giá duy nhất, trong khi dừng lỗ ở đây thay đổi theo giá cao nhất.

-

Rủi ro sụt giảm (drawdown) nhỏ hơn. Khi sử dụng dừng lỗ cố định, giá dừng lỗ cách xa giá cao nhất, có thể bị dừng lỗ trong các đợt điều chỉnh bình thường. Ở đây, khoảng cách dừng lỗ rất gần với giá cao nhất, nên các đợt điều chỉnh bình thường sẽ không kích hoạt dừng lỗ.

Phân tích rủi ro

Chiến lược này cũng có một số rủi ro:

-

Chỉ báo xác định tín hiệu vào lệnh không ổn định, có thể tạo ra tín hiệu sai.

-

Chỉ có một phương pháp dừng lỗ duy nhất, không xem xét các yếu tố khác. Thị trường có thể đột ngột thay đổi lớn khiến chiến lược mất hiệu quả.

-

Không có giới hạn chốt lời (take profit), phụ thuộc vào dừng lỗ. Nếu dừng lỗ thất bại, có thể gây ra thua lỗ lớn.

-

Cần tối ưu hóa các thông số dữ liệu. Các tham số như chu kỳ đường trung bình động cần được điều chỉnh để đạt tối ưu.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

-

Thêm nhiều chỉ báo hơn để xác nhận tín hiệu vào lệnh, tránh tín hiệu sai. Ví dụ: thêm chỉ báo khối lượng giao dịch.

-

Thêm cài đặt chốt lời. Khi lợi nhuận đạt đến một tỷ lệ nhất định thì chốt lời.

-

Tăng cường tính an toàn của dừng lỗ. Khi thị trường xảy ra bất thường, điều chỉnh khoảng cách dừng lỗ lớn hơn.

-

Tối ưu hóa các sản phẩm giao dịch, khung thời gian giao dịch, v.v. Các tham số cho từng sản phẩm và khung thời gian khác nhau cần được điều chỉnh.

-

Thêm học máy (machine learning) để tự động điều chỉnh tham số. Giúp mô hình tự động tối ưu hóa các chỉ báo đánh giá và mức dừng lỗ.

Tổng kết

Chiến lược này có tư duy tổng thể rõ ràng và hợp lý. Sử dụng đường trung bình động nhanh và chậm để xác định xu hướng là một phương pháp kinh điển, và kỹ thuật dừng lỗ động có thể khóa lợi nhuận hiệu quả và giảm rủi ro. Tuy nhiên, các chỉ báo và tham số này cần được liên tục kiểm tra và tối ưu hóa để chiến lược có thể sinh lời ổn định. Đồng thời, cũng cần phòng ngừa tác động của những thay đổi lớn của thị trường đối với chiến lược, điều này đòi hỏi hoàn thiện tư duy và khung tổng thể, đồng thời bổ sung các cơ chế an toàn.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1