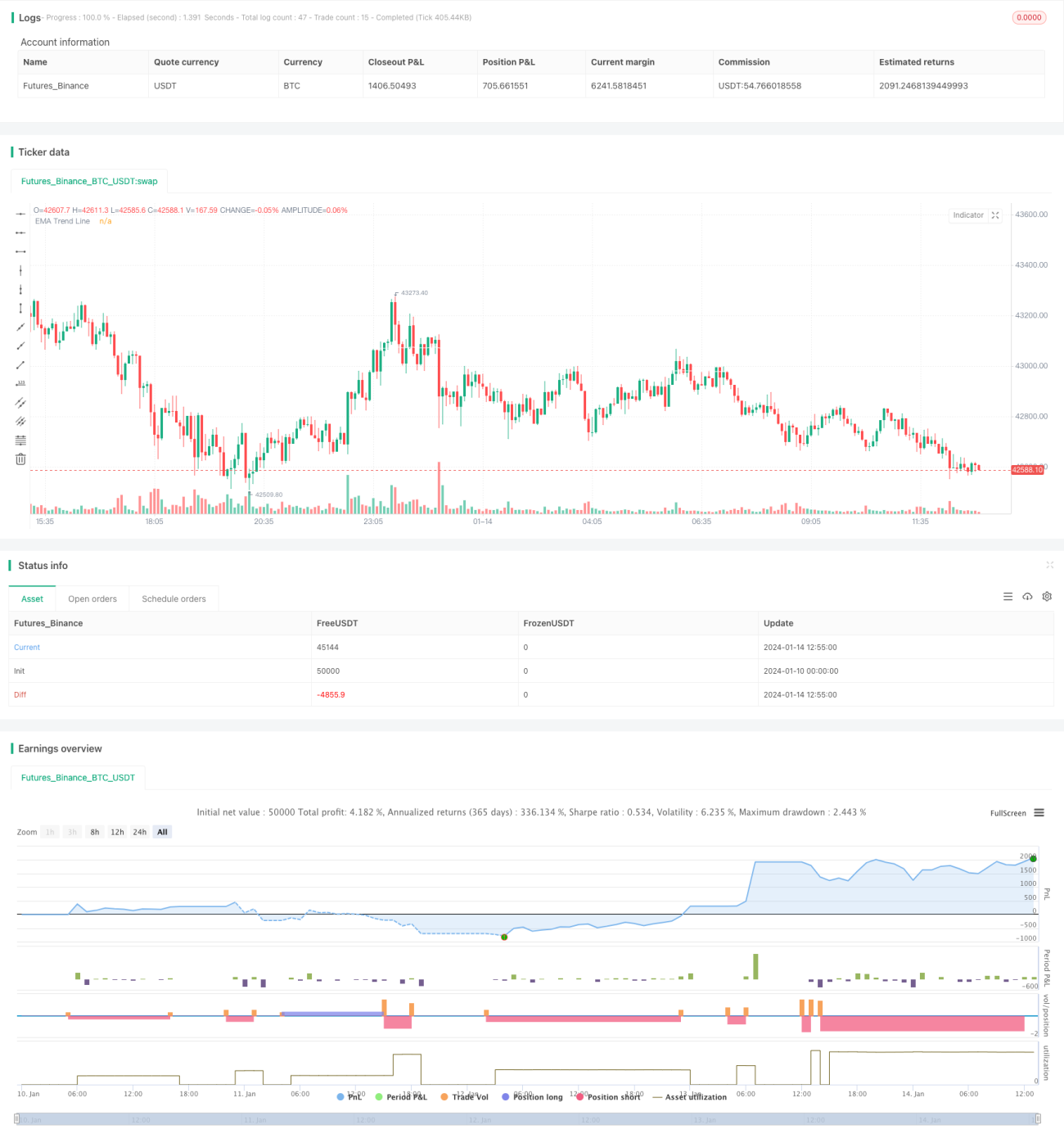

Chiến lược theo dõi xu hướng kết hợp EMA kép và RSI

Tổng quan

Chiến lược này kết hợp sử dụng chỉ báo EMA kép và RSI để xác định xu hướng giá và vào lệnh kịp thời khi xu hướng đảo chiều. Cụ thể, chiến lược sử dụng EMA chu kỳ dài hơn để xác định xu hướng chính, đồng thời sử dụng RSI để nhận biết tình trạng quá mua/quá bán trong ngắn hạn. Khi giá có sự thoái lui theo hướng xu hướng chính, tín hiệu giao dịch được phát ra dựa trên RSI, từ đó vào lệnh mua hoặc bán tùy theo hướng xu hướng.

Nguyên lý chiến lược

-

Sử dụng EMA 200 chu kỳ để xác định xu hướng chính. Giá cắt lên trên đường EMA là tín hiệu tăng, cắt xuống dưới là tín hiệu giảm.

-

Chỉ báo RSI được thiết lập với tham số 10 chu kỳ. Trong đó, RSI cắt lên trên 40 là tín hiệu quá bán, cắt xuống dưới 60 là tín hiệu quá mua.

-

Khi xu hướng chính là tăng (giá cao hơn đường EMA), nếu xảy ra tín hiệu RSI cắt xuống dưới 40 (quá bán), vào lệnh mua.

-

Khi xu hướng chính là giảm (giá thấp hơn đường EMA), nếu xảy ra tín hiệu RSI cắt lên trên 60 (quá mua), vào lệnh bán.

-

Stop loss được thiết lập bằng 4 lần ATR. Take profit được thiết lập bằng 2 lần stop loss, đạt tỷ lệ rủi ro/lợi nhuận 2:1.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là kết hợp cả chỉ báo xu hướng và đảo chiều, cho phép vào lệnh kịp thời khi xu hướng có sự thoái lui, nhờ đó đạt được hiệu suất tốt. Các ưu điểm cụ thể như sau:

-

Sử dụng hệ thống hai đường EMA để xác định xu hướng chính, giúp theo dõi xu hướng giá hiệu quả.

-

Chỉ báo RSI có thể nhận biết tình trạng quá mua/quá bán trong ngắn hạn, hỗ trợ xác định thời điểm vào lệnh.

-

Stop loss được thiết lập dựa trên ATR, có thể điều chỉnh mức cắt lỗ theo biến động thị trường, có lợi cho quản lý rủi ro.

-

Tuân thủ nghiêm ngặt nguyên tắc giao dịch theo xu hướng, giúp giảm thiểu các giao dịch không cần thiết và hạ thấp rủi ro hệ thống.

Phân tích rủi ro

Chiến lược này tồn tại các rủi ro chính sau:

-

Trong quá trình xu hướng đi ngang hoặc suy yếu, có thể phát sinh tín hiệu giao dịch sai. Khi đó cần đánh giá tình hình thận trọng trước khi vào lệnh.

-

Trong các điều kiện thị trường cực đoan, mức stop loss được thiết lập bởi ATR có thể quá lớn hoặc quá nhỏ, cần điều chỉnh linh hoạt. Cũng có thể xem xét thay thế bằng phương pháp stop loss khác.

-

Tần suất phát tín hiệu giao dịch có thể cao, cần xem xét liệu có phù hợp với sở thích tần suất giao dịch của bạn hay không.

-

Cần chú ý xem tham số RSI đã được thiết lập phù hợp chưa, nên tối ưu hóa tham số định kỳ.

Hướng tối ưu hóa

Các hướng tối ưu hóa chính của chiến lược này như sau:

-

Có thể thử nghiệm thêm các chỉ báo xu hướng khác như MACD để hỗ trợ xác định hướng xu hướng.

-

Có thể thử nghiệm kết hợp các chỉ báo đảo chiều khác như KDJ, Bollinger Bands với RSI để tìm tín hiệu giao dịch tốt hơn.

-

Có thể đưa vào các thuật toán học máy để tự động điều chỉnh tham số, thực hiện stop loss và take profit động.

-

Có thể kết hợp các yếu tố như chỉ báo tâm lý, tin tức để đánh giá, nâng cao độ ổn định tổng thể của hệ thống.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược giao dịch ngắn hạn rất điển hình, kết hợp giữa theo dõi xu hướng và chỉ báo đảo chiều. Bằng cách sử dụng hai đường EMA để xác định xu hướng chính, đồng thời tận dụng đặc tính đảo chiều của RSI để bắt cơ hội Pullback trong xu hướng và vào lệnh. Về mặt nguyên lý, chiến lược này kết hợp ưu điểm của các chỉ báo khác nhau, tạo thành hiệu ứng bổ trợ tốt. Nếu sau này được cải thiện thông qua tối ưu hóa tham số, kết hợp mô hình và các biện pháp khác, hiệu quả của chiến lược này vẫn còn nhiều dư địa để nâng cao.

- 1