Chiến lược giao dịch tối ưu hai chiều MACD

II. Tổng quan chiến lược

Chiến lược này sử dụng chỉ báo MACD và nguyên lý giao cắt đường trung bình động để xây dựng tín hiệu giao dịch. Ưu điểm của nó là có thể tối ưu hóa riêng biệt các tham số MACD cho hướng mua và bán, giúp các tham số được cấu hình tối ưu cho từng hướng thị trường khác nhau.

III. Nguyên lý chiến lược

- Tính toán riêng chỉ báo MACD cho hai hướng mua và bán. Hướng mua sử dụng một bộ tham số, hướng bán sử dụng một bộ tham số khác, có thể tự do cấu hình.

- Xác định giao cắt giữa đường MACD và đường Signal để tạo tín hiệu giao dịch. Khi mua, xem xét giao cắt tăng; khi bán, xem xét giao cắt giảm.

- Có thể cấu hình liệu có yêu cầu đường Signal cũng phải giao cắt mới kích hoạt tín hiệu hay không, nhằm tránh tín hiệu giả.

- Sau khi vào lệnh mua hoặc bán, chờ giao cắt ngược hướng để đóng vị thế.

IV. Ưu điểm của chiến lược

- Tối ưu hóa tham số hai chiều: Có thể tự do tối ưu hóa tham số cho mua và bán, giúp chúng được cấu hình tối ưu theo hướng thị trường.

- Có thể cấu hình làm mịn tín hiệu: Tham số Signal có thể kiểm soát mức độ làm mịn của đường tín hiệu, lọc nhiễu giả.

- Có thể cấu hình lọc tín hiệu: Có thể cấu hình yêu cầu giao cắt đường Signal mới kích hoạt, tránh nhiễu từ tín hiệu giả.

- Kiểm soát vị thế linh hoạt: Có thể bật riêng lẻ mua hoặc bán, hoặc đồng thời cả mua và bán.

V. Rủi ro của chiến lược

- Vấn đề độ trễ của MACD: Bản thân MACD có độ trễ nhất định, có thể bỏ lỡ các đảo chiều nhanh.

- Rủi ro chuyển đổi mua/bán: Khi thị trường biến động nhanh, việc chuyển đổi vị thế có thể quá thường xuyên.

- Rủi ro tham số: Cấu hình tham số không phù hợp có thể không nắm bắt được đặc điểm thị trường.

- Bảo vệ bằng stop-loss: Cần đặt stop-loss hợp lý để kiểm soát lỗ từng giao dịch.

Các phương pháp quản lý rủi ro:

- Kết hợp các chỉ báo khác để đánh giá xu hướng tổng thể, tránh mua đuổi đỉnh bán đáy.

- Thiết lập các tham số trễ tín hiệu và làm mịn để giảm tín hiệu sai.

- Kiểm tra và tối ưu hóa tham số nhiều lần, để phù hợp với nhịp điệu thị trường ở các khung thời gian khác nhau.

- Thiết lập cơ chế stop-loss và take-profit để kiểm soát lỗ từng giao dịch.

VI. Hướng tối ưu hóa

Có thể tối ưu hóa chiến lược này từ các khía cạnh sau:

-

Kiểm tra các tổ hợp tham số đường nhanh và đường chậm khác nhau, tìm ra tham số tốt nhất cho các khung thời gian thị trường khác nhau.

-

Kiểm tra các tham số đường Signal khác nhau, đường tín hiệu mượt hơn có thể lọc nhiễu nhiều hơn.

-

Kiểm tra sự khác biệt giữa bật và tắt bộ lọc giao cắt đường Signal, tìm ra sự cân bằng tối ưu.

-

Đặt tỷ lệ stop-loss và take-profit tối ưu dựa trên kết quả backtest.

-

Thử nghiệm chỉ mua hoặc chỉ bán, xem có thể tối đa hóa hiệu quả của chiến lược hay không.

VII. Kết luận

Chiến lược giao dịch tối ưu hóa hai chiều với MACD này, bằng cách cấu hình riêng tham số cho mua và bán, đã đạt được sự tối ưu hóa theo từng hướng thị trường khác nhau, có thể tự do điều chỉnh hướng tham gia. Đồng thời, cơ chế lọc tín hiệu được thêm vào để tránh tín hiệu sai. Thông qua tối ưu hóa tham số và các biện pháp quản lý rủi ro, có thể nâng cao hiệu quả của chiến lược.

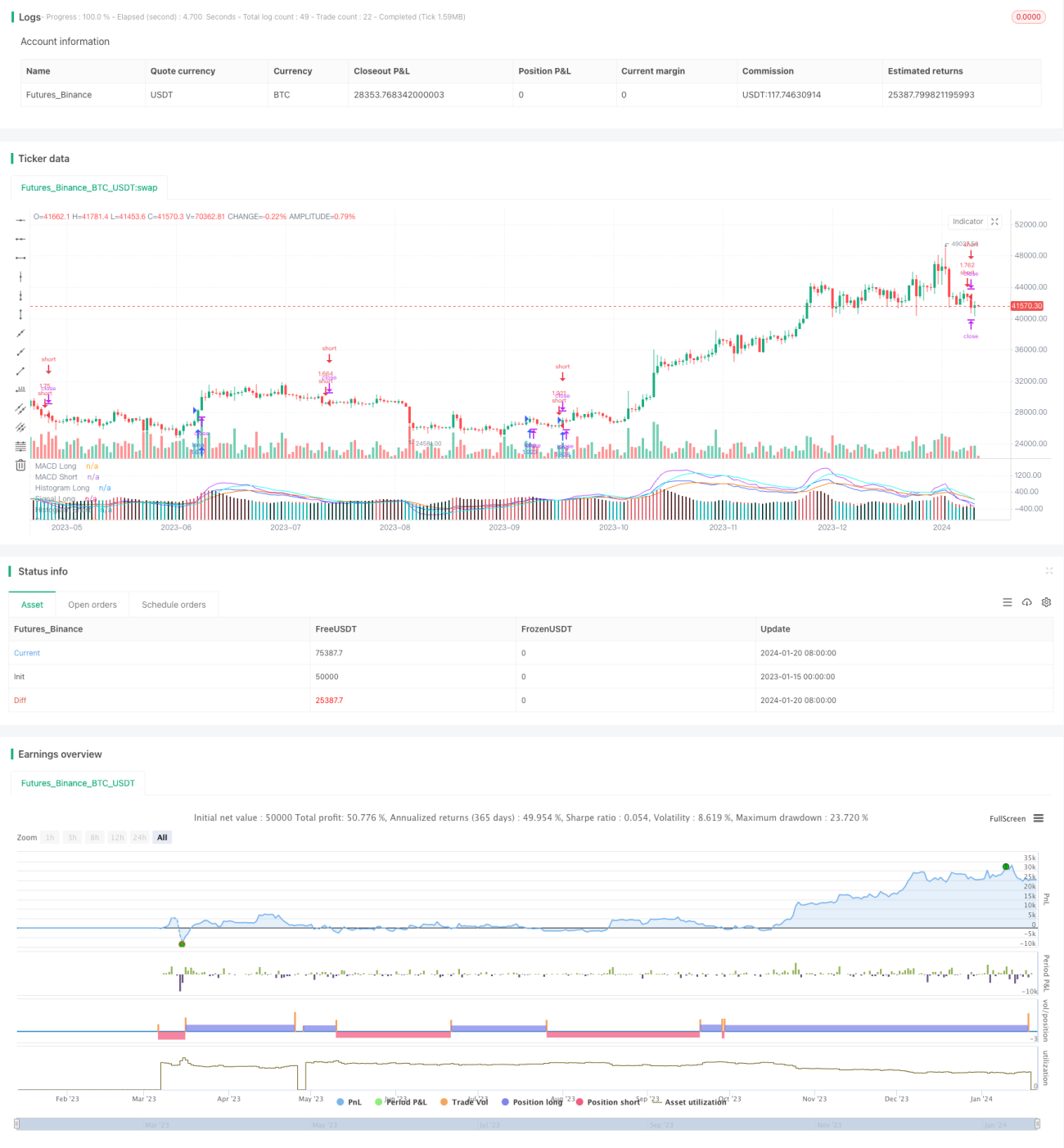

/*backtest

start: 2023-01-15 00:00:00

end: 2024-01-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Gentleman-Goat & TradingTools.Software/Optimizer

strategy(title="MACD Short/Long Strategy for TradingView Input Optimizer", shorttitle="MACD Short/Long TVIO", initial_capital=1000, default_qty_value=100, default_qty_type=strategy.percent_of_equity)- 1