Dựa trên chiến lược giao dịch lưới động

1

Follow

1802

Followers

Tổng quan

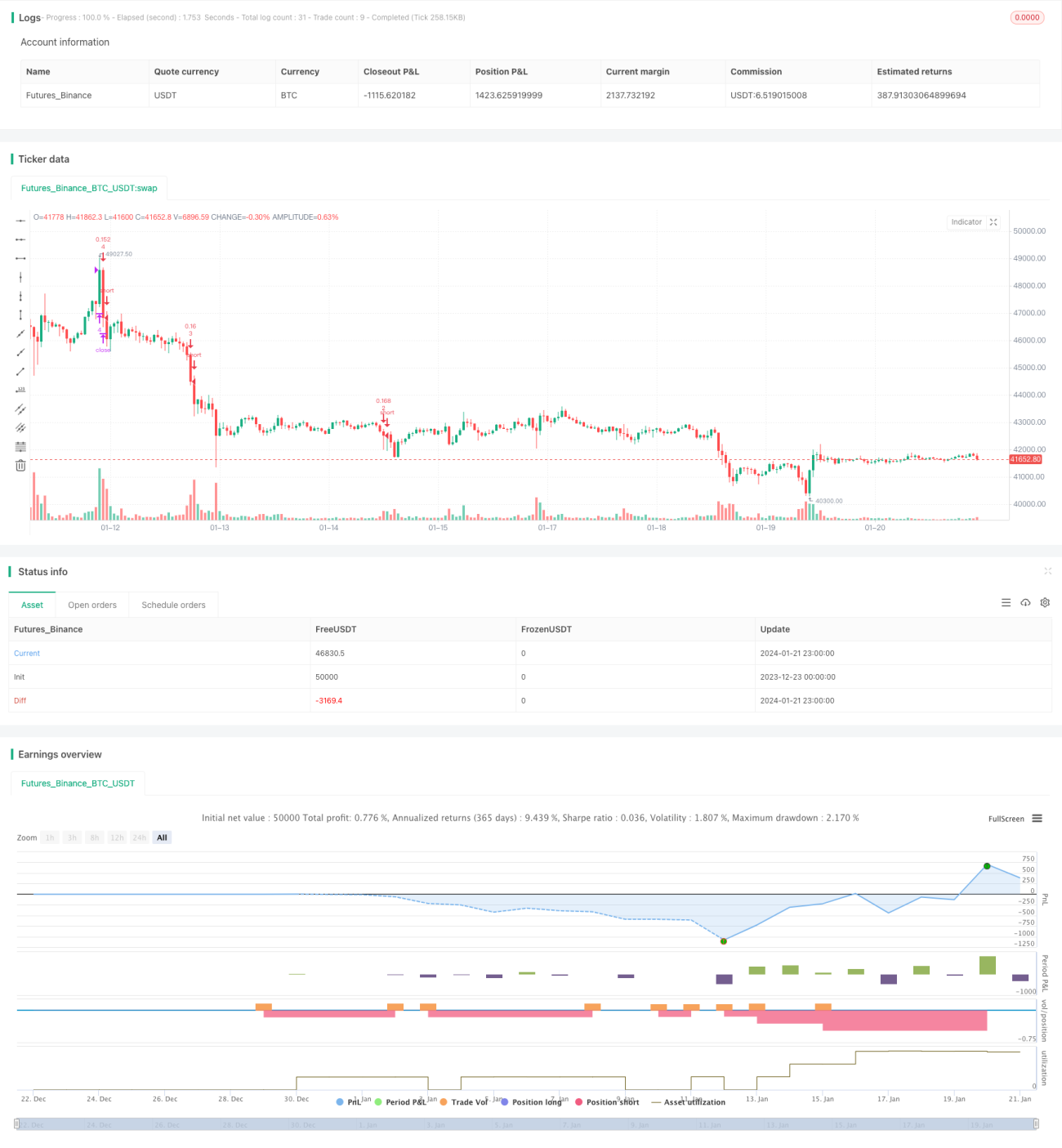

Chiến lược này thực hiện giao dịch lưới bằng cách thiết lập nhiều lệnh mua và bán song song trong một khoảng giá, điều chỉnh phạm vi lưới và các đường lưới dựa trên biến động thị trường để đạt được lợi nhuận.

Nguyên lý chiến lược

- Thiết lập biên trên và biên dưới của lưới, có thể thiết lập thủ công hoặc tự động tính toán dựa trên giá cao nhất và thấp nhất trong một khoảng thời gian gần đây.

- Tính toán độ rộng của khoảng lưới dựa trên số lượng lưới đã thiết lập.

- Tạo ra mảng giá các đường lưới tương ứng với số lượng lưới.

- Khi giá thấp hơn một đường lưới nào đó, mở lệnh mua bên dưới đường đó; khi giá cao hơn một đường lưới nào đó, đóng lệnh bán bên trên đường đó.

- Điều chỉnh linh hoạt biên trên, biên dưới, độ rộng khoảng và giá các đường lưới để thích ứng với biến động thị trường.

Phân tích ưu điểm

- Có thể đạt được lợi nhuận ổn định trong thị trường đi ngang và biến động, không bị ảnh hưởng bởi xu hướng một chiều.

- Hỗ trợ cài đặt thủ công và tự động tính toán khoảng lưới, khả năng thích ứng cao.

- Có thể tối ưu hóa lợi nhuận bằng cách điều chỉnh số lượng lưới, độ rộng lưới và khối lượng lệnh.

- Tích hợp kiểm soát vị thế, giúp quản lý rủi ro.

- Hỗ trợ điều chỉnh linh hoạt phạm vi lưới, giúp chiến lược có khả năng thích ứng cao.

Phân tích rủi ro

- Khi thị trường có xu hướng mạnh, có thể xảy ra thua lỗ lớn.

- Thiết lập số lượng lưới và vị thế không phù hợp có thể khuếch đại rủi ro.

- Việc tự động tính toán khoảng lưới có thể không hiệu quả trong các điều kiện thị trường cực đoan.

Cách khắc phục rủi ro:

- Tối ưu hóa tham số lưới, kiểm soát chặt chẽ tổng vị thế.

- Đóng chiến lược trước khi xuất hiện xu hướng lớn.

- Kết hợp các chỉ báo xu hướng để đánh giá tình hình thị trường, đóng chiến lược nếu cần thiết.

Hướng tối ưu hóa

- Kết hợp đặc điểm thị trường và quy mô vốn để chọn số lượng lưới tối ưu.

- Thử nghiệm các khung thời gian khác nhau để tối ưu hóa tham số tự động tính lưới.

- Tối ưu hóa cách tính khối lượng lệnh để đạt được lợi nhuận ổn định hơn.

- Kết hợp các chỉ báo khác để nhận diện xu hướng lớn, thiết lập điều kiện đóng chiến lược.

Tổng kết

Chiến lược giao dịch lưới động này thích ứng với biến động thị trường bằng cách điều chỉnh linh hoạt các tham số khoảng lưới, giúp thu lợi nhuận trong thị trường đi ngang và biến động. Đồng thời, thiết lập kiểm soát vị thế phù hợp có thể quản lý rủi ro. Việc tối ưu hóa tham số lưới và kết hợp các chỉ báo xu hướng có thể nâng cao độ ổn định của chiến lược.

Source

Pine

/*backtest

start: 2023-12-23 00:00:00

end: 2024-01-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("sarasa srinivasa kumar", overlay=true, pyramiding=14, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.1)

i_autoBounds = input(group="Grid Bounds", title="Use Auto Bounds?", defval=true, type=input.bool) // calculate upper and lower bound of the grid automatically? This will theorhetically be less profitable, but will certainly require less attention

i_boundSrc = input(group="Grid Bounds", title="(Auto) Bound Source", defval="Hi & Low", options=["Hi & Low", "Average"]) // should bounds of the auto grid be calculated from recent High & Low, or from a Simple Moving AverageStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1