Chiến lược Grid sóng lợi nhuận dao động

Tổng quan

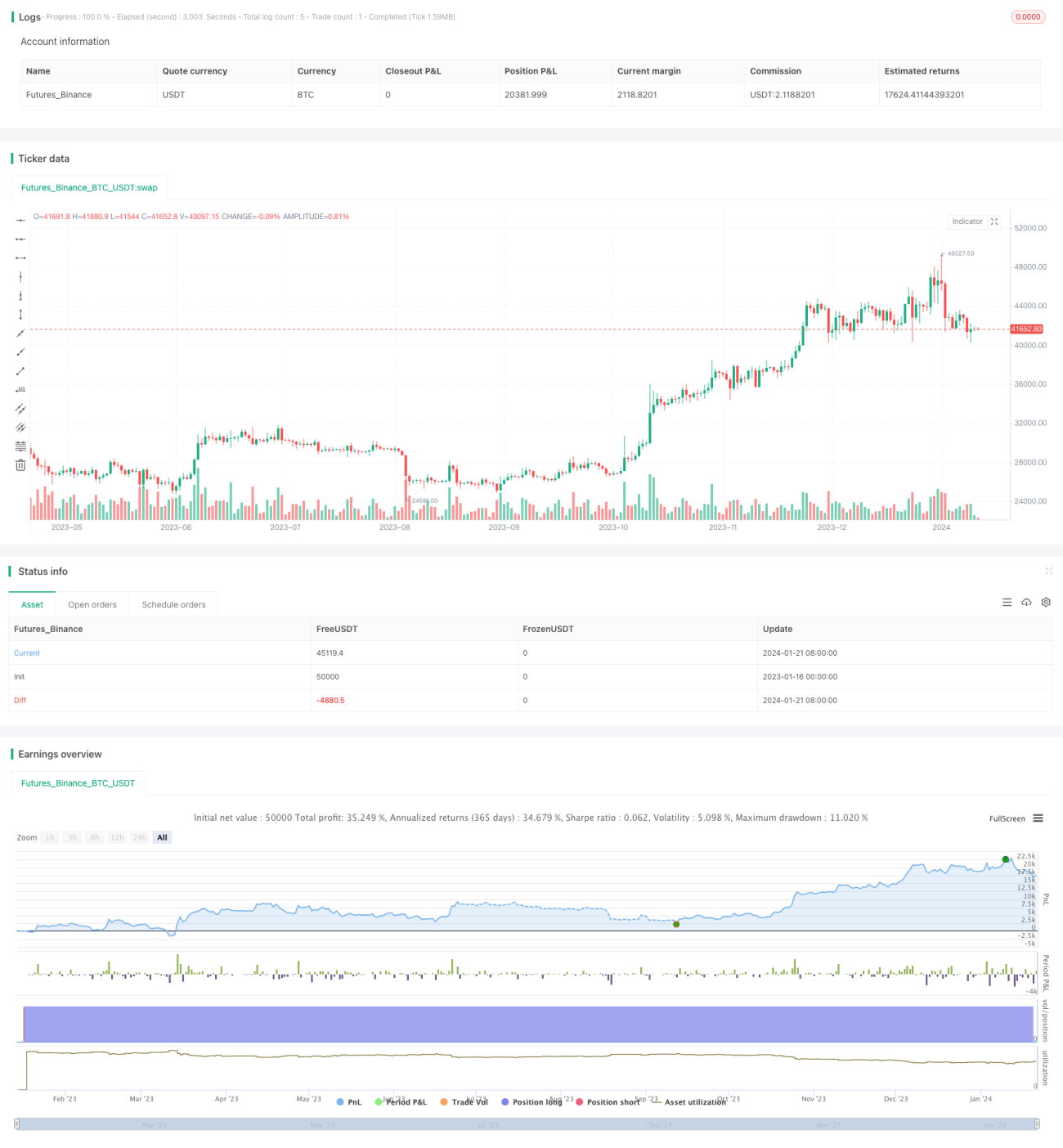

Chiến lược Grid dao động lợi nhuận (Grid chiến thuật biến động sinh lời) là một chiến lược theo xu hướng, tự động thiết lập lưới dựa trên biến động giá, giúp thu lợi nhuận liên tục khi giá dao động.

Nguyên lý chiến lược

Cốt lõi của chiến lược này là xây dựng một lưới dao động giá. Khi giá đi vào các vùng dao động khác nhau, các tín hiệu giao dịch mới sẽ được tạo ra. Ví dụ, nếu khoảng cách lưới được đặt là 500 đô la, thì khi giá tăng hơn 500 đô la, một tín hiệu mua mới sẽ xuất hiện.

Cụ thể, chiến lược liên tục di chuyển để thiết lập các lưới mới bằng cách theo dõi mức giá cao nhất hoặc thấp nhất mới. Trong code, chúng ta định nghĩa một biến re_grid để lưu trữ mức giá lưới hiện tại. Chỉ cần giá phá vỡ mức giá lưới này với một khoảng cách lớn hơn khoảng cách lưới đã thiết lập, mức giá lưới tiếp theo sẽ được tính toán lại.

Như vậy, khi giá có biến động đủ lớn, các tín hiệu giao dịch mới sẽ được tạo ra, và chúng ta có thể kiếm lợi nhuận bằng cách mua hoặc bán. Khi giá bắt đầu di chuyển ngược hướng vượt quá khoảng cách lưới, vị thế ban đầu sẽ bị cắt lỗ.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là khả năng tự động theo dõi xu hướng giá và sinh lời liên tục. Miễn là giá duy trì biến động đủ lớn, quy mô vị thế của chúng ta sẽ tăng dần và lợi nhuận cũng ngày càng nhiều.

Ngoài ra, bằng cách thiết lập hợp lý các tham số lưới, có thể kiểm soát rủi ro hiệu quả. Hơn nữa, kết hợp với các chỉ báo kỹ thuật như Ichimoku Cloud để lọc tín hiệu sẽ giúp tăng độ ổn định của chiến lược.

Phân tích rủi ro

Rủi ro chính của chiến lược này là giá có thể đột ngột đảo chiều, dẫn đến cắt lỗ. Khi đó, lợi nhuận tích lũy trước đó có thể bị giảm hoặc thua lỗ.

Để kiểm soát rủi ro này, chúng ta có thể đặt mức cắt lỗ, điều chỉnh hợp lý các tham số lưới, lựa chọn các cặp giao dịch có xu hướng mạnh, và kết hợp nhiều chỉ báo kỹ thuật để lọc tín hiệu.

Hướng tối ưu

Chúng ta có thể tiếp tục tối ưu chiến lược từ các khía cạnh sau:

-

Tối ưu các tham số lưới, tìm tổ hợp khoảng cách lưới, quy mô vị thế tối ưu.

-

Thêm hoặc điều chỉnh cơ chế cắt lỗ để kiểm soát rủi ro tốt hơn.

-

Thử nghiệm trên các cặp giao dịch khác nhau, chọn những cặp có biến động lớn và xu hướng rõ ràng hơn.

-

Thêm nhiều chỉ báo kỹ thuật để đánh giá, nâng cao độ ổn định của chiến lược.

Kết luận

Chiến lược Grid dao động lợi nhuận này thông qua việc xây dựng lưới giá tự động theo dõi xu hướng, có thể thu lợi nhuận liên tục một cách hiệu quả. Đồng thời, nó cũng tồn tại rủi ro drawdown nhất định. Bằng cách tối ưu tham số, thiết lập cắt lỗ, lựa chọn cặp giao dịch phù hợp, có thể kiểm soát rủi ro và nâng cao độ ổn định của chiến lược.

- 1