Chiến lược giao dịch BTC dựa trên đường EMA và chỉ báo MACD

Tổng quan

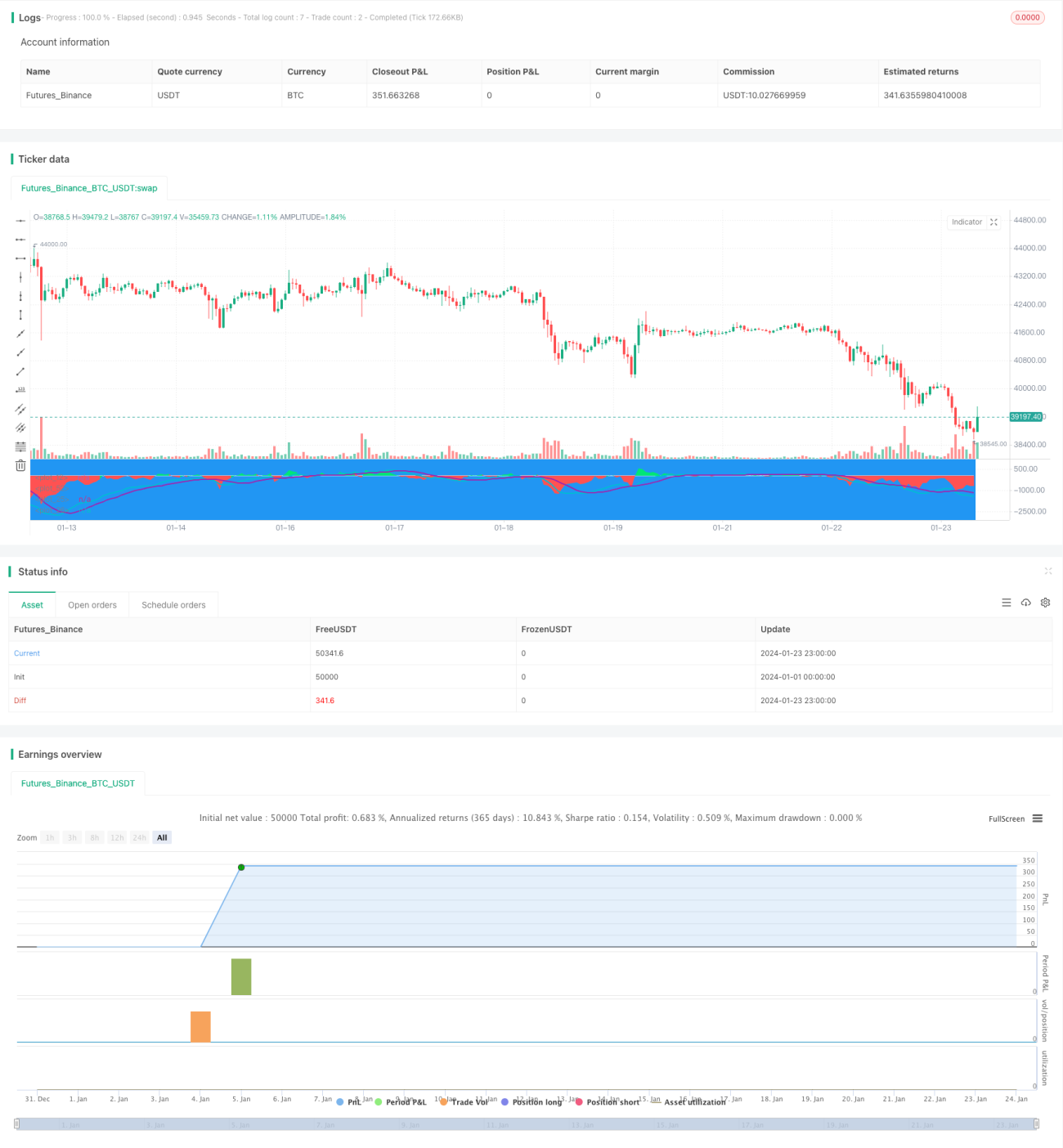

Chiến lược này là một chiến lược kết hợp dựa trên chênh lệch đường trung bình EMA và chỉ báo MACD, được sử dụng cho giao dịch ngắn hạn BTC. Nó kết hợp tín hiệu từ đường EMA và MACD để tạo ra tín hiệu mua và bán trong các điều kiện cụ thể.

Nguyên lý chiến lược

Khi chênh lệch âm và nhỏ hơn ngưỡng, đồng thời MACD xuất hiện giao cắt bearish (chết chéo), tín hiệu mua được phát ra. Khi chênh lệch dương và lớn hơn ngưỡng, đồng thời MACD xuất hiện giao cắt bullish (vàng chéo), tín hiệu bán được phát ra.

Bằng cách kết hợp tín hiệu từ chênh lệch đường EMA và chỉ báo MACD, có thể loại bỏ một số tín hiệu giả, nâng cao độ tin cậy của tín hiệu.

Phân tích ưu điểm

- Sử dụng chỉ báo kết hợp, tín hiệu đáng tin cậy hơn

- Áp dụng cài đặt chu kỳ ngắn, phù hợp với giao dịch ngắn hạn

- Có cài đặt stop loss và take profit, giúp kiểm soát rủi ro

Phân tích rủi ro

- Khi thị trường biến động mạnh, stop loss có thể bị phá vỡ

- Cần tối ưu hóa tham số để phù hợp hơn với các môi trường thị trường khác nhau

- Cần kiểm tra hiệu quả trên các loại coin và sàn giao dịch khác nhau

Hướng tối ưu hóa

- Tối ưu hóa tham số EMA và MACD để phù hợp hơn với môi trường biến động của BTC

- Thêm chiến lược mở vị thế và tăng/giảm vị thế, tối ưu hiệu quả sử dụng vốn

- Bổ sung các phương pháp stop loss như trailing stop, stop loss dao động,... để giảm rủi ro

- Kiểm tra hiệu quả trên các sàn giao dịch và loại coin khác nhau

Tổng kết

Chiến lược này tích hợp ưu điểm của cả đường trung bình và chỉ báo MACD, sử dụng tín hiệu kết hợp, có thể lọc hiệu quả các tín hiệu giả. Bằng cách tối ưu hóa tham số và chiến lược mở vị thế, có thể đạt được lợi nhuận ổn định. Tuy nhiên, cũng cần cảnh giác với rủi ro stop loss bị phá vỡ, cần kiểm tra và hoàn thiện thêm.

- 1