Chiến lược giao dịch dao động hỗ trợ kháng cự

1

Follow

1802

Followers

Tổng quan

Chiến lược này kết hợp giao cắt của RSI và chỉ báo Stochastic (STO), cùng với chiến lược tối ưu hóa trượt giá khi đóng vị thế, nhằm kiểm soát chính xác logic giao dịch và thực hiện cắt lỗ/chốt lời chính xác. Đồng thời, thông qua tối ưu hóa tín hiệu, có thể nắm bắt xu hướng tốt hơn và quản lý vốn hợp lý.

Nguyên lý chiến lược

- Chỉ báo RSI xác định vùng quá mua/quá bán, kết hợp với giao cắt vàng/tử của giá trị K và D của chỉ báo Stochastic để tạo tín hiệu giao dịch.

- Đưa vào nhận dạng phân kỳ nến (Fractal) để hỗ trợ xác định tín hiệu xu hướng, tránh giao dịch sai lầm.

- Đường trung bình SMA hỗ trợ xác định hướng xu hướng. Khi đường trung bình ngắn hạn cắt lên trên đường trung bình dài hạn, đó là tín hiệu tăng giá.

- Chiến lược trượt giá khi đóng vị thế, thiết lập giá cắt lỗ/chốt lời dựa trên phạm vi dao động giá cao nhất và thấp nhất.

Phân tích ưu điểm

- Tối ưu hóa tham số RSI, xác định tốt vùng quá mua/quá bán, tránh giao dịch sai lầm.

- Tối ưu hóa tham số chỉ báo STO, điều chỉnh độ trơn (smoothing) giúp lọc nhiễu, nâng cao chất lượng tín hiệu.

- Đưa vào phân tích kỹ thuật Heikin-Ashi để nhận dạng sự thay đổi hướng thân nến, đảm bảo độ chính xác của tín hiệu giao dịch.

- Đường trung bình SMA hỗ trợ xác định xu hướng lớn, tránh giao dịch ngược xu hướng.

- Kết hợp chiến lược trượt giá cắt lỗ/chốt lời, có thể tối đa hóa lợi nhuận cho mỗi giao dịch.

Phân tích rủi ro

- Khi thị trường chung giảm liên tục, vốn có thể đối mặt với rủi ro lớn.

- Tần suất giao dịch có thể quá cao, làm tăng chi phí giao dịch và chi phí trượt giá.

- Chỉ báo RSI dễ tạo ra tín hiệu giả, cần kết hợp với các chỉ báo khác để lọc.

Tối ưu hóa chiến lược

- Điều chỉnh tham số RSI để tối ưu hóa việc xác định quá mua/quá bán.

- Điều chỉnh tham số chỉ báo STO (độ trơn và chu kỳ) để nâng cao chất lượng tín hiệu.

- Điều chỉnh chu kỳ đường trung bình động để tối ưu hóa nhận định xu hướng.

- Đưa thêm nhiều chỉ báo kỹ thuật để nâng cao độ chính xác của tín hiệu.

- Tối ưu hóa tỷ lệ cắt lỗ/chốt lời để giảm rủi ro cho mỗi giao dịch.

Kết luận

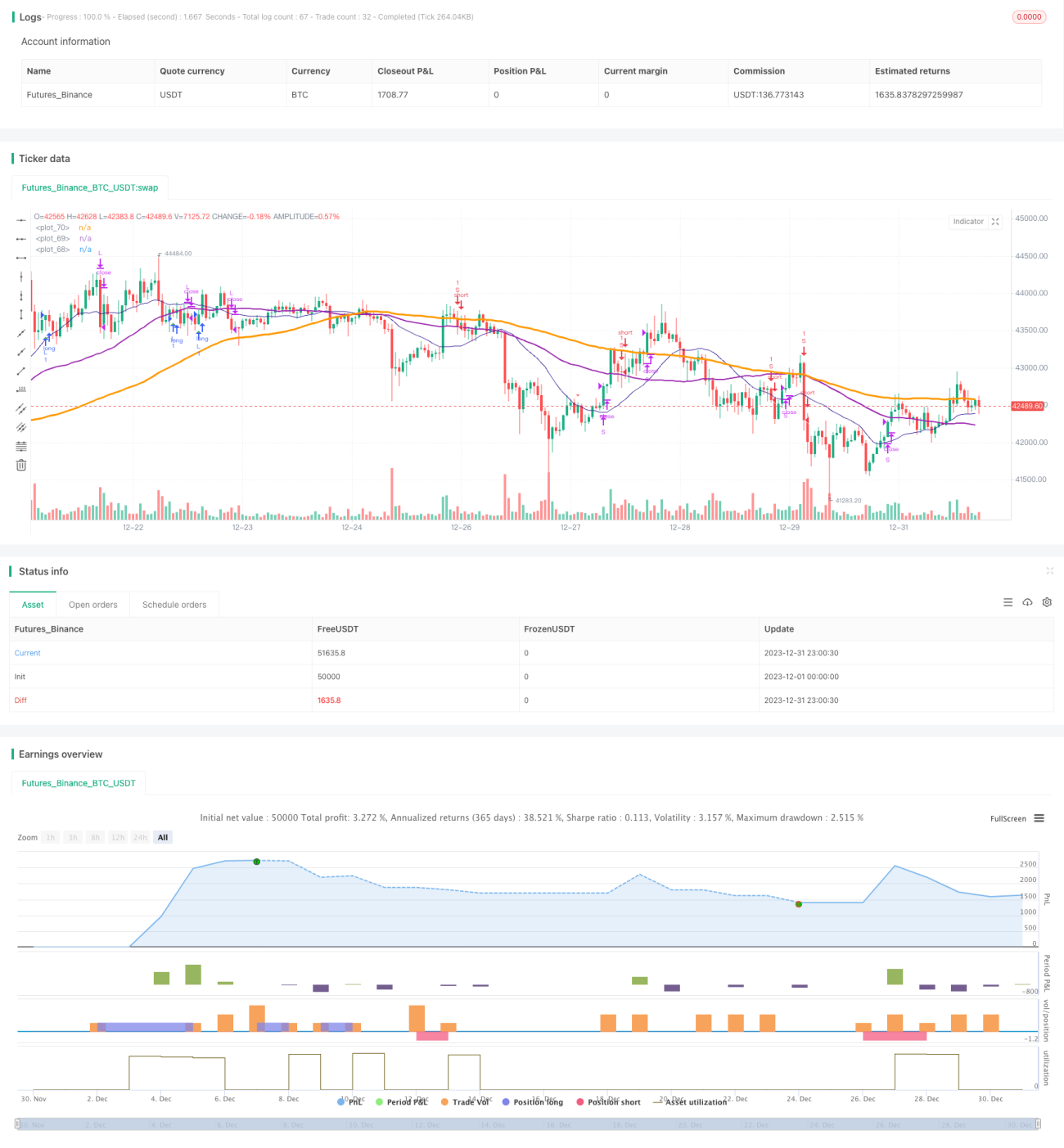

Chiến lược này tích hợp ưu điểm của nhiều chỉ báo kỹ thuật chính thống, thông qua tối ưu hóa tham số và hoàn thiện quy tắc, đã đạt được sự cân bằng giữa chất lượng tín hiệu giao dịch và cắt lỗ/chốt lời. Nó có tính tổng quát và khả năng sinh lời ổn định nhất định. Thông qua tối ưu hóa liên tục, có thể nâng cao tỷ lệ thắng và tỷ suất lợi nhuận.

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//study(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true)

strategy(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true )

smoothK = input(3, minval=1)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1