Chiến lược định lượng giao cắt đường trung bình động lượng

Tổng quan

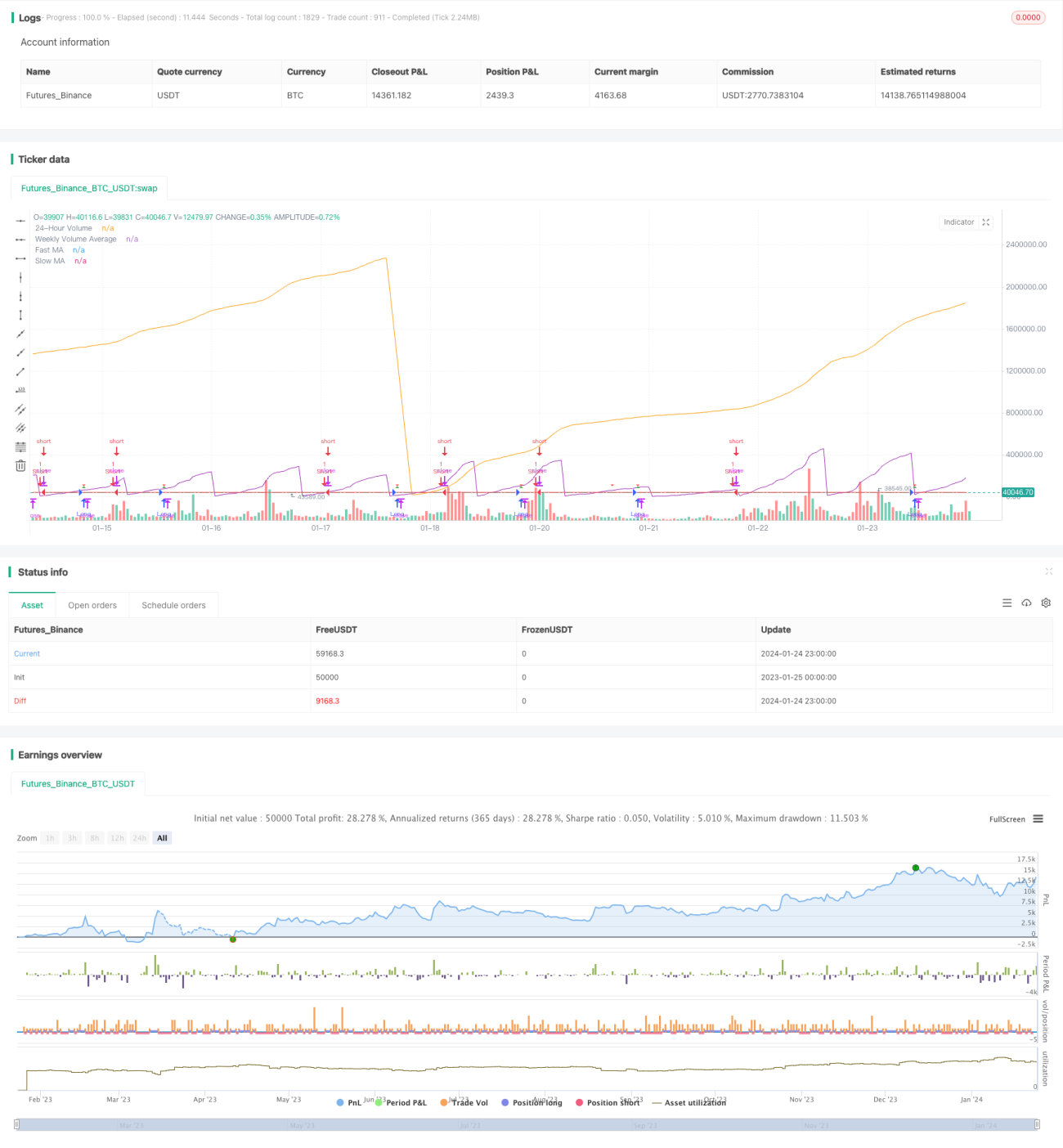

Chiến lược này kết hợp hai chỉ báo kỹ thuật chính là đường trung bình động và khối lượng giao dịch, thiết kế các quy tắc vào và thoát lệnh cho cả vị thế long và short, hình thành một chiến lược giao dịch định lượng hoàn chỉnh.

Nguyên lý chiến lược

Chỉ báo chính

- Đường trung bình động: Đường trung bình động nhanh (đường màu xanh dương) và đường trung bình động chậm (đường màu đỏ).

- Khối lượng giao dịch: Khối lượng giao dịch 24 giờ (màu tím) và khối lượng giao dịch trung bình 7 ngày (đường màu cam).

Điều kiện chiến lược

Điều kiện vào lệnh Long:

- Đường trung bình động nhanh cắt lên trên đường trung bình động chậm

- Khối lượng giao dịch 24 giờ thấp hơn 50% khối lượng giao dịch trung bình 7 ngày

Điều kiện vào lệnh Short:

Đường trung bình động nhanh cắt xuống dưới đường trung bình động chậm

Vào và thoát lệnh

Vào lệnh Long: Mở vị thế long khi thỏa mãn điều kiện vào lệnh Long

Vào lệnh Short: Mở vị thế short khi thỏa mãn điều kiện vào lệnh Short

Chốt lời và Cắt lỗ:

Hiển thị mức chốt lời và cắt lỗ sau khi mở vị thế long

Phân tích ưu điểm

- Kết hợp chỉ báo giá và chỉ báo khối lượng, tránh tín hiệu phá vỡ giả

- Quy tắc vào và thoát lệnh rõ ràng

- Có cơ chế chốt lời và cắt lỗ để kiểm soát rủi ro

Phân tích rủi ro

- Chiến lược hai đường trung bình động dễ tạo ra giao dịch thường xuyên

- Chất lượng dữ liệu khối lượng giao dịch không thể đảm bảo

- Tối ưu hóa tham số có nguy cơ tối ưu quá mức

Phương pháp cải thiện:

- Điều chỉnh tham số đường trung bình phù hợp, giảm tần suất giao dịch

- Kết hợp nhiều nguồn dữ liệu hơn để xác thực tín hiệu định lượng

- Kiểm tra backtest nghiêm ngặt, tránh tối ưu quá mức

Hướng tối ưu hóa

- Thêm các chỉ báo khác để lọc tín hiệu

- Điều chỉnh động mức chốt lời và cắt lỗ

- Phân tích đa khung thời gian, nâng cao độ ổn định

Tổng kết

Chiến lược này tích hợp chỉ báo đường trung bình động và chỉ báo khối lượng giao dịch, thông qua cơ chế xác nhận kép để thiết kế một chiến lược giao dịch định lượng hoàn chỉnh. Có ưu điểm như điều kiện vào lệnh rõ ràng, có chốt lời và cắt lỗ, đơn giản và dễ vận hành. Đồng thời cũng cần phòng ngừa vấn đề giao dịch thường xuyên của chiến lược hai đường trung bình, chú ý đến chất lượng dữ liệu khối lượng giao dịch, tránh tối ưu quá mức tham số. Bước tiếp theo thực hiện tối ưu hóa đa chỉ báo, chốt lời cắt lỗ động và phân tích đa khung thời gian.

- 1