Chiến lược theo dõi xu hướng xuyên suốt thị trường dựa trên cắt lỗ động hai chiều theo đường trung bình EMA

1

Follow

1802

Followers

Tổng quan

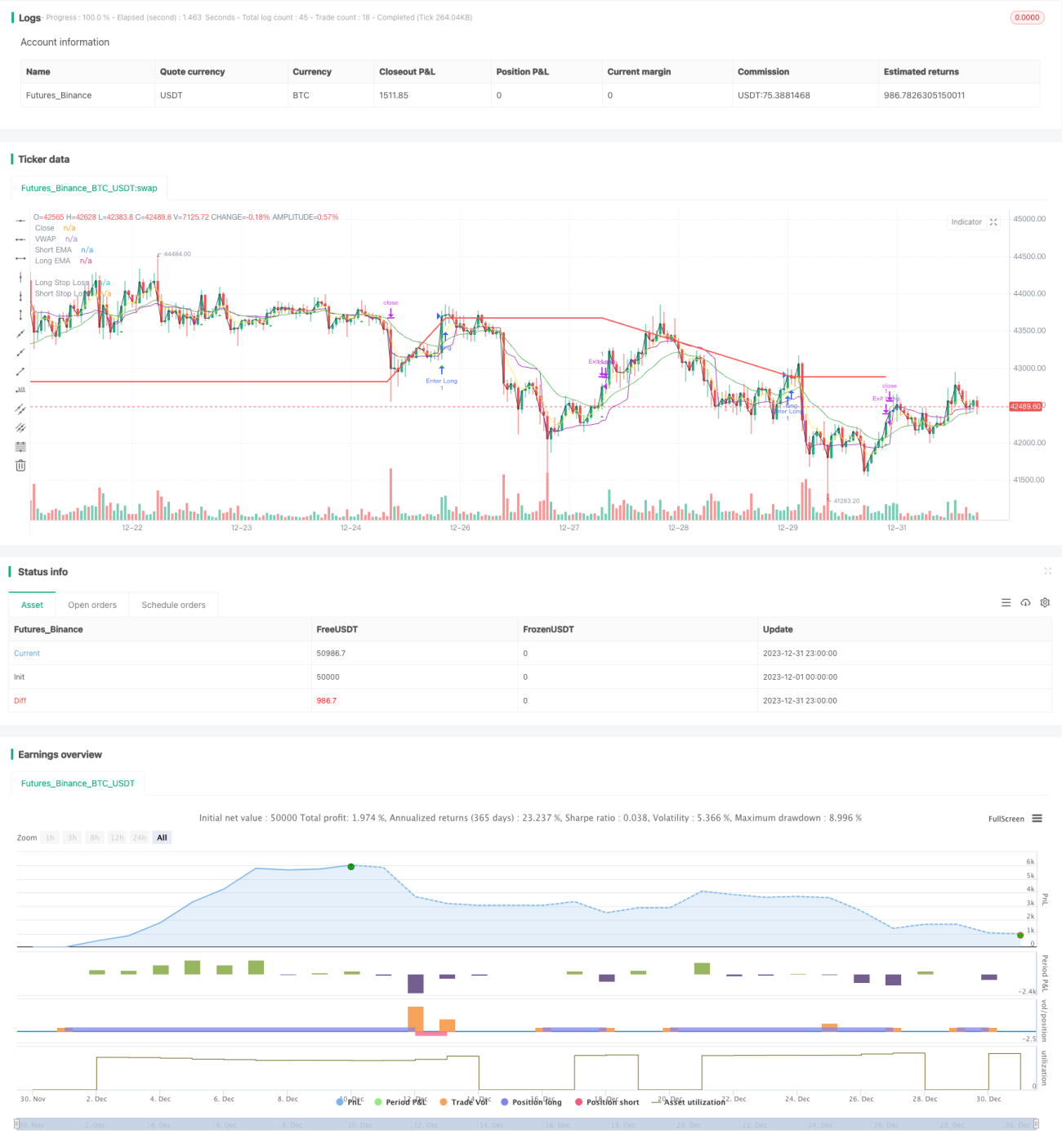

Chiến lược này dựa trên giao cắt vàng và giao cắt chết của đường trung bình EMA để theo dõi hai chiều, đồng thời thiết lập các mức stop loss động cho vị thế long và short, nhằm nắm bắt xu hướng thị trường.

Nguyên lý chiến lược

- Tính đường EMA nhanh (5 ngày) và đường EMA chậm (20 ngày)

- Khi đường nhanh cắt lên trên đường chậm, vào lệnh long; khi đường nhanh cắt xuống dưới đường chậm, vào lệnh short.

- Sau khi vào lệnh long, đặt mức stop loss động là giá vào lệnh * (1 - tỷ lệ stop loss vị thế long); sau khi vào lệnh short, đặt mức stop loss động là giá vào lệnh * (1 + tỷ lệ stop loss vị thế short).

- Khi giá chạm mức stop loss tương ứng, thoát lệnh stop loss.

Phân tích ưu điểm

- Đường trung bình EMA có khả năng theo dõi xu hướng tốt, sự giao cắt hai chiều tạo thành tín hiệu thời gian, có hiệu quả khóa chặt cơ hội xu hướng.

- Tính toán stop loss động, theo thị trường sau khi có lợi nhuận, có thể khóa lợi nhuận xu hướng ở mức tối đa.

- Sử dụng vwap làm điều kiện lọc bổ sung, tránh bị mắc kẹt, nâng cao chất lượng tín hiệu.

Phân tích rủi ro

- Chiến lược thuần xu hướng, dễ bị mắc kẹt khi thị trường dao động.

- Stop loss quá rộng có thể gây ra thua lỗ lớn hơn.

- Độ trễ của tín hiệu từ đường EMA có thể bỏ lỡ điểm vào lệnh tốt nhất.

Có thể tối ưu hóa bằng cách sử dụng ATR để quản lý rủi ro, cải thiện chiến lược stop loss ngắn hạn, hoặc kết hợp với các chỉ báo khác để lọc nhiễu giao dịch.

Hướng tối ưu hóa

- Kết hợp các chỉ báo stop loss động như ATR hoặc DONCH, thiết lập mức stop loss phù hợp hơn với thị trường.

- Thêm các chỉ báo kỹ thuật khác để lọc tín hiệu, như MACD, KDJ, v.v., giảm tín hiệu sai.

- Tối ưu hóa tham số, tìm kiếm tổ hợp độ dài đường trung bình nhanh/chậm tối ưu.

- Có thể thử phương pháp machine learning để tìm tham số tối ưu.

Kết luận

Nhìn chung, đây là một chiến lược theo dõi xu hướng rất điển hình. EMA kép tạo ra giao cắt vàng và giao cắt chết, stop loss động, có hiệu quả khóa lợi nhuận xu hướng. Đồng thời cũng tồn tại rủi ro trễ và rủi ro stop loss quá rộng. Bằng cách tối ưu hóa tham số, quản lý rủi ro, lọc tín hiệu, có thể đạt được hiệu suất chiến lược tốt hơn.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1