Chiến lược hai đường trung bình động theo lý thuyết Chan

Tổng quan

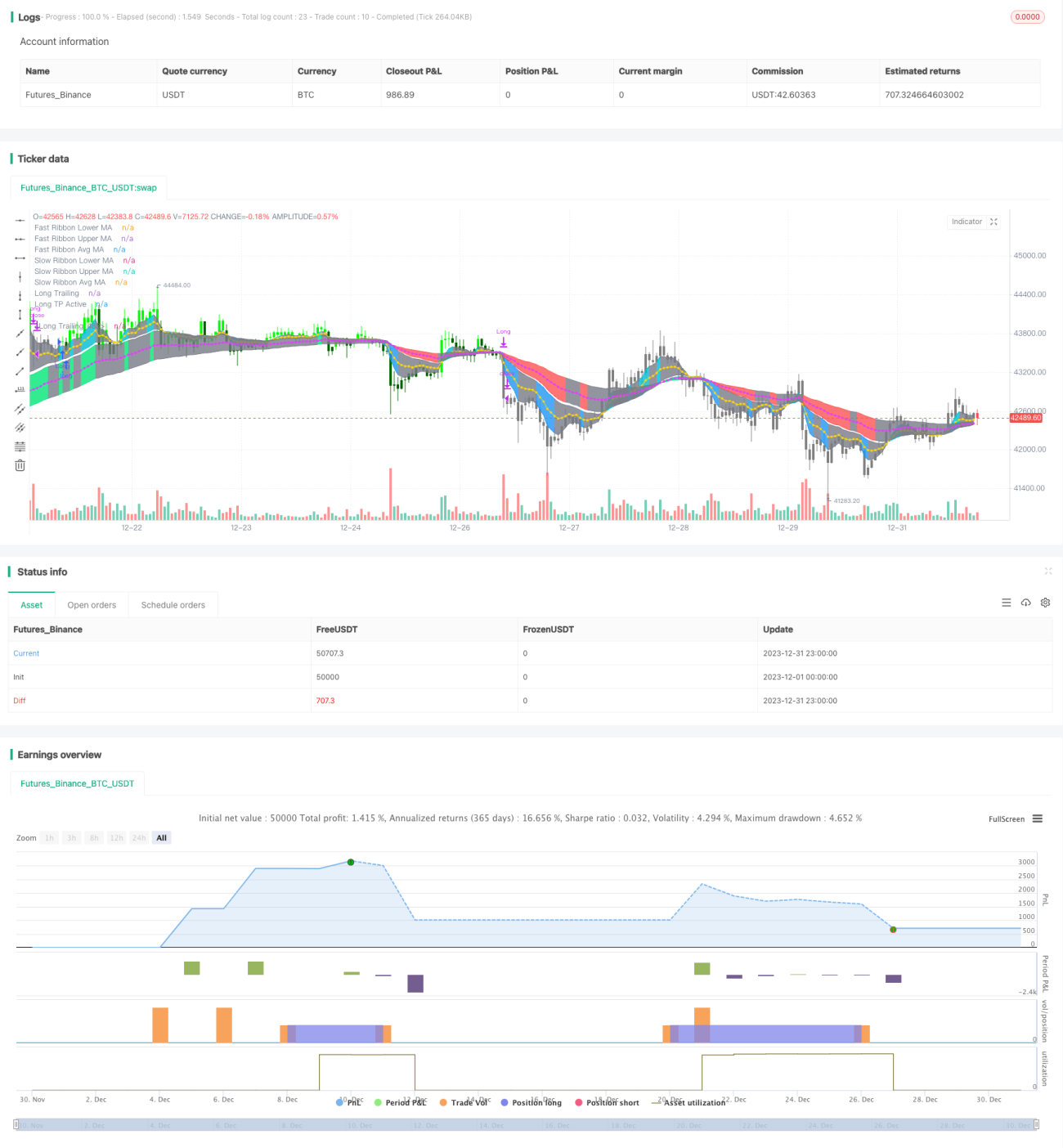

Chiến lược song đường trung bình động dựa trên lý thuyết缠论 (Chan Theory) là một chiến lược theo dõi xu hướng. Nó xây dựng nhóm đường trung bình động nhanh và nhóm đường trung bình động chậm bằng cách tính toán hai bộ đường trung bình động, đồng thời kết hợp với mối quan hệ giữa giá và đường trung bình để xác định hướng xu hướng.

Khi đường nhanh cắt lên trên đường chậm là tín hiệu tăng giá. Khi đường nhanh cắt xuống dưới đường chậm là tín hiệu giảm giá. Chiến lược này kết hợp hướng của đường trung bình nhanh và chậm, số lượng nến phá vỡ giá và các điều kiện khác để xác định thời điểm vào và thoát lệnh cụ thể.

Nguyên lý chiến lược

Chiến lược song đường trung bình động dựa trên lý thuyết缠论 xác định các tiêu chí xu hướng ngắn hạn và dài hạn thông qua việc tính toán hai bộ đường trung bình động. Cụ thể, chiến lược định nghĩa:

- Nhóm đường trung bình động nhanh, bao gồm đường trung bình động dải dưới nhanh và đường trung bình động dải trên nhanh, đại diện cho xu hướng ngắn hạn;

- Nhóm đường trung bình động chậm, bao gồm đường trung bình động dải dưới chậm và đường trung bình động dải trên chậm, đại diện cho xu hướng dài hạn.

Chiến lược sử dụng mối quan hệ giá giữa nhóm đường trung bình nhanh và nhóm đường trung bình chậm để đánh giá tính hợp lý của xu hướng ngắn hạn và dài hạn, cũng như thời điểm vào và thoát lệnh cụ thể.

Điều kiện vào lệnh như sau:

- Khi đường trung bình dải trên nhanh đột phá lên trên đường trung bình dải trên chậm từ 2 cây nến trở lên, vào lệnh mua (long).

- Khi đường trung bình dải dưới nhanh đột phá xuống dưới đường trung bình dải dưới chậm từ 2 cây nến trở lên, vào lệnh bán (short).

Điều kiện thoát lệnh như sau:

- Trong thời gian giữ vị thế mua, khi đường trung bình nhanh cắt xuống dưới đường trung bình chậm, thoát lệnh mua.

- Trong thời gian giữ vị thế bán, khi đường trung bình nhanh cắt lên trên đường trung bình chậm, thoát lệnh bán.

Ngoài ra, chiến lược còn thiết lập các chức năng như chốt lời (take profit), cắt lỗ (stop loss), cắt lỗ động (trailing stop) để kiểm soát rủi ro.

Phân tích ưu điểm

Các ưu điểm chính của chiến lược song đường trung bình động dựa trên lý thuyết缠论 bao gồm:

- Thông qua phán đoán bằng hai đường trung bình động, có thể lọc hiệu quả nhiễu thị trường, khóa hướng xu hướng.

- Kết hợp đường trung bình nhanh/chậm và mối quan hệ giá, độ tin cậy của tín hiệu cao.

- Các quy tắc chiến lược đơn giản, rõ ràng, dễ hiểu và thực hiện, phù hợp với giao dịch định lượng.

- Tích hợp sẵn các biện pháp kiểm soát rủi ro như chốt lời, cắt lỗ, cắt lỗ động, có thể kiểm soát hiệu quả rủi ro giao dịch.

Phân tích rủi ro

Chiến lược song đường trung bình động dựa trên lý thuyết缠论 cũng tồn tại một số rủi ro, chủ yếu thể hiện ở:

- Trong thị trường dao động (sideways), có thể tạo ra tín hiệu giả, dẫn đến các giao dịch không cần thiết.

- Hệ thống đường trung bình động phản ứng chậm với các sự kiện đột xuất (như tin tức xấu/tốt quan trọng), có thể gây ra thua lỗ lớn.

- Cắt lỗ động có thể bị phá vỡ trong điều kiện thị trường cụ thể, làm mở rộng thua lỗ.

Để kiểm soát các rủi ro trên, có thể cải thiện bằng cách tối ưu tham số đường trung bình động, hoặc kết hợp với các chỉ báo khác để lọc.

Hướng tối ưu hóa

Chiến lược song đường trung bình động dựa trên lý thuyết缠论 có thể được tối ưu hóa từ các khía cạnh sau:

- Tối ưu tham số đường trung bình động, điều chỉnh chu kỳ đường trung bình, thích ứng với các khung thời gian thị trường khác nhau.

- Thêm các chỉ bộ lọc (filter) khác, hình thành chiến lược kết hợp đa chỉ báo, nâng cao độ chính xác của tín hiệu.

- Tối ưu cài đặt cắt lỗ, chốt lời, thiết lập ngưỡng drawdown, kiểm soát thua lỗ tối đa.

- Đưa vào mô hình học máy dự đoán xu hướng, hỗ trợ xác định thời điểm vào lệnh.

Tổng kết

Nhìn chung, chiến lược song đường trung bình động dựa trên lý thuyết缠论 là một chiến lược theo dõi xu hướng rất thiết thực. Các quy tắc phán đoán đơn giản, logic rõ ràng, kiểm soát rủi ro thông qua hệ thống hai đường trung bình động, cơ sở lý thuyết vững chắc. Bước tiếp theo có thể cải tiến từ nhiều khía cạnh như tối ưu hóa tham số, kiểm soát rủi ro, v.v., để nâng cao hơn nữa khả năng sinh lời và tính ổn định của chiến lược.

- 1