Chiến lược theo dõi xu hướng dựa trên đa chỉ báo

Tổng quan

Chiến lược này kết hợp nhiều chỉ báo để xác định xu hướng, đồng thời thiết lập cắt lỗ theo dõi xu hướng nhằm khóa lợi nhuận. Chủ yếu sử dụng các chỉ báo như Bollinger Bands, RSI, ADX để xác định thời điểm vào lệnh, cùng với ATR và Bollinger Bands để cắt lỗ.

Nguyên lý chiến lược

Chiến lược xác định điểm vào lệnh dựa trên Bollinger Bands, RSI và ADX. Khi giá tiến gần dải dưới của Bollinger Bands và RSI dưới 30, thị trường được coi là quá bán, vào lệnh mua; khi giá tiến gần dải trên của Bollinger Bands và RSI trên 70, thị trường được coi là quá mua, vào lệnh bán. Ngoài ra, nếu ADX trên 25, xu hướng được xác định là đã hình thành, lúc này tín hiệu mua/bán sẽ hiệu quả hơn.

Sau khi mở vị thế, chiến lược sử dụng chỉ báo ATR và dải trên/dưới của Bollinger Bands để cắt lỗ. Cụ thể, ATR được dùng cho mức cắt lỗ tối đa – khi giá chạm mức cắt lỗ tối đa thì đóng lệnh; dải trên/dưới của Bollinger Bands được dùng để thiết lập điểm cắt lỗ theo dõi, cập nhật giá cắt lỗ theo dõi theo diễn biến giá thực tế.

Phân tích ưu điểm

Chiến lược này kết hợp nhiều chỉ báo để nhận diện xu hướng hiệu quả; sử dụng cơ chế cắt lỗ để khóa lợi nhuận, giảm thiểu rủi ro thua lỗ, là một chiến lược tương đối vững chắc. Các ưu điểm cụ thể:

- Sử dụng Bollinger Bands để xác định tình trạng quá mua/quá bán, có thể phát hiện cơ hội đảo chiều.

- Kết hợp chỉ báo RSI giúp tăng độ chính xác của tín hiệu.

- Chỉ báo ADX xác định xu hướng hình thành, đảm bảo hướng giao dịch đúng đắn.

- Cắt lỗ theo dõi bằng ATR và Bollinger Bands giúp khóa lợi nhuận tối đa.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

- Dùng nhiều chỉ báo, dễ xảy ra tối ưu hóa tham số quá mức.

- Khi biên độ Bollinger Bands rộng, tín hiệu quá mua/quá bán kém hiệu quả.

- Theo dõi cắt lỗ không phù hợp có thể dẫn đến thua lỗ gia tăng.

Để đối phó với các rủi ro này, ta có thể thực hiện các biện pháp sau:

- Kết hợp tối ưu nhiều bộ tham số, tránh tối ưu quá mức.

- Điều chỉnh tham số Bollinger Bands dựa trên biến động thị trường.

- Kiểm tra khoảng cách cắt lỗ để đảm bảo chịu được biến động bình thường.

Hướng tối ưu hóa

Chiến lược này cũng có thể được tối ưu hóa theo các hướng sau:

- Thêm kiểm soát vị thế, điều chỉnh quy mô vị thế dựa trên hệ số cắt lỗ.

- Thêm mô-đun quản lý vốn (money management), kiểm soát chặt chẽ mức thua lỗ tối đa mỗi lệnh.

- Kiểm tra các chỉ báo cắt lỗ khác như DMI, Envelopes, v.v.

- Thêm mô hình học máy để dự đoán xác suất xu hướng, nâng cao hiệu quả.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược bám xu hướng tương đối vững chắc. Bằng cách kết hợp nhiều chỉ báo để xác định hướng xu hướng và sử dụng các biện pháp cắt lỗ để kiểm soát rủi ro, có thể đạt được tỷ suất lợi nhuận tốt. Chúng tôi cũng đã đề xuất một số hướng tối ưu hóa, nếu được tối ưu thêm sẽ đạt được hiệu quả tốt hơn.

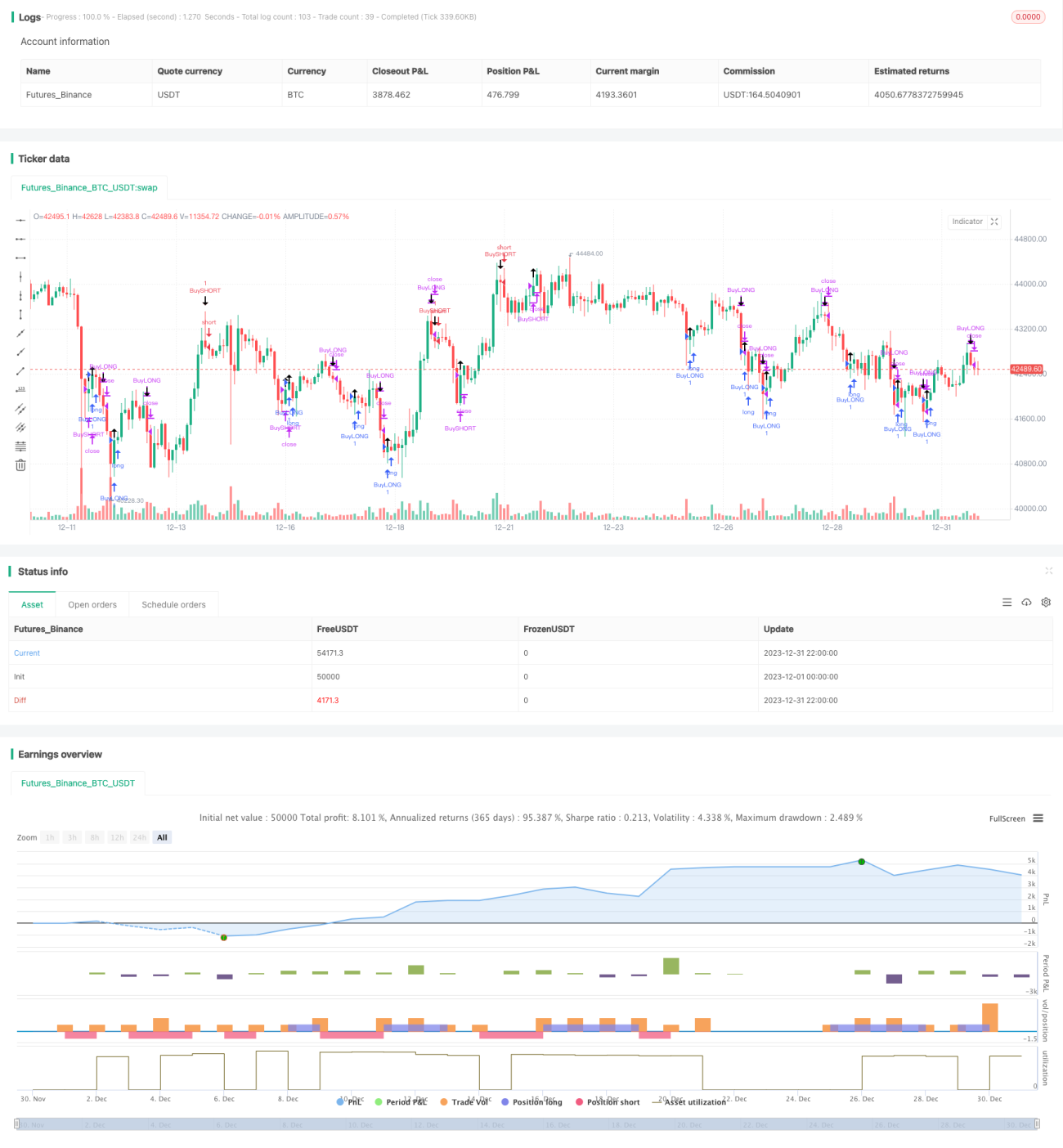

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// THIS SCRIPT IS MEANT TO ACCOMPANY COMMAND EXECUTION BOTS

// THE INCLUDED STRATEGY IS NOT MEANT FOR LIVE TRADING

// THIS STRATEGY IS PURELY AN EXAMLE TO START EXPERIMENTATING WITH YOUR OWN IDEAS- 1