Chiến lược bám động lượng đa khung thời gian

Tổng quan

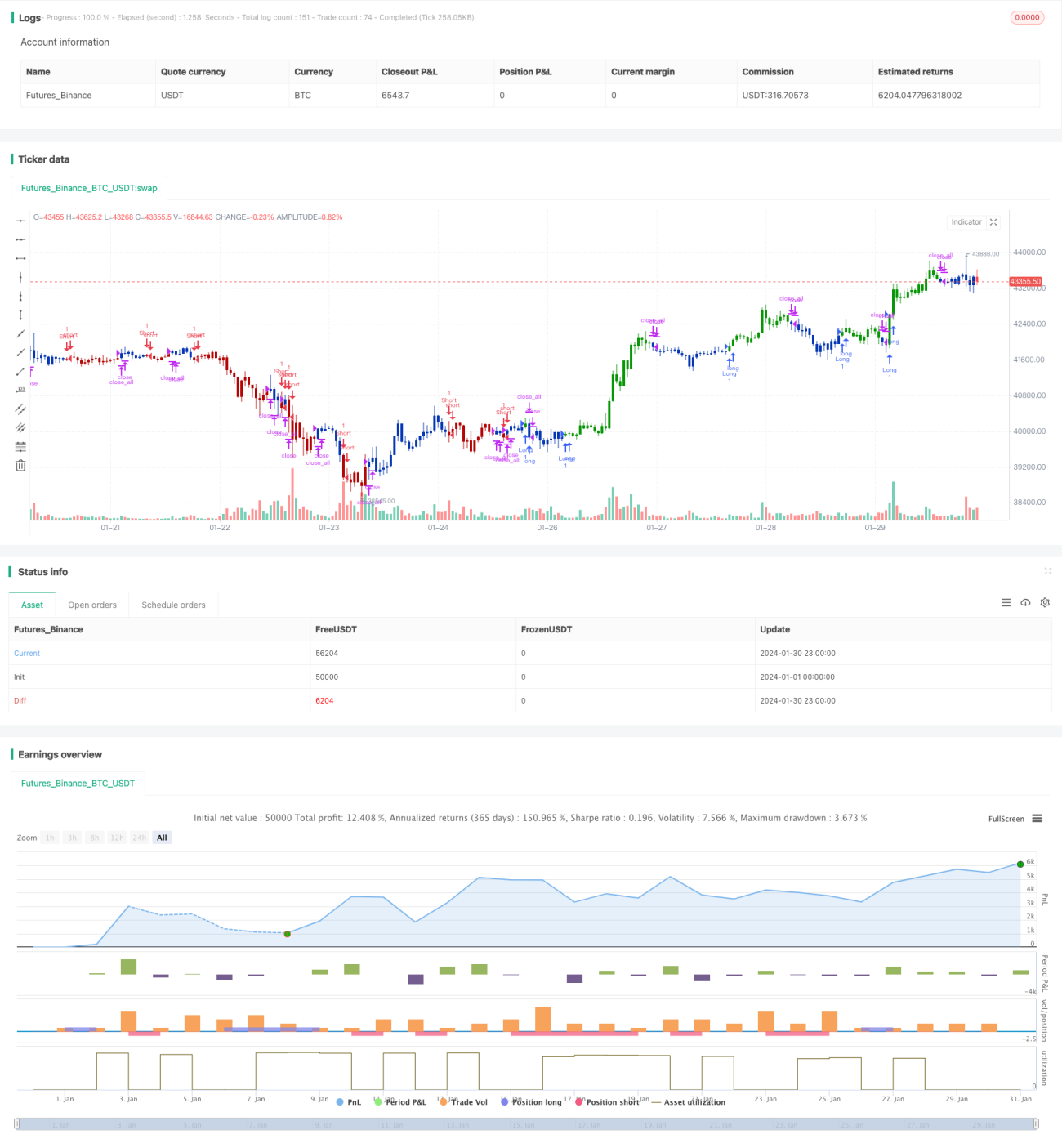

Chiến lược này kết hợp chỉ báo 123 Reversal và MACD để theo dõi động lượng đa khung thời gian. 123 Reversal xác định điểm đảo chiều ngắn hạn, MACD xác định xu hướng trung và dài hạn, sự kết hợp này cho phép nắm bắt tín hiệu mua/bán vừa đảo chiều ngắn hạn vừa xác nhận xu hướng trung dài hạn.

Nguyên lý chiến lược

Chiến lược bao gồm hai phần:

-

Phần 123 Reversal: Khi hai nến hiện tại tạo đỉnh/đáy và Stochastic (chỉ báo ngẫu nhiên) ở dưới/trên 50, sẽ phát tín hiệu mua/bán.

-

Phần MACD: Khi đường nhanh cắt lên đường chậm phát tín hiệu mua, đường nhanh cắt xuống đường chậm phát tín hiệu bán.

Cuối cùng kết hợp cả hai, tức là khi 123 Reversal xuất hiện đồng thời MACD cũng có tín hiệu cùng chiều, thì phát tín hiệu cuối cùng.

Phân tích ưu điểm

Chiến lược này kết hợp đảo chiều ngắn hạn và xu hướng trung dài hạn, có thể nắm bắt xu hướng trung dài hạn trong biến động ngắn hạn, nhờ đó đạt tỷ lệ thắng cao hơn. Đặc biệt trong thị trường đi ngang, có thể lọc bớt nhiễu nhờ 123 Reversal, nâng cao độ ổn định.

Ngoài ra, bằng cách điều chỉnh tham số, có thể cân bằng tỷ lệ tín hiệu đảo chiều và tín hiệu xu hướng, thích ứng với các môi trường thị trường khác nhau.

Phân tích rủi ro

Chiến lược này có độ trễ thời gian nhất định, đặc biệt khi sử dụng MACD chu kỳ dài, có thể bỏ lỡ biến động ngắn hạn. Hơn nữa, bản thân tín hiệu đảo chiều đã có tính ngẫu nhiên nhất định, dễ bị mắc kẹt.

Có thể rút ngắn chu kỳ MACD hoặc thêm cắt lỗ để kiểm soát rủi ro.

Hướng tối ưu

Chiến lược có thể tối ưu từ các hướng sau:

-

Điều chỉnh tham số 123 Reversal để tối ưu hiệu quả đảo chiều

-

Điều chỉnh tham số MACD để tối ưu nhận định xu hướng

-

Thêm các chỉ báo phụ trợ khác để lọc, nâng cao hiệu quả

-

Thêm chiến lược cắt lỗ để kiểm soát rủi ro

Tổng kết

Chiến lược này tích hợp nhiều tham số và chỉ báo kỹ thuật đa khung thời gian, thông qua theo dõi động lượng đa khung thời gian, cân bằng ưu điểm của giao dịch đảo chiều và giao dịch xu hướng. Có thể điều chỉnh tham số để cân bằng hiệu quả, và có thể đưa thêm các chỉ báo hoặc cắt lỗ để tối ưu hóa, là một ý tưởng chiến lược rất tiềm năng.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 28/01/2021

// This is combo strategies for get a cumulative signal. - 1