Chiến lược sóng ba đường trung bình phân tích kiên nhẫn những thông tin quý giá ẩn chứa trong nến K

Tổng quan

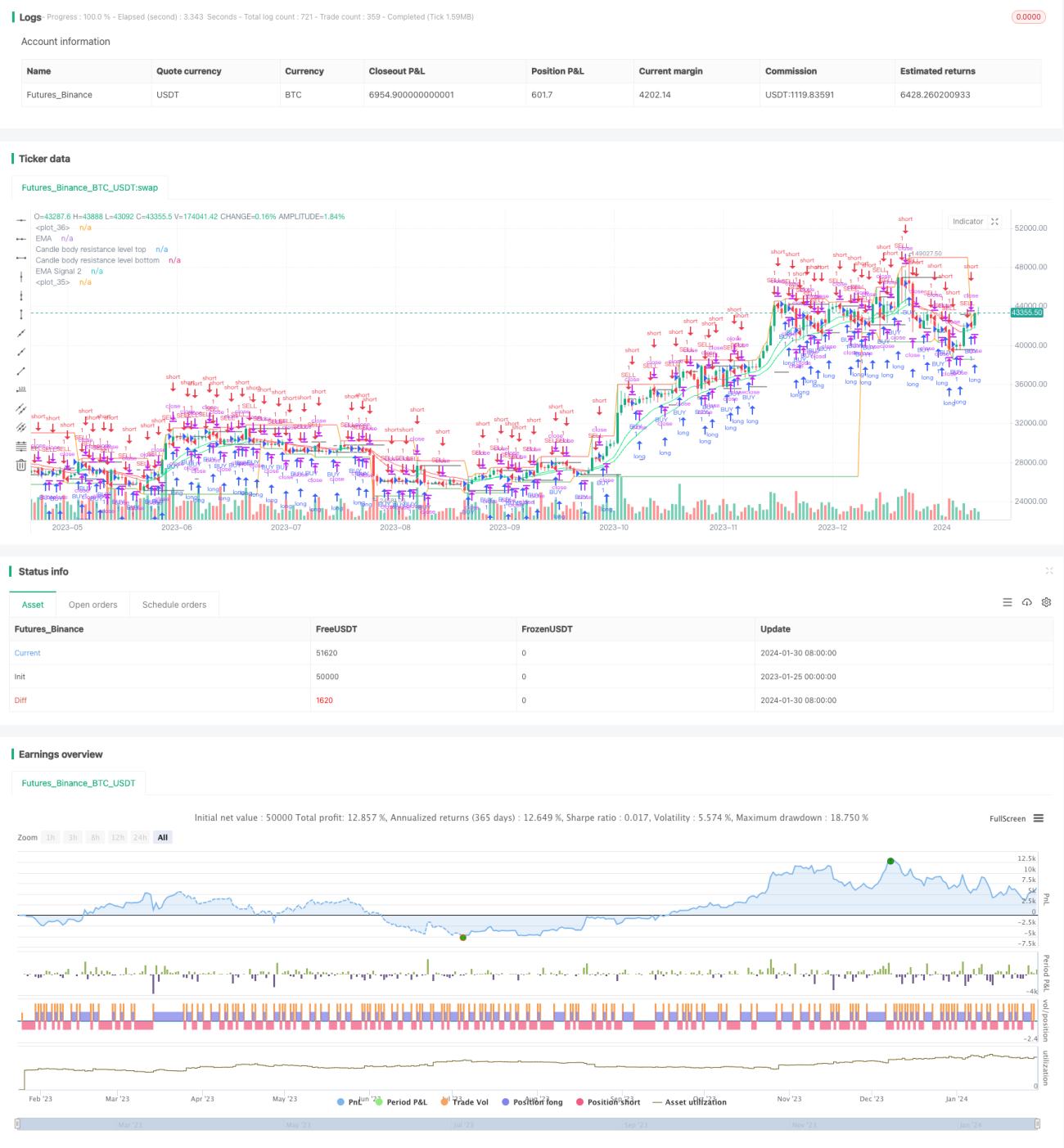

Chiến lược giao dịch sóng ba đường trung bình động sử dụng nhiều chỉ báo đường trung bình động, thông qua phân tích chuyên sâu các nến K để khám phá quy luật ẩn giấu trong biến động giá, thực hiện giao dịch chênh lệch giá với rủi ro thấp.

Nguyên lý chiến lược

Chiến lược này chồng nhiều nhóm chỉ báo EMA lên nền tảng dải Bollinger, xây dựng kênh giá và phát hiện quy luật biến động giá. Cụ thể:

- Sử dụng chỉ báo BodyResistanceChannel để vẽ các mức kháng cự của thân nến.

- Sử dụng chỉ báo Support/Resistance để vẽ các mức hỗ trợ và kháng cự nhiều ngày.

- Sử dụng hệ thống hai EMA để xác định xu hướng giá.

- Sử dụng chỉ báo đường trung bình Hull để làm mịn đường cong giá.

Trên cơ sở đó, kết hợp nhận dạng mô hình để xác định cơ hội đảo chiều và xây dựng chiến lược giao dịch chênh lệch giá.

Phân tích ưu điểm

Chiến lược này có các ưu điểm sau:

- Sử dụng nhiều nhóm EMA để xây dựng kênh giá, có thể xác định rõ hướng đi của biến động giá.

- Áp dụng chỉ báo đường trung bình Hull giúp làm mịn hiệu quả việc xác định điểm phá vỡ giá.

- Kết hợp mô hình đảo chiều và chỉ báo kênh, thực hiện giao dịch với xác suất cao và rủi ro thấp.

- Xây dựng hệ thống chỉ báo đa tầng, tín hiệu giao dịch ổn định và đáng tin cậy.

Phân tích rủi ro

Chiến lược này cũng tồn tại các rủi ro sau:

- Rủi ro kênh giá bị phá vỡ gây thua lỗ lớn. Giải pháp cụ thể là sử dụng trailing stop để giảm thiểu tổn thất mỗi lệnh.

- Rủi ro nhận dạng sai mô hình đảo chiều dẫn đến tín hiệu sai. Giải pháp cụ thể là tối ưu tham số, nâng cao độ chính xác của nhận dạng mô hình.

- Rủi ro tham số chỉ báo không phù hợp khiến chất lượng tín hiệu giao dịch giảm sút. Giải pháp cụ thể là kiểm tra tối ưu đa tổ hợp tham số.

Hướng tối ưu

Các hướng tối ưu chính của chiến lược này bao gồm:

- Tối ưu tổ hợp chu kỳ tham số EMA để chỉ báo phù hợp hơn với đặc điểm thị trường.

- Điều chỉnh vị trí stop loss, đảm bảo lợi nhuận đồng thời giảm thiểu tối đa rủi ro thua lỗ mỗi lệnh.

- Bổ sung mô-đun điều chỉnh vị thế động dựa trên biến động, kiểm soát rủi ro hiệu quả.

- Tận dụng công nghệ học sâu để khai thác thêm nhiều quy luật giá, nâng cao chất lượng tín hiệu.

Tổng kết

Chiến lược giao dịch sóng ba đường trung bình động khai thác sâu quy luật biến động giá, ổn định và hiệu quả, đáng để ứng dụng lâu dài và tiếp tục tối ưu. Đầu tư cần lý trí và kiên nhẫn, giao dịch từng bước mới là chìa khóa thành công.

- 1