Chiến lược giao dịch dựa trên đường trung bình động giá

Tổng quan

Ý tưởng cốt lõi của chiến lược này là dựa trên sự di chuyển của giá trung bình để tạo ra tín hiệu giao dịch. Nó kết hợp ba chỉ báo SuperTrend với các thông số khác nhau và thiết lập nhiều phương pháp cắt lỗ như cắt lỗ ATR, cắt lỗ neo, cắt lỗ phần trăm và cắt lỗ điểm.

Ưu điểm của chiến lược là sử dụng hệ thống đa SuperTrend để nâng cao độ chính xác của tín hiệu, đồng thời cung cấp thiết lập cắt lỗ linh hoạt.

Nguyên lý chiến lược

-

Tính toán ba bộ chỉ báo SuperTrend: Đường SuperTrend được tính dựa trên tích của chỉ báo ATR và giá trung bình. Khi giá vượt lên trên đường SuperTrend là tín hiệu tăng giá, khi giá phá vỡ xuống dưới đường SuperTrend là tín hiệu giảm giá.

-

Sử dụng dải trên và dải dưới của chỉ báo Bollinger Bands để đánh giá sự phá vỡ giá. Phá vỡ dải trên của Bollinger Bands là tín hiệu tăng giá, phá vỡ dải dưới là tín hiệu giảm giá.

-

Kết hợp tín hiệu mua bán của ba bộ chỉ báo SuperTrend để xác định điều kiện vào lệnh mua (long) và bán (short).

-

Thiết lập nhiều phương pháp cắt lỗ như cắt lỗ ATR, cắt lỗ neo, cắt lỗ phần trăm và cắt lỗ điểm để quản lý rủi ro.

-

Dựa vào giá trị của chỉ báo ATR để quyết định có vào thị trường hay không. Điều này có thể dùng để lọc các tín hiệu sai trong môi trường biến động thấp.

Ưu điểm chiến lược

-

Kết hợp nhiều bộ thông số khác nhau cho các chỉ báo SuperTrend có thể nâng cao độ chính xác của tín hiệu.

-

Sử dụng chỉ báo Bollinger Bands để đánh giá xem giá có thực sự phá vỡ dải trên/dưới hay không, tránh các phá vỡ giả.

-

Cung cấp nhiều phương pháp cắt lỗ để quản lý rủi ro, tối đa hóa việc tránh các khoản lỗ vượt quá khả năng chịu đựng.

-

Sử dụng giá trị chỉ báo ATR để kiểm soát việc có vào thị trường hay không, có thể lọc các tín hiệu gây nhầm lẫn.

Rủi ro chiến lược

-

Việc kết hợp nhiều chỉ báo để xác định thời điểm vào lệnh có thể bỏ lỡ một số cơ hội tốt.

-

Thiết lập phương pháp cắt lỗ không phù hợp có thể gây ra tổn thất vượt quá mong đợi.

-

Thiết lập thông số Bollinger Bands không đúng cũng có thể khiến tín hiệu bị trễ.

-

Thiết lập điều kiện lọc chỉ báo ATR quá nghiêm ngặt cũng sẽ khiến nhiều tín hiệu bị lọc bỏ.

Hướng tối ưu hóa chiến lược

-

Điều chỉnh thông số chu kỳ ATR của chỉ báo SuperTrend để tối ưu độ nhạy của chỉ báo.

-

Thử nghiệm các loại giá trung bình khác nhau làm nguồn đầu vào cho chỉ báo SuperTrend, ví dụ như đường trung bình động trọng số (WMA).

-

Tối ưu thông số Bollinger Bands để nó phản ứng nhanh hơn với xu hướng thực của giá.

-

Kết hợp đặc điểm biến động của thị trường để điều chỉnh giới hạn thông số của bộ lọc chỉ báo ATR.

-

Kiểm tra tỷ suất lợi nhuận trong các điều kiện cắt lỗ khác nhau thông qua backtest để tìm ra điểm cắt lỗ tối ưu.

Tổng kết

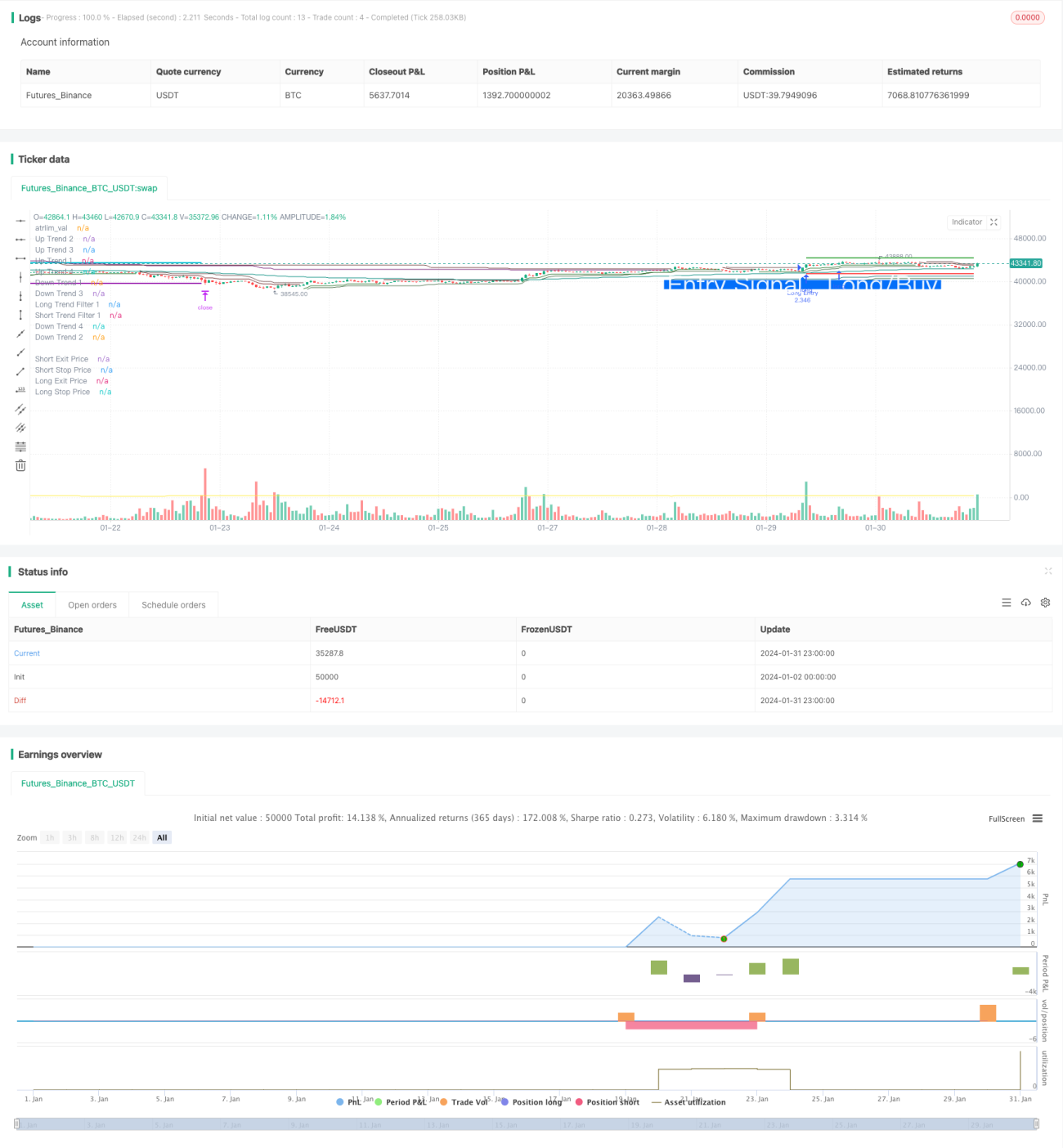

Chiến lược này kết hợp nhiều chỉ báo để lọc và xác định tín hiệu, ở một mức độ nhất định đã lọc bỏ một phần nhiễu. Đồng thời cung cấp cơ chế cắt lỗ linh hoạt để kiểm soát rủi ro. Bằng cách điều chỉnh thông số, có thể đạt được hiệu suất chiến lược tốt hơn. Tuy nhiên, việc xác định bằng nhiều chỉ báo cũng có thể dẫn đến bỏ lỡ cơ hội. Nhìn chung, chiến lược này phù hợp với đầu tư trung và dài hạn, có thể đạt được lợi nhuận đầu tư ổn định.

/*backtest

start: 2024-01-02 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version=5

// @strategy_alert_message {{strategy.order.comment}}

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © TradeSmart22- 1