Chiến lược chốt lời và cắt lỗ dựa trên ba đường trung bình động hàm mũ

Tổng quan

Chiến lược chốt lời cắt lỗ dựa trên ba đường trung bình động hàm mũ là một chiến lược giao dịch theo xu hướng, sử dụng ba đường trung bình động hàm mũ với các chu kỳ khác nhau để vào và thoát lệnh. Đồng thời, chiến lược này sử dụng chỉ số Dải biên độ thực trung bình (ATR) để thiết lập các mức chốt lời và cắt lỗ, qua đó quản lý rủi ro.

Nguyên lý chiến lược

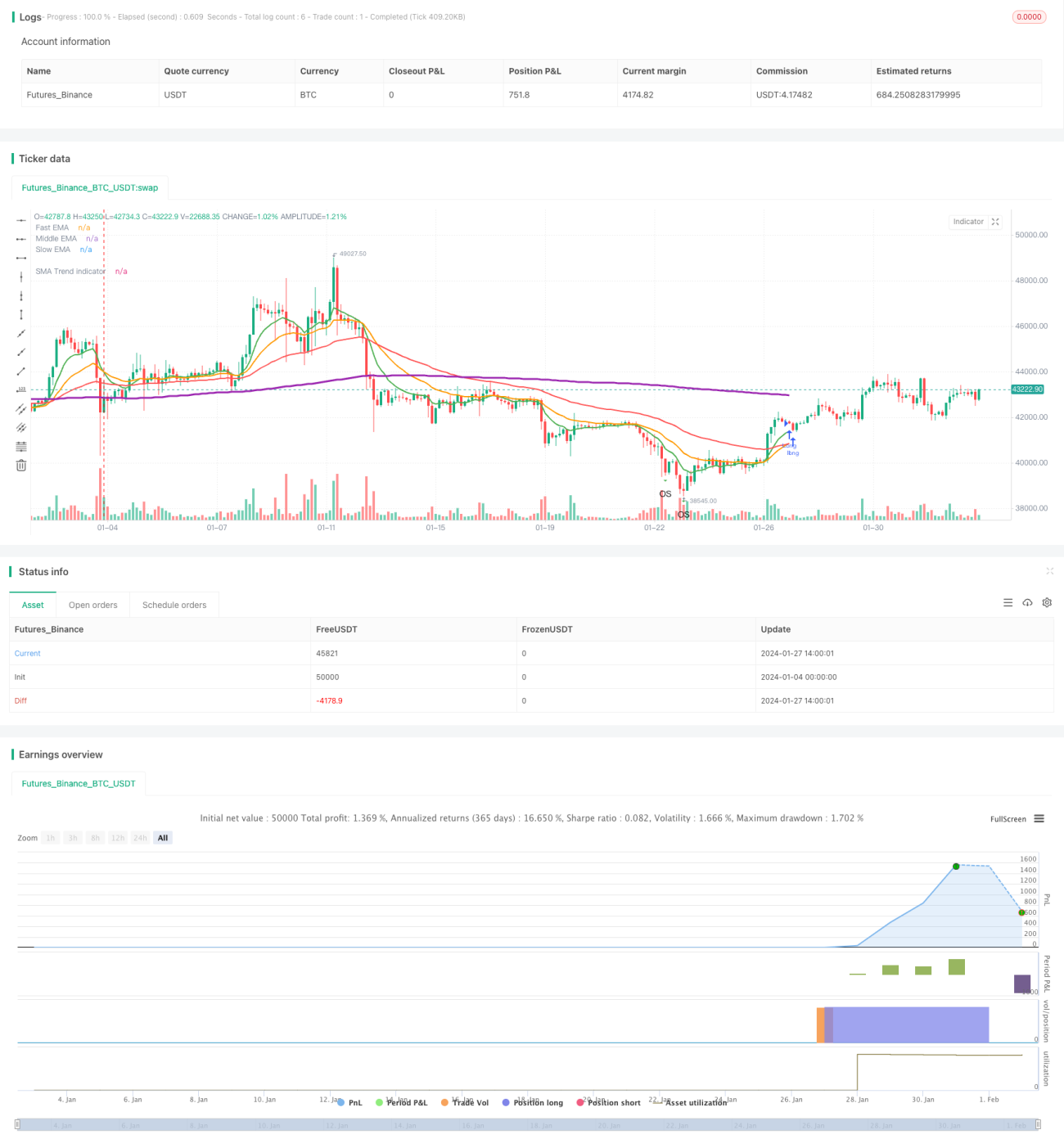

Chiến lược sử dụng ba đường trung bình động hàm mũ: đường nhanh, đường trung bình và đường chậm. Khi đường trung bình cắt lên trên đường chậm thì mua (long); khi đường nhanh cắt xuống dưới đường trung bình thì đóng vị thế. Đây là một chiến lược theo xu hướng điển hình, xác định hướng xu hướng thông qua sự chuyển đổi đa/không của ba đường trung bình.

Đồng thời, chiến lược sử dụng chỉ số ATR để tính toán các mức chốt lời và cắt lỗ. Cụ thể, mức chốt lời cho lệnh mua là giá vào lệnh + ATR * hệ số chốt lời; mức chốt lời cho lệnh bán là giá vào lệnh – ATR * hệ số chốt lỗ. Nguyên lý cắt lỗ tương tự như chốt lời. Điều này giúp hạn chế hiệu quả rủi ro một chiều.

Phân tích ưu điểm

- Chỉ số quyết định trực quan, rõ ràng, dễ hiểu và dễ thực hiện.

- Tính hệ thống cao, dễ dàng định lượng.

- Kết hợp cả theo dõi xu hướng và kiểm soát rủi ro.

Phân tích rủi ro

- Có độ trễ nhất định, không thể kịp thời bắt được các điểm đảo chiều.

- Dễ bị cắt lỗ trong xu hướng dao động (sideways).

- Cần tối ưu hóa thông số, nếu không hiệu quả thực hiện sẽ kém.

Các biện pháp ứng phó rủi ro bao gồm: rút ngắn chu kỳ đường trung bình phù hợp, tối ưu hóa hệ số chốt lời/cắt lỗ, thêm các chỉ số quyết định phụ trợ.

Hướng tối ưu hóa

- Kết hợp nhiều loại đường trung bình khác nhau để tìm tham số tốt nhất.

- Bổ sung các chỉ báo kỹ thuật khác để phán đoán, như MACD, RSI, v.v.

- Sử dụng thuật toán học máy để tự động tối ưu hóa tham số.

- Điều chỉnh linh hoạt mức chốt lời cắt lỗ dựa trên biên độ thực.

- Kết hợp chỉ báo tâm lý để tránh giao dịch quá tải.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược theo xu hướng hiệu quả ổn định, với thiết lập tham số đơn giản, dễ thực hiện. Thông qua việc chốt lời và cắt lỗ động dựa trên ATR, có thể hạn chế rủi ro một chiều. Tuy nhiên, cần chú ý đến việc tối ưu hóa tham số và kết hợp các chỉ báo, tránh tối ưu quá mức và độ trễ quyết định. Nhìn chung, cân bằng lợi nhuận – rủi ro khá tốt, đáng để cân nhắc.

- 1