Chiến lược giao dịch định lượng dựa trên kênh SSL và xu hướng sóng

Tổng quan

Chiến lược này chủ yếu dựa trên chỉ báo kênh SSL và chỉ báo xu hướng sóng, kết hợp với các chỉ báo phụ trợ khác, tạo nên một chiến lược giao dịch định lượng tương đối hoàn chỉnh. Tên chiến lược bao gồm các chỉ báo cốt lõi như kênh SSL và xu hướng sóng, cùng với các từ khóa về giao dịch định lượng, đáp ứng yêu cầu.

Nguyên lý chiến lược

Chiến lược này có sáu điều kiện vào lệnh giao dịch, trong đó hai điều kiện đầu là cốt lõi, cụ thể như sau:

- Đường cơ sở của chỉ báo kết hợp SSL có màu xanh lam (tăng giá) hoặc đỏ (giảm giá)

- Chỉ báo kênh SSL cắt lên trên (tăng giá) hoặc cắt xuống dưới (giảm giá)

- Chỉ báo xu hướng sóng cắt lên trên (tăng giá) hoặc cắt xuống dưới (giảm giá)

- Chiều cao nến vào lệnh không vượt quá ngưỡng

- Nến vào lệnh nằm bên trong dải Bollinger

- Mức chốt lời không chạm vào đường trung bình động

Khi cả sáu điều kiện này đồng thời thỏa mãn, chiến lược sẽ vào lệnh mua hoặc bán. Khoảng cách cắt lỗ được tính dựa trên giá trị của chỉ báo ATR, khoảng cách chốt lời bằng khoảng cách cắt lỗ nhân với tỷ lệ Risk Reward Ratio.

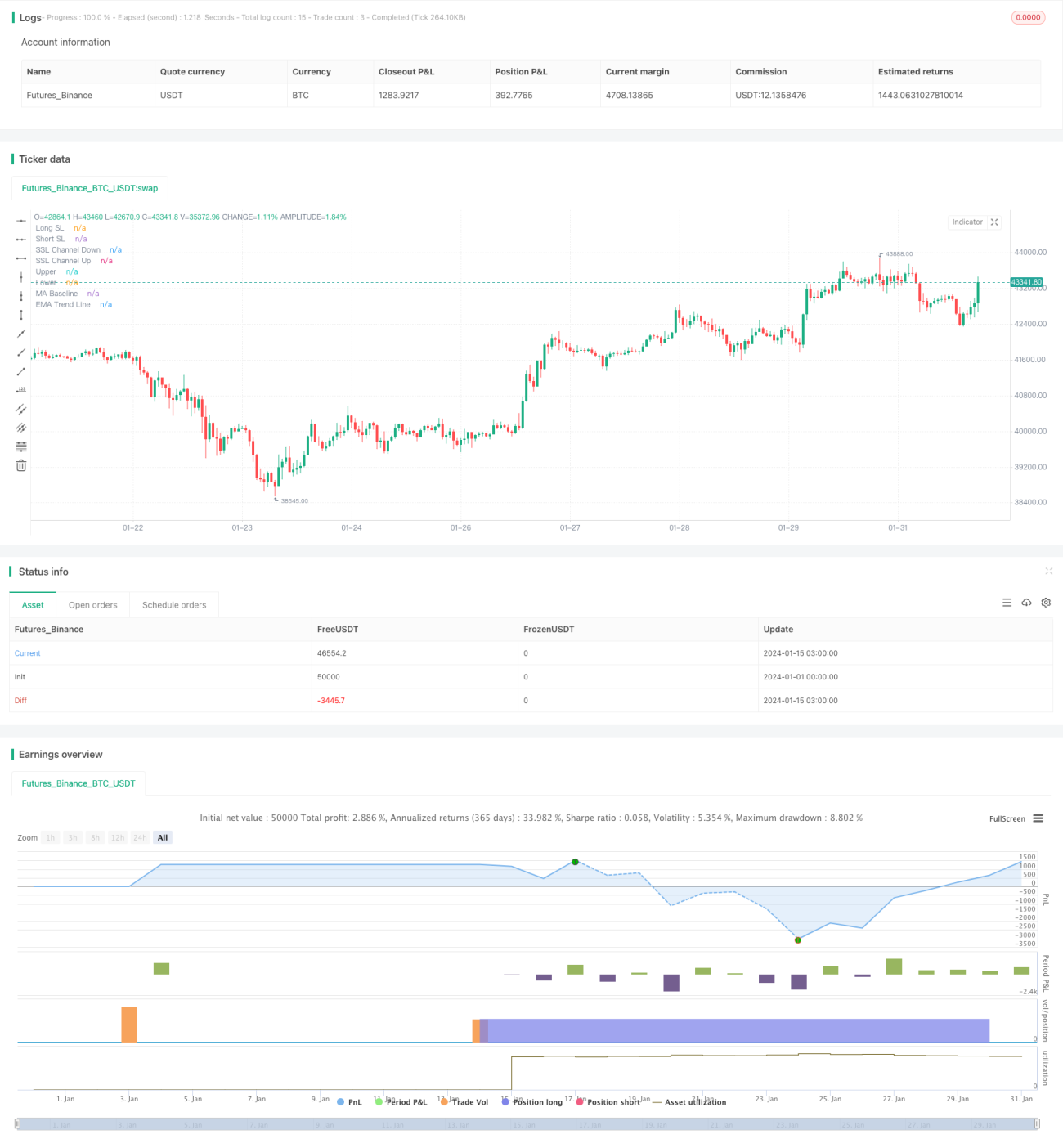

Chiến lược này cũng có cơ chế quản lý rủi ro hoàn chỉnh, bao gồm thiết lập cắt lỗ, kiểm soát quy mô vị thế và kiểm soát drawdown tối đa. Đồng thời, chiến lược vẽ các đường hỗ trợ trên biểu đồ, giúp trực quan nhìn thấy mức cắt lỗ và chốt lời mỗi lần, cũng như tình hình lãi/lỗ cụ thể. Điều này rất hữu ích cho việc phân tích và tối ưu hóa chiến lược.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là sử dụng chỉ báo kênh SSL để xác định hướng xu hướng với độ chính xác rất cao, kết hợp với các chỉ báo như xu hướng sóng để xác nhận, có thể giảm đáng kể các tín hiệu nhiễu. Đồng thời, các điều kiện vào lệnh nghiêm ngặt cũng giúp tránh các giao dịch không cần thiết, từ đó giảm số lần giao dịch và giảm chi phí giao dịch.

Ngoài ra, cơ chế quản lý rủi ro và vốn hoàn chỉnh của chiến lược cũng là một lợi thế lớn. Các chiến lược cắt lỗ và chốt lời được thiết lập trước có thể kiểm soát hiệu quả mức thua lỗ tối đa cho mỗi giao dịch. Kết hợp với kiểm soát quy mô vị thế, có thể kiểm soát drawdown tối đa của tài khoản trong phạm vi có thể chấp nhận được.

Phân tích rủi ro

Rủi ro lớn nhất của chiến lược này là các điều kiện vào lệnh nghiêm ngặt có thể bỏ lỡ một số cơ hội giao dịch, dẫn đến khả năng sinh lợi bị ảnh hưởng nhất định. Khi thị trường ở trạng thái dao động, khả năng sinh lợi của chiến lược cũng sẽ giảm.

Ngoài ra, hiệu quả của các chỉ báo như xu hướng sóng trong việc xác định xu hướng thị trường cũng có thể bị ảnh hưởng bởi các bất thường thị trường như phá vỡ giả. Lúc này cần điều chỉnh tham số hoặc thêm các chỉ báo khác để xác nhận.

Nhìn chung, rủi ro của chiến lược này vẫn có thể kiểm soát được. Thông qua điều chỉnh và tối ưu hóa tham số, có thể làm cho chiến lược thích nghi hơn với các môi trường thị trường khác nhau.

Hướng tối ưu hóa

Chiến lược này còn có một số hướng có thể tối ưu hóa như sau:

- Tối ưu hóa tham số của xu hướng sóng để xác định điểm đảo chiều xu hướng chính xác hơn

- Thêm các chỉ báo khác để xác nhận, như KDJ, MACD, v.v., tránh ảnh hưởng của phá vỡ giả

- Có thể điều chỉnh và tối ưu hóa tham số theo từng sản phẩm, từng khung thời gian, tăng tính ổn định của chiến lược

- Thêm thuật toán học máy, sử dụng dữ liệu lịch sử để huấn luyện, tối ưu hóa tham số chiến lược theo thời gian thực

- Sử dụng các thuật toán như yếu tố tần suất cao để tăng tần suất giao dịch và khả năng sinh lợi của chiến lược

Thông qua việc thực hiện các biện pháp tối ưu hóa này, dự kiến khả năng sinh lợi và tính ổn định của chiến lược có thể đạt đến mức cao hơn.

Tổng kết

Nhìn chung, chiến lược này tích hợp nhiều chỉ báo và cơ chế vào lệnh nghiêm ngặt, vừa đảm bảo tỷ lệ thắng cao, vừa đạt được hiệu quả kiểm soát rủi ro tốt. Kết hợp với các hướng tối ưu hóa trong tương lai, chiến lược này có tiềm năng phát triển lớn, là một chiến lược giao dịch định lượng đáng được đề xuất.

- 1