Chiến lược dựa trên theo dõi động lượng và xu hướng

Tổng quan

Chiến lược này kết hợp chỉ báo SuperTrend và chỉ báo Directional Movement Index (ADX) để xác định và theo dõi xu hướng. Chỉ báo SuperTrend dùng để nhận biết hướng xu hướng giá hiện tại, ADX dùng để đánh giá sức mạnh xu hướng – chỉ giao dịch khi xu hướng mạnh. Ngoài ra, chiến lược còn sử dụng màu sắc thân nến, chỉ báo khối lượng để xác nhận, hình thành bộ quy tắc giao dịch tương đối hoàn chỉnh.

Nhìn chung, chiến lược này thuộc dạng theo dõi xu hướng, nhằm nắm bắt các xu hướng rõ ràng trung và dài hạn, đồng thời tránh bị nhiễu trong giai đoạn tích lũy và dao động.

Nguyên lý chiến lược

-

Sử dụng chỉ báo SuperTrend để xác định hướng xu hướng giá. Khi giá đứng trên SuperTrend là tín hiệu tăng, khi giá đứng dưới SuperTrend là tín hiệu giảm.

-

Sử dụng ADX để đánh giá sức mạnh xu hướng. Chỉ phát sinh tín hiệu giao dịch khi ADX lớn hơn ngưỡng cài đặt, giúp lọc bỏ giai đoạn tích lũy không rõ ràng.

-

Màu sắc thân nến dùng để xác định diễn biến tăng hay giảm hiện tại, kết hợp với chỉ báo SuperTrend để tạo xác nhận.

-

Khối lượng giao dịch tăng lên được dùng làm tín hiệu xác nhận. Chỉ mở vị thế khi khối lượng tăng.

-

Thiết lập mức cắt lỗ và chốt lời để khóa lợi nhuận và kiểm soát rủi ro.

-

Đóng tất cả vị thế trước khi kết thúc khung giờ giao dịch đã được thiết lập.

Ưu điểm chiến lược

-

Theo dõi xu hướng rõ ràng trung và dài hạn, tránh dao động lằng nhằng, đạt tỷ lệ lợi nhuận cao.

-

Tham số chiến lược ít, dễ hiểu và dễ thực thi.

-

Quản lý rủi ro tốt với cắt lỗ và chốt lời được thiết lập.

-

Sử dụng nhiều chỉ báo để xác nhận, giảm thiểu tín hiệu giả.

Rủi ro chiến lược

-

Khi thị trường điều chỉnh sâu có thể gặp thua lỗ lớn.

-

Khi kết quả kinh doanh của cổ phiếu thay đổi có thể xảy ra đảo chiều mạnh.

-

Sự kiện thiên nga đen khi chính sách thay đổi lớn.

Biện pháp xử lý rủi ro tương ứng:

-

Điều chỉnh tham số ADX phù hợp, đảm bảo chỉ giao dịch trong xu hướng mạnh.

-

Mở rộng mức cắt lỗ, kiểm soát thua lỗ mỗi lệnh.

-

Theo dõi sát chính sách và sự kiện quan trọng, chủ động cắt lỗ khi cần.

Hướng tối ưu hóa chiến lược

-

Có thể thử nghiệm các tổ hợp tham số SuperTrend khác nhau, chọn tham số cho tín hiệu ổn định hơn.

-

Có thể thử nghiệm các tham số ADX khác nhau để xác định tổ hợp tối ưu.

-

Có thể thêm các chỉ báo xác nhận khác như độ biến động, Bollinger Bands... để giảm thêm tín hiệu giả.

-

Có thể kết hợp chiến lược phá vỡ (breakout) để cắt lỗ kịp thời khi xu hướng bị phá vỡ.

Tổng kết

Chiến lược này có ý tưởng tổng thể rõ ràng: dùng SuperTrend để xác định hướng xu hướng giá, dùng ADX để đánh giá sức mạnh xu hướng, theo dõi xu hướng trong điều kiện xu hướng mạnh. Đồng thời thiết lập cắt lỗ và chốt lời để kiểm soát rủi ro. Tham số ít, dễ tối ưu hóa. Có thể xem như một ví dụ tốt để học chiến lược xu hướng đơn giản hiệu quả. Sau đó có thể cải thiện thêm thông qua tối ưu hóa tham số, lọc tín hiệu, v.v.

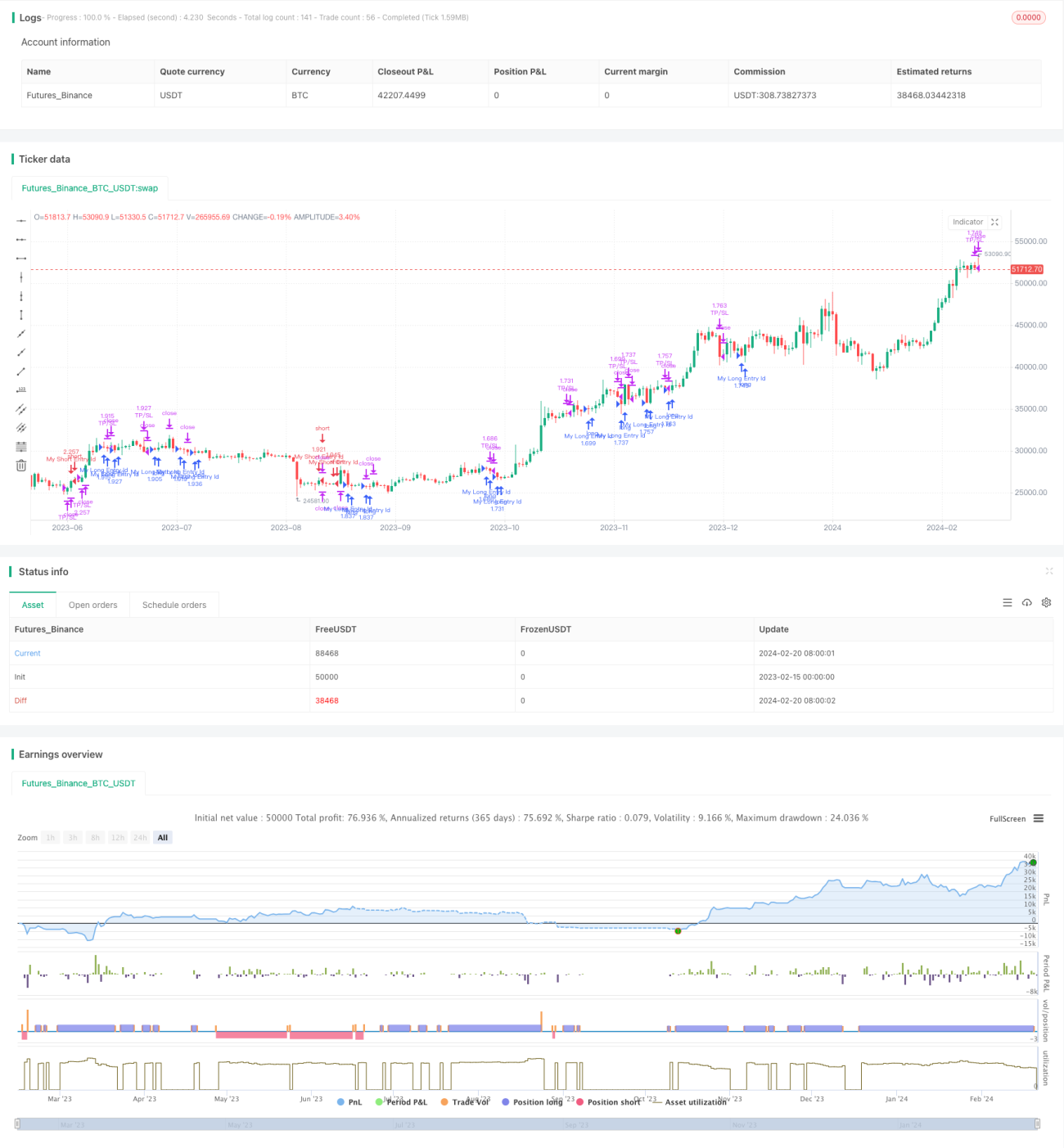

/*backtest

start: 2023-02-15 00:00:00

end: 2024-02-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Intraday Strategy Template

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © vikris- 1