Hệ thống giao dịch định lượng kép

Chiến lược này là một hệ thống giao dịch tổng hợp kết hợp chỉ báo CCI, chỉ báo RSI và hai đường trung bình động. Hệ thống này có thể nắm bắt xu hướng thông thường, đồng thời sử dụng sự giao nhau của các chỉ báo RSI để xác nhận thêm điểm vào lệnh, giúp lọc bỏ một số nhiễu.

Nguyên lý chiến lược

Chiến lược này chủ yếu dựa vào chỉ báo CCI để xác định hướng xu hướng. Khi giá trị chỉ báo CCI trên 100 là thị trường tăng, dưới -100 là thị trường giảm. Hệ thống sử dụng sự giao nhau của hai đường trung bình động để hỗ trợ xác định hướng xu hướng. Khi đường trung bình động nhanh cắt lên trên đường trung bình động chậm là tín hiệu mua, ngược lại là tín hiệu bán.

Sau khi xác định xu hướng tăng/giảm, hệ thống sử dụng sự giao nhau của hai chỉ báo RSI với độ dài tham số khác nhau làm xác nhận điểm vào. Ví dụ, trong thị trường tăng, nếu chỉ báo RSI chu kỳ ngắn cắt lên trên chỉ báo RSI chu kỳ dài, đó là tín hiệu mua cuối cùng. Thiết kế này chủ yếu để lọc nhiễu, tránh các điều chỉnh ngắn hạn trong xu hướng gây ra giao dịch sai.

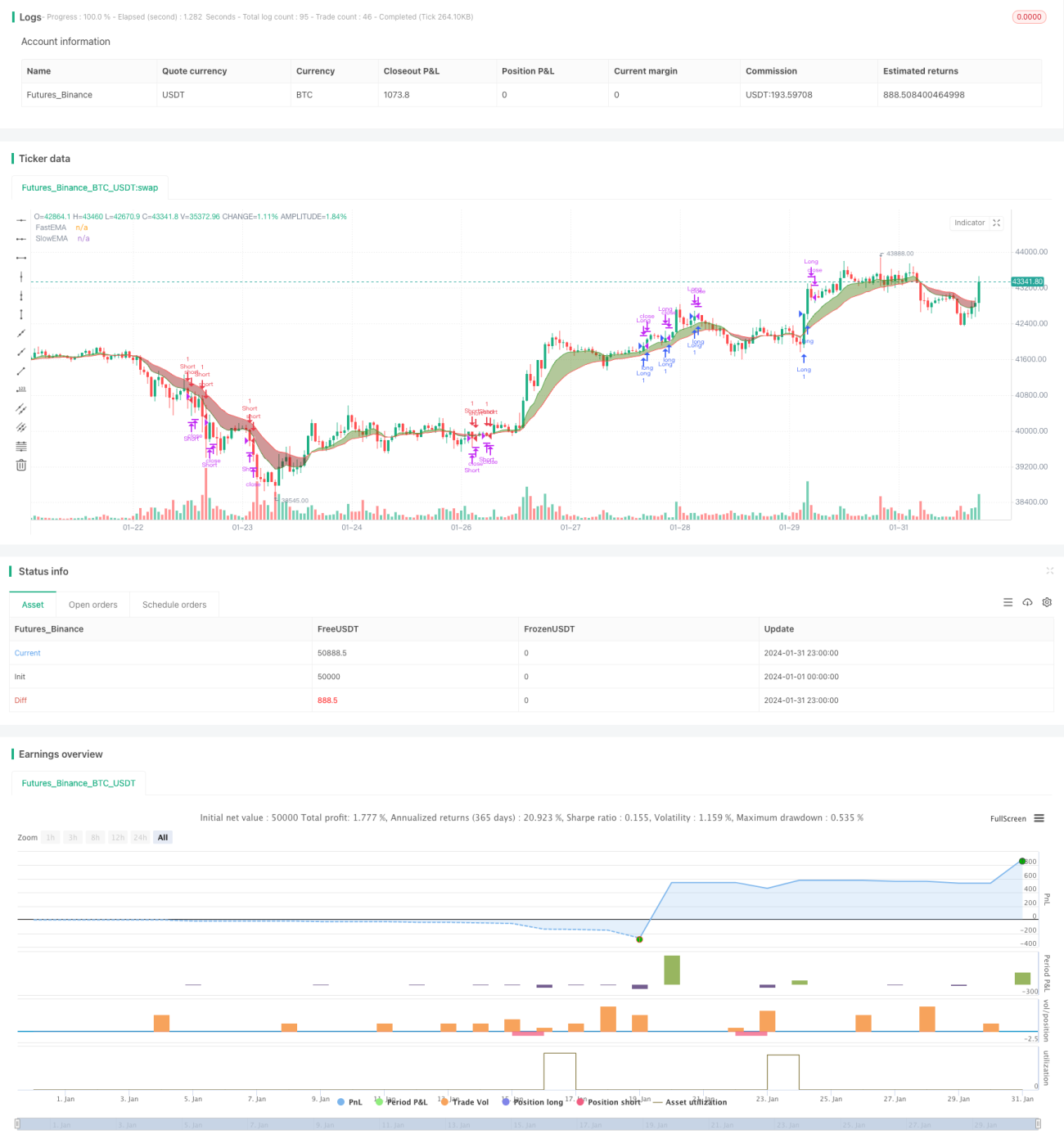

Chiến lược này chỉ mở lệnh trong khung thời gian giao dịch chỉ định và đóng toàn bộ lệnh 15 phút trước khi đóng cửa để tránh rủi ro qua đêm. Sau khi mở lệnh, sẽ sử dụng trailing stop để chốt lời.

Phân tích ưu điểm

- Kết hợp xác định xu hướng và sự giao nhau của chỉ báo, có thể nhận diện xu hướng hiệu quả và lọc nhiễu, điểm vào chính xác

- Sử dụng trailing stop để chủ động kiểm soát rủi ro, tránh tình trạng bị săn đuổi stop loss

- Chỉ mở lệnh trong khung thời gian giao dịch chỉ định, tránh rủi ro gap qua đêm

- Tham số RSI có thể điều chỉnh, linh hoạt thích ứng với các môi trường thị trường khác nhau

Phân tích rủi ro

- Chỉ báo CCI hoạt động kém trong thị trường có biến động bất thường

- Điều kiện giao nhau của hai RSI bị hạn chế nhiều, có thể bỏ lỡ một số cơ hội

- Trailing stop có thể quá chủ quan, cần tối ưu tham số

- Khung thời gian giao dịch chỉ định có thể bỏ lỡ các gap do tin tức đêm quan trọng

Đề xuất tối ưu

- Có thể thử nghiệm các tham số CCI khác nhau để tìm ra tổ hợp tham số tốt nhất

- Thử nghiệm xem có thể bỏ điều kiện giới hạn giao nhau RSI, chỉ dùng CCI để xác định điểm vào

- Thực hiện backtest tối ưu hóa tham số trailing stop để tìm tham số tốt nhất

- Thử nghiệm bỏ logic đóng lệnh bắt buộc, thay vào đó theo dõi trailing stop trong suốt thời gian nắm giữ để tối đa hóa lợi nhuận

Tổng kết

Chiến lược này xem xét tổng thể cả xác định xu hướng và xác nhận giao nhau của chỉ báo, vừa kiểm soát rủi ro vừa đảm bảo hiệu quả của tín hiệu giao dịch. Thông qua tối ưu hóa tham số và điều chỉnh logic, chiến lược này có thể nâng cao thêm không gian lợi nhuận và giảm thiểu cơ hội bị bỏ lỡ. Đây là một ý tưởng giao dịch rất tiềm năng.

- 1