Chiến lược giao dịch đa khung thời gian dựa trên chỉ báo nén

Tổng quan

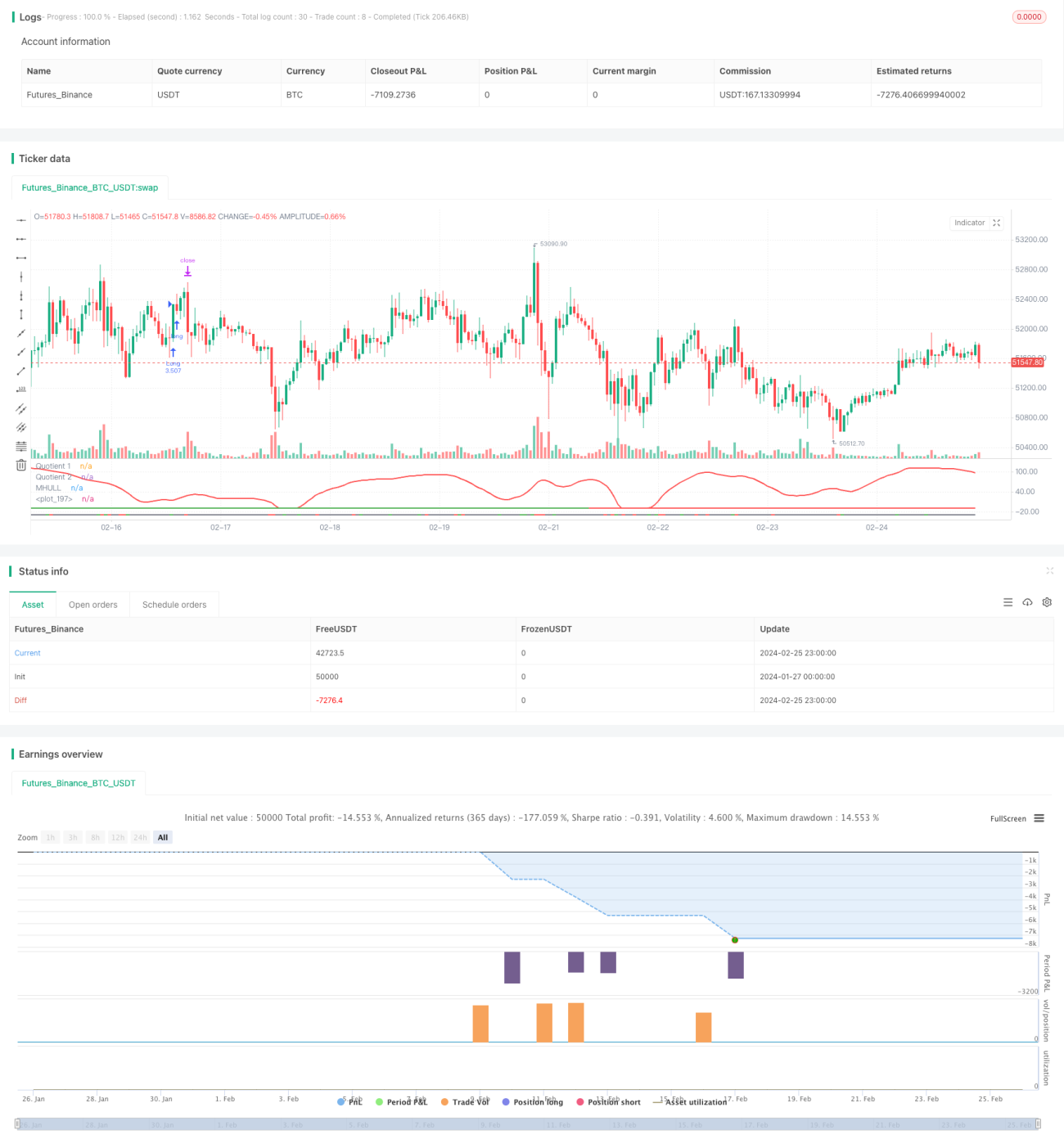

Chiến lược này kết hợp ba chỉ báo: Boom Hunter, Hull Suite và Volatility Oscillator để thực hiện giao dịch theo xu hướng và breakout trên nhiều khung thời gian. Chiến lược phù hợp với các tài sản kỹ thuật số có biến động cao và biến động giá đột ngột như Bitcoin.

Nguyên lý

Logic cốt lõi của chiến lược dựa trên ba chỉ báo sau:

-

Boom Hunter: Một bộ dao động sử dụng kỹ thuật nén chỉ báo, xác định tín hiệu mua và bán thông qua sự giao nhau của hai chỉ báo (Quotient1 và Quotient2).

-

Hull Suite: Một nhóm các chỉ báo đường trung bình động trơn tru, xác định hướng xu hướng dựa trên mối quan hệ giữa dải giữa, dải trên và dải dưới.

-

Volatility Oscillator: Một chỉ báo dao động định lượng thông tin biến động giá.

Logic vào lệnh của chiến lược như sau: Khi hai chỉ báo Quotient của Boom Hunter giao nhau lên hoặc xuống, đồng thời giá phá vỡ dải giữa Hull và phân kỳ với dải trên hoặc dải dưới, và chỉ báo biến động nằm trong vùng quá mua/quá bán. Điều này giúp lọc các tín hiệu phá vỡ giả, tăng độ chính xác khi vào lệnh.

Cắt lỗ được thiết lập bằng cách tìm đáy thấp nhất hoặc đỉnh cao nhất trong một khoảng thời gian nhất định (mặc định 20 nến), còn chốt lời được tính bằng tỷ lệ phần trăm cắt lỗ nhân với tỷ lệ chốt lời đã cấu hình (mặc định 3 lần). Khối lượng vị thế được tính dựa trên tỷ lệ phần trăm tổng tài sản tài khoản (mặc định 3%) và mức cắt lỗ cụ thể của từng mã.

Ưu điểm

- Sử dụng kỹ thuật nén chỉ báo để trích xuất tín hiệu giao dịch chính từ giá, tăng xác suất sinh lời.

- Kết hợp nhiều chỉ báo để xác nhận, tránh phá vỡ giả, xác định chính xác hướng xu hướng.

- Thiết lập cắt lỗ và chốt lời động, cho phép bám xu hướng với rủi ro được kiểm soát.

- Sử dụng chỉ báo biến động để đảm bảo giao dịch trong môi trường biến động cao.

- Phân tích đa khung thời gian, tăng tính ổn định của chiến lược.

Rủi ro

- Chỉ báo Boom Hunter có thể bị méo do nén, dẫn đến tín hiệu sai.

- Dải giữa Hull Suite có độ trễ, không thể theo dõi kịp thời sự thay đổi giá.

- Khi biến động giảm, có thể bỏ lỡ cơ hội giao dịch hoặc gây ra đóng lệnh thua lỗ.

Cách khắc phục:

- Điều chỉnh tham số của chỉ báo nén để cân bằng độ nhạy của chỉ báo.

- Thử sử dụng các đường trung bình động hàm mũ như EHMA để thay thế cho dải giữa.

- Thêm các chỉ báo đánh giá khác để tránh bị đánh lừa bởi biến động.

Tối ưu hóa

Chiến lược có thể được tối ưu hóa từ các khía cạnh sau:

-

Tối ưu hóa tham số: Thay đổi các tham số chỉ báo như độ dài chu kỳ, hệ số nén để tìm ra bộ tham số tốt nhất.

-

Tối ưu hóa khung thời gian: Kiểm tra các khung thời gian khác nhau (1 phút, 5 phút, 30 phút, v.v.) để tìm ra chu kỳ giao dịch phù hợp nhất.

-

Tối ưu hóa khối lượng: Thay đổi kích thước và tỷ lệ khối lượng mỗi giao dịch để tìm ra phương án sử dụng vốn tối ưu.

-

Tối ưu hóa cắt lỗ: Điều chỉnh vị trí cắt lỗ theo từng cặp giao dịch để đạt tỷ lệ lợi nhuận/rủi ro tốt nhất.

-

Tối ưu hóa điều kiện: Thêm hoặc bớt các điều kiện lọc chỉ báo để có thời điểm vào lệnh chính xác hơn.

Kết luận

Chiến lược này kết hợp ba chỉ báo Boom Hunter, Hull Suite và Volatility Oscillator, thực hiện giao dịch theo xu hướng trên nhiều khung thời gian, có thể nhận diện hiệu quả các hành vi giá đột ngột, phù hợp với các tài sản kỹ thuật số có biến động cao. Chiến lược có rủi ro được kiểm soát, thông qua tối ưu hóa tham số, điều kiện lọc và cắt lỗ, có tính thực chiến và khả năng mở rộng cao.

- 1