Chiến lược long kết hợp chỉ báo động lượng và đường trung bình động

Tổng quan

Chiến lược này kết hợp chỉ báo động lượng MACD và chỉ báo xu hướng DMI, thực hiện lệnh mua khi điều kiện phù hợp. Thoát lệnh được thiết lập với chốt lời cố định và trailing stop dựa trên biến động tùy chỉnh để khóa lợi nhuận.

Nguyên lý

Chiến lược này dựa vào các chỉ báo MACD và DMI để vào lệnh:

- Khi MACD dương (đường MACD nằm trên đường Signal) cho thấy động lực tăng giá đang mạnh lên.

- Khi DI+ trong DMI cao hơn DI- cho thấy thị trường đang trong giai đoạn xu hướng tăng.

Khi cả hai điều kiện trên cùng thỏa mãn, lệnh mua sẽ được mở.

Thoát lệnh có hai tiêu chuẩn:

- Chốt lời cố định: chốt lời khi giá đóng cửa tăng đến tỷ lệ phần trăm đã đặt.

- Trailing stop dựa trên biến động: sử dụng ATR và mức giá cao nhất gần đây để tính toán một vị trí cắt lỗ điều chỉnh động. Điều này có thể trailing stop loss theo biến động của thị trường.

Lợi thế

- Sự kết hợp giữa MACD và DMI cho phép đánh giá hướng xu hướng thị trường một cách đáng tin cậy, giảm thiểu các giao dịch sai.

- Điều kiện chốt lời kết hợp giữa chốt lời cố định và trailing stop dựa trên biến động, giúp linh hoạt khóa lợi nhuận.

Rủi ro

- Cả MACD và DMI đều có thể tạo ra tín hiệu giả, dẫn đến thua lỗ không cần thiết.

- Chốt lời cố định có thể khiến lợi nhuận không được tối đa hóa.

- Tốc độ trailing của trailing stop dựa trên biến động có thể được điều chỉnh không phù hợp, quá mạnh hoặc quá bảo thủ.

Hướng tối ưu

- Có thể xem xét thêm các chỉ báo khác để lọc tín hiệu vào lệnh, ví dụ như sử dụng chỉ báo KDJ để xác định tình trạng quá mua/quá bán.

- Có thể thử nghiệm các tham số khác nhau để đạt hiệu quả chốt lời/cắt lỗ tốt hơn.

- Có thể điều chỉnh các tham số như đường trung bình động theo từng sản phẩm giao dịch cụ thể để tối ưu hóa hệ thống.

Tổng kết

Chiến lược này tổng hợp nhiều chỉ báo để đánh giá xu hướng và điều kiện thị trường, can thiệp vào những thời điểm có xác suất thuận lợi cao. Điều kiện chốt lời cũng được thiết kế tối ưu, đảm bảo một mức lợi nhuận nhất định đồng thời tính đến sự linh hoạt trong việc khóa lợi nhuận. Thông qua việc điều chỉnh tham số và quản lý rủi ro thêm, chiến lược này có thể trở thành một hệ thống giao dịch định lượng ổn định.

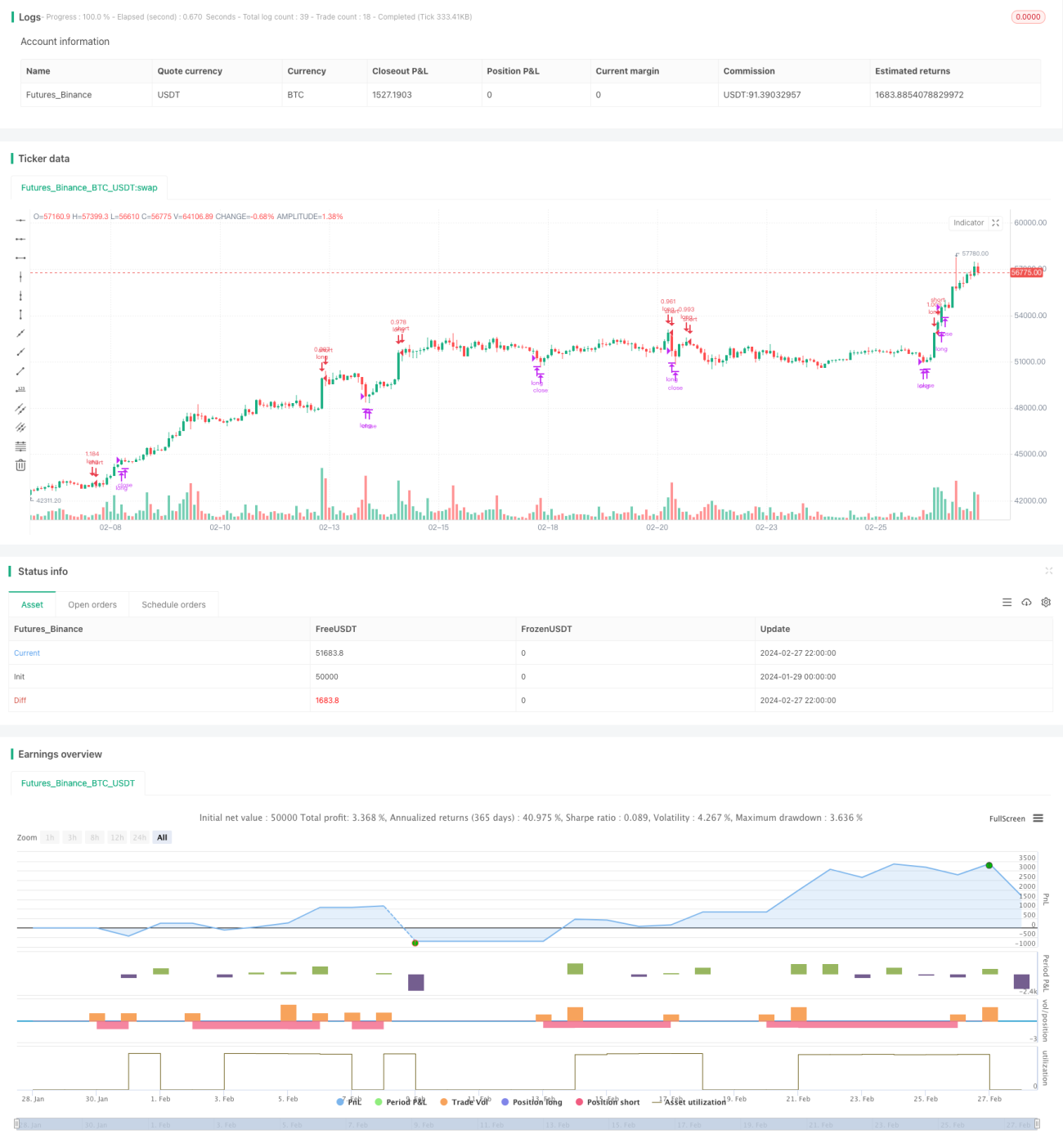

/*backtest

start: 2024-01-29 00:00:00

end: 2024-02-28 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=4

strategy(shorttitle='(MACD + DMI Scalping with Volatility Stop',title='MACD + DMI Scalping with Volatility Stop by (Coinrule)', overlay=true, initial_capital = 100, process_orders_on_close=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type=strategy.commission.percent, commission_value=0.1)

- 1