Chiến lược Theo xu hướng với Xác nhận Ba lần

Tổng quan

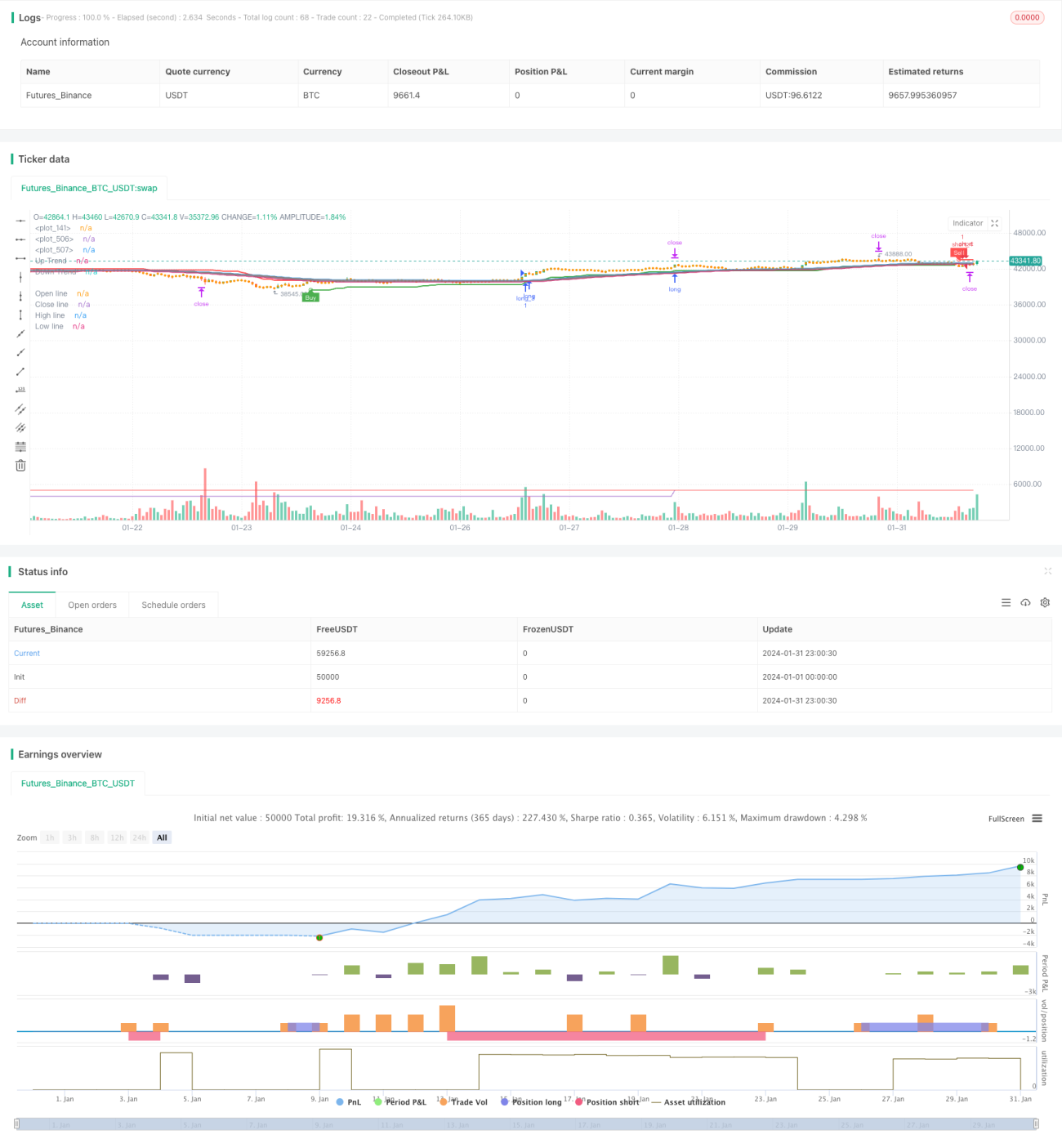

Chiến lược theo dõi xu hướng xác nhận ba lớp kết hợp tín hiệu từ ba chỉ báo chính: đường trung bình động, đường Ý Nghĩa (Yiyi Line) và Siêu Xu Hướng (Super Trend) để bắt được xu hướng với xác suất cao. Khi cả ba chỉ báo đồng thời phát tín hiệu mua hoặc bán, chiến lược sẽ vào lệnh kịp thời và theo dõi xu hướng; khi xu hướng đảo chiều, chiến lược sẽ nhanh chóng cắt lỗ và đảo chiều bán khống.

Nguyên lý chiến lược

Đường trung bình động xác định xu hướng chính

Chiến lược sử dụng đường trung bình động chu kỳ 52 để xác định hướng xu hướng chính. Khi giá vượt lên trên đường trung bình động, đó là xu hướng tăng; khi giá cắt xuống dưới đường trung bình động, đó là xu hướng giảm.

Đường Ý Nghĩa nhận diện đảo chiều phụ

Chiến lược đồng thời sử dụng đường Ý Nghĩa (Yiyi Line) để nhận diện các đảo chiều phụ ngắn hạn. Cách tính của đường Ý Nghĩa tương tự đường trung bình động, nhưng giá Đóng cửa được thay thế bằng giá Mở cửa, giúp phản ánh nhanh hơn thông tin đảo chiều giá. Khi giá vượt lên trên đường Ý Nghĩa đang giảm, báo hiệu tín hiệu giá ổn định và phục hồi ngắn hạn; khi giá cắt xuống dưới đường Ý Nghĩa đang tăng, báo hiệu tín hiệu giá giảm ngắn hạn.

Siêu Xu Hướng xác định điểm đảo chiều

Chiến lược cũng kết hợp chỉ báo Siêu Xu Hướng (Super Trend) để xác định các điểm đảo chiều quan trọng. Chỉ báo Siêu Xu Hướng kết hợp khoảng thời gian của chỉ báo ATR và dữ liệu giá, điều chỉnh động biên trên và biên dưới của kênh, từ đó xác định thời điểm đảo chiều.

Lọc tín hiệu xác nhận ba lớp

Khi cả ba chỉ báo (đường trung bình động, đường Ý Nghĩa, Siêu Xu Hướng) đồng thời phát tín hiệu mua, chiến lược mới vào lệnh mua; khi cả ba cùng phát tín hiệu bán, chiến lược mới vào lệnh bán. Nhờ xác nhận ba chỉ báo, có thể lọc hiệu quả các tín hiệu giả, nâng cao xác suất vào lệnh.

Phân tích ưu điểm

Đánh giá đa chiều, xác suất cao

Chiến lược kết hợp ba chỉ báo: đường trung bình động, đường Ý Nghĩa và Siêu Xu Hướng, đánh giá xu hướng và các điểm chính từ các chiều khác nhau, đảm bảo xác suất vào lệnh cao.

Phản ứng nhanh, theo dõi thời gian thực

Việc đưa vào đường Ý Nghĩa đảm bảo chiến lược có thể phản ứng nhanh với các đảo chiều ngắn hạn của giá; chỉ báo Siêu Xu Hướng với kênh thích ứng ATR cũng có thể theo dõi sự thay đổi giá theo thời gian thực.

Tự động chốt lời cắt lỗ, kiểm soát rủi ro hiệu quả

Chiến lược tích hợp sẵn cơ chế tự động chốt lời cắt lỗ, có thể điều chỉnh động điểm chốt lời cắt lỗ dựa trên ATR, kiểm soát hiệu quả thua lỗ trên mỗi lệnh.

Rủi ro và giải pháp

Rủi ro tần suất giao dịch quá cao

Do tín hiệu giao dịch của chiến lược xuất hiện thường xuyên, dễ gây giao dịch quá mức. Có thể tăng chu kỳ tham số đường trung bình động một cách phù hợp để giảm tần suất giao dịch.

Rủi ro không chắc chắn của đảo chiều

Hiệu quả của đường Ý Nghĩa và chỉ báo Siêu Xu Hướng trong việc xác định điểm đảo chiều không chắc chắn, có thể xảy ra rủi ro nhận định sai. Có thể tăng thêm điều kiện lọc tham số chỉ báo để đảm bảo tín hiệu đảo chiều có xác suất cao hơn.

Rủi ro thua lỗ trong thị trường dao động

Trong thị trường dao động (sideway), do các tín hiệu giao nhau liên tục, chiến lược sẽ thường xuyên mở lệnh rồi cắt lỗ, gây rủi ro thua lỗ. Có thể nhận diện thị trường dao động và tạm dừng giao dịch chiến lược trong giai đoạn này.

Hướng tối ưu hóa

Kết hợp chỉ báo biến động

Có thể xem xét kết hợp các chỉ báo biến động như Dải Bollinger. Khi giá tiến gần đến biên trên hoặc biên dưới của Dải Bollinger, tránh mở lệnh mới, có thể né tránh hiệu quả rủi ro trong thị trường dao động.

Tăng điều kiện lọc vào lệnh

Có thể thử thêm các chỉ báo hỗ trợ khác như KDJ, MACD, và chỉ vào lệnh khi chúng cũng đồng thời phát tín hiệu. Điều này có thể lọc thêm tín hiệu giả, giảm giao dịch không cần thiết.

Tối ưu hóa chiến lược chốt lời cắt lỗ

Có thể tối ưu hóa chiến lược chốt lời cắt lỗ, ví dụ như chốt lời di động, chốt lời di động hàm mũ, chốt lời theo từng phần với khoảng cách, để lợi nhuận nhiều hơn và ổn định hơn.

Tổng kết

Chiến lược theo dõi xu hướng xác nhận ba lớp tận dụng tối đa ưu điểm của ba chỉ báo: đường trung bình động, đường Ý Nghĩa và Siêu Xu Hướng, giúp đánh giá và bắt xu hướng với xác suất cao. Đồng thời, thiết lập cơ chế tự động chốt lời cắt lỗ để kiểm soát hiệu quả thua lỗ trên mỗi lệnh. Điều đáng để tối ưu hóa thêm là có thể kết hợp các chỉ báo phụ trợ khác để lọc vào lệnh, cũng như cải thiện chiến lược chốt lời cắt lỗ, giúp chiến lược trở nên thực tế hơn.

- 1