Chiến lược chốt lời cắt lỗ động cho vị thế mua/bán dựa trên VWAP và tín hiệu liên khung thời gian

Tổng quan

Chiến lược này sử dụng VWAP (Giá trung bình gia quyền theo khối lượng) trên khung ngày làm tín hiệu vào và ra lệnh. Khi giá đóng cửa cắt lên trên VWAP sẽ kích hoạt lệnh mua, stop loss đặt ở mức thấp nhất của nến trước đó nằm dưới VWAP, mục tiêu lợi nhuận đặt ở trên giá mở cửa 3 pip; khi giá đóng cửa cắt xuống dưới VWAP sẽ kích hoạt lệnh bán, stop loss đặt ở mức cao nhất của nến trước đó nằm trên VWAP, mục tiêu lợi nhuận đặt ở dưới giá mở cửa 3 pip. Chiến lược này không bao gồm điều kiện thoát lệnh, giao dịch sẽ được giữ cho đến khi xuất hiện tín hiệu ngược lại.

Nguyên lý chiến lược

- Lấy dữ liệu VWAP trên khung ngày, làm cơ sở để xác định xu hướng và tín hiệu giao dịch.

- Xác định xem giá đóng cửa hiện tại có cắt lên/xuống VWAP không, lần lượt là điều kiện kích hoạt cho lệnh mua và bán.

- Khi mua, nếu mức thấp nhất của nến trước đó nằm dưới VWAP, thì đặt stop loss ở mức đó, nếu không thì trực tiếp dùng VWAP làm stop loss; khi bán thì ngược lại.

- Sau khi mở lệnh, đặt mục tiêu chốt lời cố định 3 pip.

- Chiến lược chạy liên tục cho đến khi kích hoạt tín hiệu ngược lại để đóng lệnh và mở lệnh mới.

Bằng cách sử dụng dữ liệu VWAP xuyên khung để xác định xu hướng, đồng thời sử dụng stop loss động và chốt lời cố định, có thể nắm bắt hiệu quả xu hướng thị trường, kiểm soát rủi ro sụt giảm và kịp thời khóa lợi nhuận.

Phân tích ưu điểm

- Đơn giản hiệu quả: Logic chiến lược rõ ràng, chỉ sử dụng một chỉ báo VWAP, đã có thể thực hiện xác định xu hướng và kích hoạt tín hiệu, đơn giản dễ thực hiện và tối ưu.

- Stop loss động: Đặt stop loss dựa trên mức cao/thấp của nến trước đó, có thể thích ứng tốt hơn với biến động thị trường, giảm rủi ro.

- Chốt lời cố định: Đặt mục tiêu giá với số pip cố định giúp kịp thời khóa lợi nhuận, tránh lợi nhuận bị hao hụt.

- Dừng lỗ và chốt lời kịp thời: Chiến lược sẽ đóng lệnh ngay khi có tín hiệu ngược lại, không gây thêm tổn thất cho lợi nhuận hiện có, đồng thời sẽ mở lệnh mới để bắt kịp xu hướng mới.

Phân tích rủi ro

- Tối ưu tham số: Chiến lược sử dụng mốc 3 pip cố định để chốt lời, trong giao dịch thực tế có thể cần tối ưu dựa trên các tài sản và đặc điểm thị trường khác nhau để chọn tham số tốt nhất.

- Thị trường dao động: Trong thị trường dao động, việc vào và ra lệnh thường xuyên có thể dẫn đến chi phí giao dịch cao, ảnh hưởng đến lợi nhuận.

- Tính liên tục của xu hướng: Chiến lược phụ thuộc vào thị trường có xu hướng, nếu thị trường nằm trong vùng dao động hoặc xu hướng không liên tục, có thể xuất hiện nhiều tín hiệu giao dịch, mang lại nhiều rủi ro hơn.

Hướng tối ưu

- Lọc xu hướng: Thêm các chỉ báo xu hướng khác như đường trung bình động, MACD, để xác nhận xu hướng lần hai, tăng độ tin cậy của tín hiệu.

- Chốt lời động: Dựa vào độ biến động thị trường, chỉ báo ATR,... điều chỉnh linh hoạt số pip chốt lời để thích ứng tốt hơn với thị trường.

- Quản lý vị thế: Dựa vào vốn tài khoản, khẩu vị rủi ro,... điều chỉnh linh hoạt quy mô vị thế cho mỗi giao dịch.

- Lựa chọn khung giờ giao dịch: Dựa trên đặc điểm tài sản và mức độ hoạt động giao dịch, chọn khung giờ giao dịch tốt nhất để tăng hiệu quả chiến lược.

Tổng kết

Chiến lược này sử dụng dữ liệu VWAP xuyên khung để xác định xu hướng và kích hoạt tín hiệu, đồng thời sử dụng stop loss động và chốt lời cố định để kiểm soát rủi ro và khóa lợi nhuận. Đây là một chiến lược giao dịch định lượng đơn giản và hiệu quả. Thông qua các tối ưu về lọc xu hướng, chốt lời động, quản lý vị thế và lựa chọn khung giờ giao dịch, có thể nâng cao hơn nữa tính ổn định và tiềm năng lợi nhuận của chiến lược. Tuy nhiên, trong ứng dụng thực tế, vẫn cần chú ý đến các yếu tố như đặc điểm thị trường, chi phí giao dịch và tối ưu tham số để đạt được hiệu suất chiến lược tốt hơn.

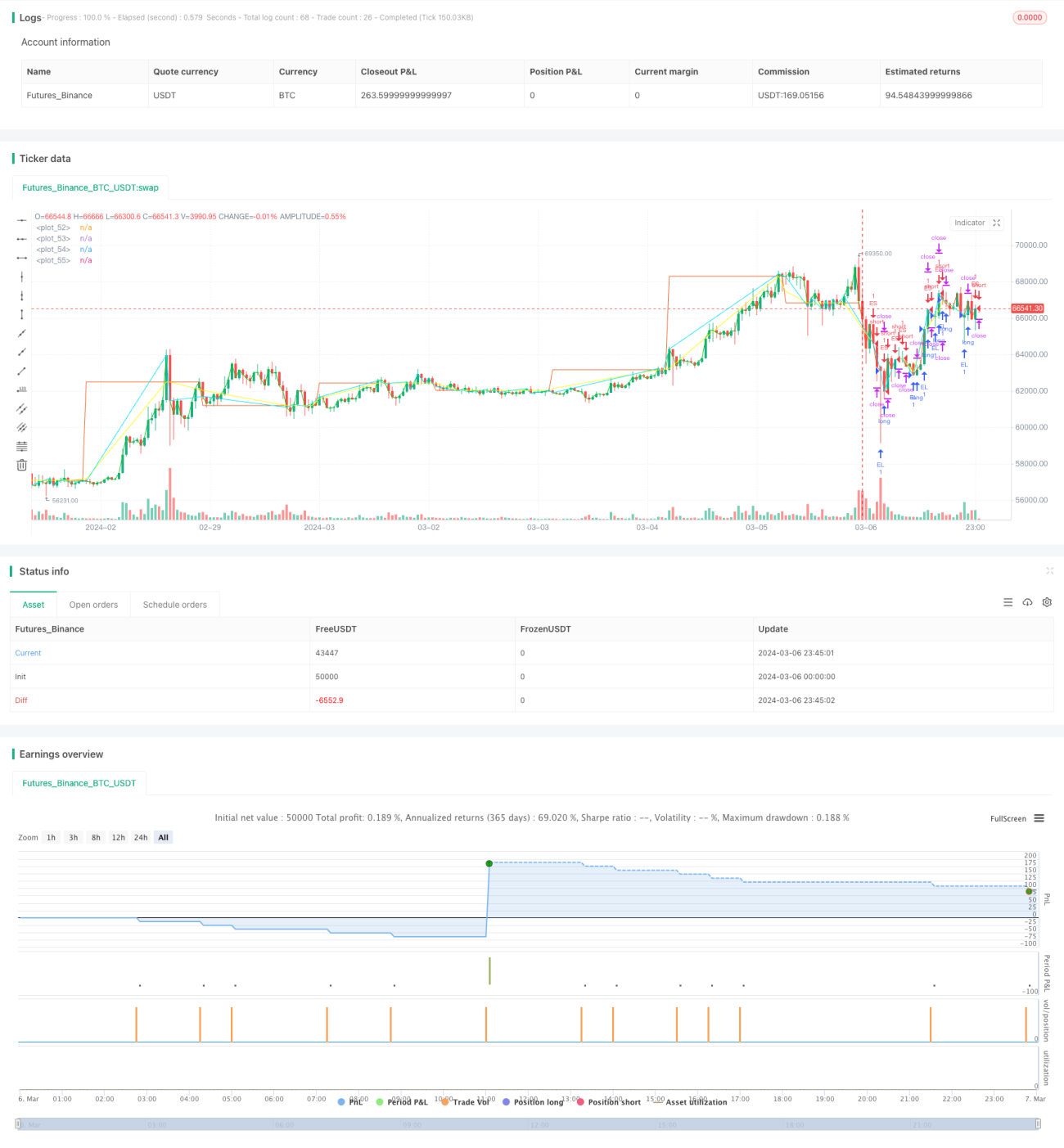

/*backtest

start: 2024-03-06 00:00:00

end: 2024-03-07 00:00:00

period: 45m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('Pine Script Tutorial Example Strategy 1', overlay=true, initial_capital=1000, default_qty_value=100, default_qty_type=strategy.percent_of_equity)

// fastEMA = ta.ema(close, 24)

// slowEMA = ta.ema(close, 200)- 1