Chiến lược giao dịch xu hướng động lượng Ruda

Tổng quan

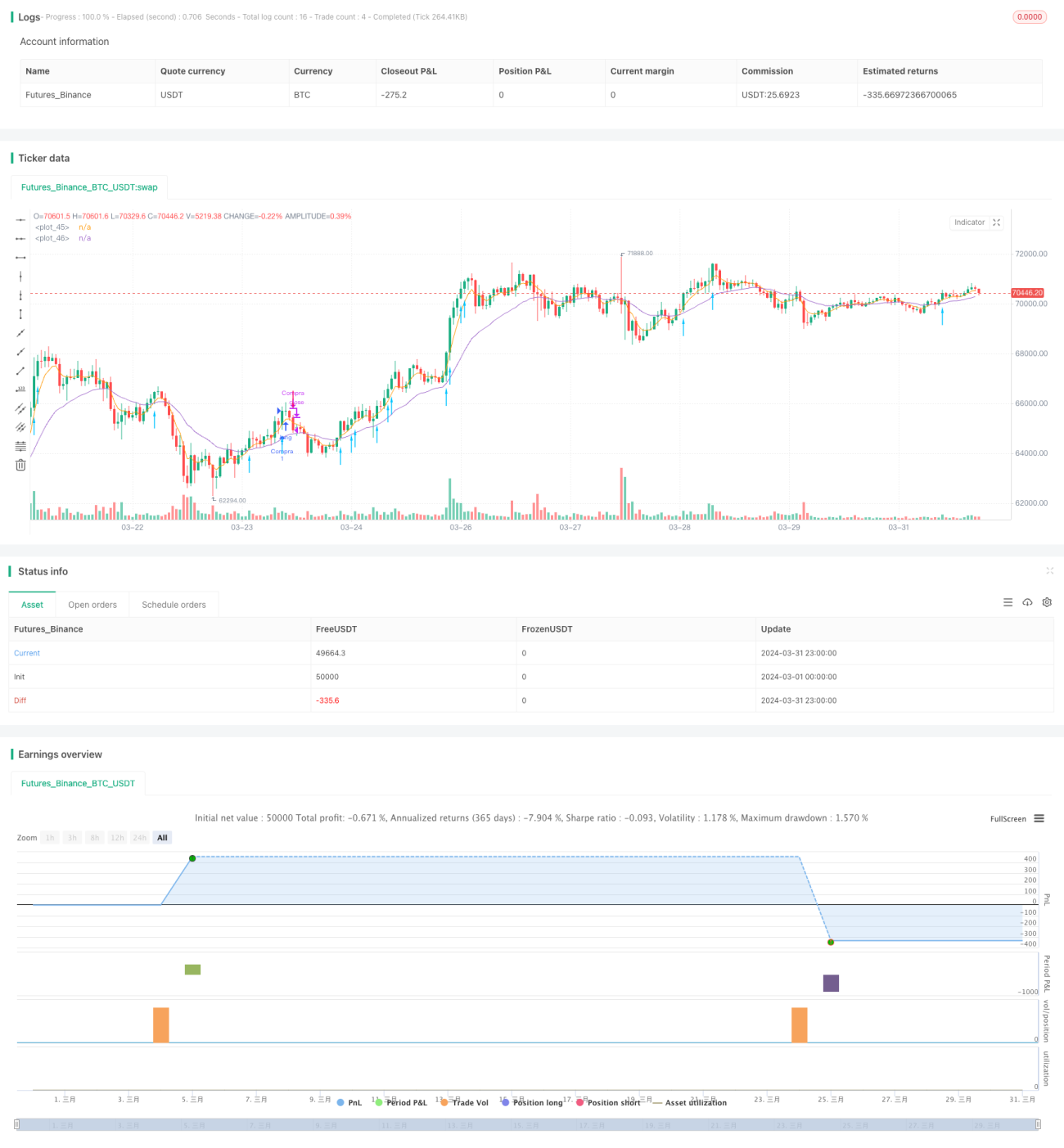

Chiến lược giao dịch động lượng theo xu hướng Ruda là một chiến lược giao dịch định lượng dựa trên các chỉ báo động lượng và xu hướng. Chiến lược này sử dụng các chỉ báo như OBV (On Balance Volume), EMA (Đường trung bình động hàm mũ) và tỷ lệ thân nến để xác định thời điểm mua và bán. Khi EMA ngắn hạn cắt lên trên EMA dài hạn, OBV đạt đỉnh mới trong 10 ngày, và tỷ lệ thân nến lớn hơn ngưỡng thiết lập, chiến lược sẽ mua vào tại giá mở cửa ngày hôm sau; khi giá giảm xuống dưới mức cắt lỗ hoặc giá đóng cửa giảm xuống dưới EMA ngắn hạn, chiến lược sẽ đóng vị thế.

Nguyên lý chiến lược

- Tính hai đường EMA, tham số EMA ngắn hạn là 5, EMA dài hạn là 21. Khi EMA ngắn hạn cắt lên trên EMA dài hạn, coi xu hướng tăng, ngược lại là xu hướng giảm.

- Tính chỉ báo OBV, khi OBV đạt đỉnh mới trong 10 ngày, coi động lượng tăng mạnh.

- Tính tỷ lệ thân nến, khi tỷ lệ thân nến lớn hơn ngưỡng thiết lập (mặc định 50%), coi xu hướng đã được xác nhận.

- Khi xu hướng tăng, động lượng tăng mạnh và xu hướng đã được xác nhận, chiến lược mua vào tại giá mở cửa ngày hôm sau, giá cắt lỗ là giá trị nhỏ nhất giữa giá thấp nhất trong ngày và giá mở cửa trừ 1%.

- Khi giá giảm xuống dưới giá cắt lỗ hoặc giá đóng cửa giảm xuống dưới EMA ngắn hạn, chiến lược đóng vị thế.

Phân tích ưu điểm

- Kết hợp chỉ báo xu hướng và động lượng, có thể bắt được các sản phẩm mạnh.

- Sử dụng giá mở cửa ngày hôm sau để mua và cắt lỗ động, có thể tránh được một số phá vỡ giả.

- Điều kiện cắt lỗ và chốt lời rõ ràng, rủi ro có thể kiểm soát.

Phân tích rủi ro

- Chỉ báo xu hướng và động lượng có độ trễ, có thể dẫn đến mua đuổi và cắt lỗ quá sớm.

- Tham số cố định, thiếu tính thích ứng, hiệu suất có thể khác biệt lớn trong các trạng thái thị trường khác nhau.

- Chỉ kiểm thử trên một thị trường và một sản phẩm, tính ổn định và khả năng áp dụng của chiến lược cần được xác nhận thêm.

Hướng tối ưu

- Tối ưu hóa tham số của chỉ báo xu hướng và động lượng, nâng cao độ nhạy và hiệu quả của chỉ báo.

- Đưa vào đánh giá trạng thái thị trường, điều chỉnh tham số động theo đặc điểm thị trường hiện tại.

- Mở rộng phạm vi kiểm thử, thêm các thị trường và sản phẩm khác nhau để kiểm tra, nâng cao độ ổn định của chiến lược.

- Xem xét đưa vào mô-đun quản lý vị thế và quản lý rủi ro, nâng cao tỷ lệ lợi nhuận trên rủi ro.

Tổng kết

Chiến lược giao dịch động lượng theo xu hướng Ruda là một chiến lược giao dịch định lượng đơn giản và dễ sử dụng, thông qua sự kết hợp của các chỉ báo xu hướng và động lượng, có thể bắt được các sản phẩm mạnh và cơ hội xu hướng. Tuy nhiên, chiến lược này cũng có một số hạn chế như độ trễ của chỉ báo, tham số cố định. Trong tương lai, có thể tối ưu và cải thiện chiến lược bằng cách tối ưu hóa tham số chỉ báo, đưa ra cơ chế thích ứng, mở rộng phạm vi kiểm thử và tăng cường quản lý rủi ro, nhằm nâng cao độ ổn định và khả năng sinh lời của chiến lược.

- 1