Tổng quan

Chiến lược này sử dụng nhiều đường trung bình động (VWMA), Chỉ số định hướng trung bình (ADX) và các chỉ báo định hướng (DMI) để nắm bắt cơ hội long trong thị trường Bitcoin. Bằng cách kết hợp các chỉ báo kỹ thuật như động lượng giá, xu hướng và khối lượng giao dịch, chiến lược này nhằm tìm ra điểm vào lệnh khi xu hướng tăng mạnh, động lượng đủ lớn, đồng thời kiểm soát rủi ro chặt chẽ.

Nguyên lý chiến lược

- Sử dụng VWMA 9 kỳ và 14 kỳ để xác định xu hướng long, khi đường trung bình ngắn hạn vượt lên trên đường dài hạn, tín hiệu long được phát sinh.

- Đưa vào một đường trung bình thích ứng được xây dựng từ VWMA giá cao nhất và thấp nhất 89 kỳ làm bộ lọc xu hướng, chỉ khi giá đóng cửa hoặc giá mở cửa cao hơn đường trung bình này mới xem xét mở lệnh.

- Sử dụng các chỉ báo ADX và DMI để xác nhận sức mạnh xu hướng, chỉ khi ADX lớn hơn 18 và chênh lệch giữa +DI và -DI lớn hơn 15 thì mới cho rằng xu hướng đủ mạnh.

- Tận dụng hàm phân vị khối lượng giao dịch để lọc các nến có khối lượng nằm trong khoảng 60%–95%, tránh các giai đoạn khối lượng quá thấp.

- Đặt stop loss ở mức 0,96–0,99 lần mức cao nhất của nến trước đó, và giảm dần khi khung thời gian lớn hơn, nhằm kiểm soát rủi ro.

- Đóng lệnh khi đạt thời gian nắm giữ đã định hoặc giá phá vỡ xuống dưới đường trung bình thích ứng.

Phân tích ưu điểm

- Kết hợp nhiều chỉ báo kỹ thuật, đánh giá trạng thái thị trường từ nhiều chiều như xu hướng, động lượng và khối lượng, tín hiệu đáng tin cậy hơn.

- Cơ chế lọc bằng đường trung bình thích ứng và khối lượng giao dịch giúp loại bỏ hiệu quả các tín hiệu giả, giảm thiểu giao dịch không hiệu quả.

- Cài đặt stop loss chặt chẽ và giới hạn thời gian nắm giữ giúp giảm đáng kể rủi ro của chiến lược.

- Mã được thiết kế theo mô-đun, dễ đọc và dễ bảo trì, thuận tiện cho việc tối ưu hóa và mở rộng.

Phân tích rủi ro

- Khi thị trường dao động hoặc xu hướng không rõ ràng, chiến lược này có thể phát sinh nhiều tín hiệu giả.

- Vị trí stop loss tương đối gần, khi biến động giá lớn có thể kích hoạt stop loss quá sớm, dẫn đến thua lỗ lớn hơn.

- Thiếu cân nhắc đến tình hình kinh tế vĩ mô và các sự kiện trọng đại, có thể thất bại trước các sự kiện "thiên nga đen".

- Các tham số được cài đặt tương đối cố định, thiếu tính thích ứng, hiệu suất có thể không ổn định trong các điều kiện thị trường khác nhau.

Hướng tối ưu hóa

- Đưa thêm các chỉ báo có thể mô tả môi trường thị trường, như Chỉ số sức mạnh tương đối (RSI), Bollinger Bands, v.v., để nâng cao độ tin cậy của tín hiệu.

- Tối ưu hóa vị trí stop loss một cách linh hoạt, ví dụ sử dụng ATR hoặc stop loss theo phần trăm, để ứng phó với các điều kiện biến động thị trường khác nhau.

- Kết hợp dữ liệu kinh tế vĩ mô và phân tích dư luận để tăng cường mô-đun kiểm soát rủi ro của chiến lược.

- Sử dụng thuật toán học máy để tự động tối ưu hóa các tham số, nâng cao tính thích ứng và ổn định của chiến lược.

Tổng kết

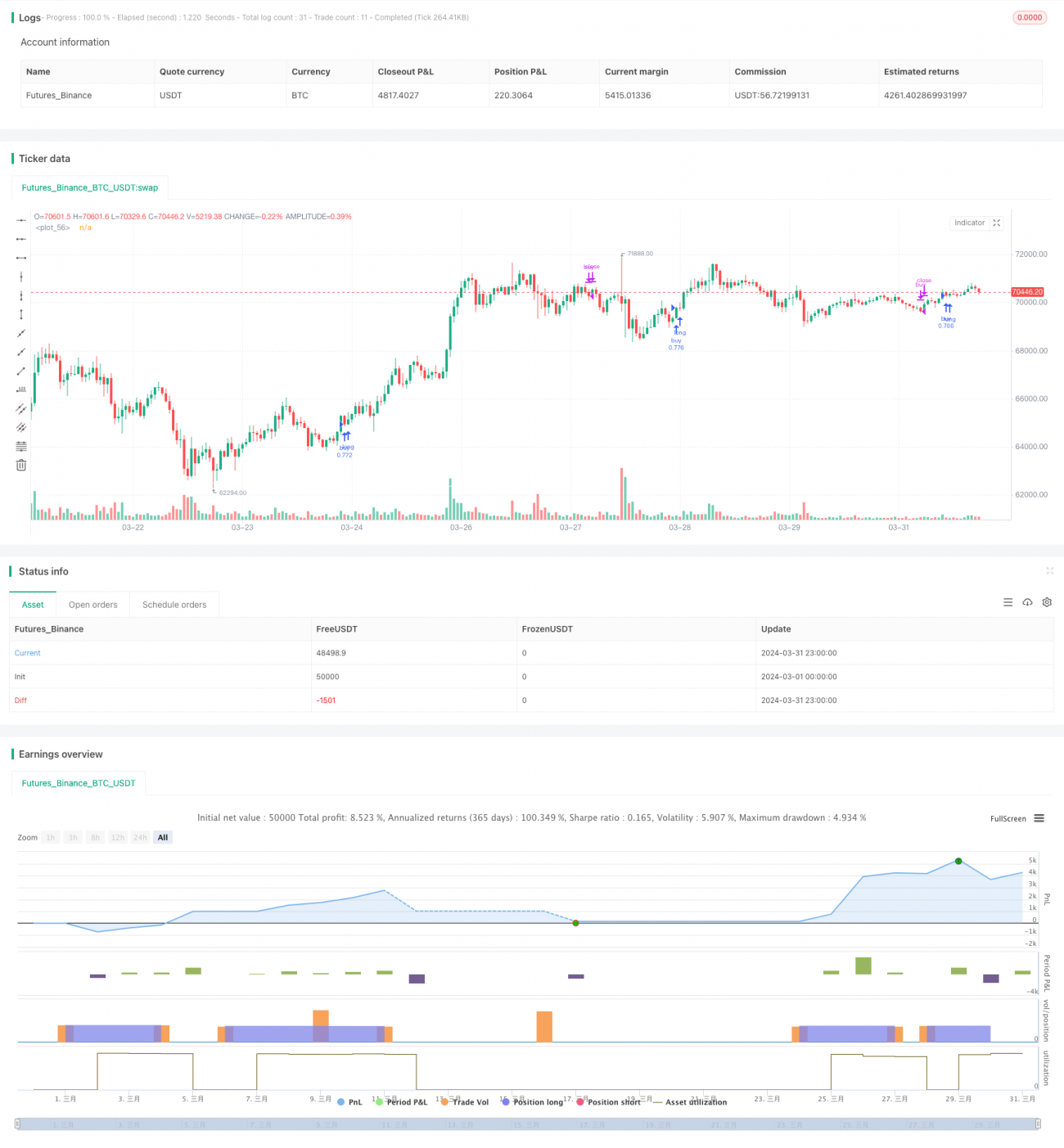

Chiến lược long Bitcoin VWMA-ADX, bằng cách xem xét tổng hợp nhiều chỉ báo kỹ thuật như xu hướng giá, động lượng và khối lượng giao dịch, có thể nắm bắt hiệu quả các cơ hội tăng giá trong thị trường Bitcoin. Đồng thời, các biện pháp kiểm soát rủi ro chặt chẽ và điều kiện đóng lệnh rõ ràng giúp kiểm soát rủi ro tốt. Tuy nhiên, chiến lược này cũng có một số hạn chế, chẳng hạn như khả năng thích ứng với sự thay đổi của môi trường thị trường chưa đủ, chiến lược stop loss cần được tối ưu hóa, v.v. Trong tương lai, có thể cải thiện từ độ tin cậy của tín hiệu, kiểm soát rủi ro, tối ưu hóa tham số, v.v., để nâng cao hơn nữa tính ổn định và khả năng sinh lời của chiến lược. Nhìn chung, Chiến lược long Bitcoin VWMA-ADX cung cấp cho nhà đầu tư một tư duy giao dịch hệ thống dựa trên động lượng và xu hướng, đáng để khám phá và cải tiến thêm.

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Q_D_Nam_N_96

//@version=5

- 1