Chiến lược theo dõi xu hướng đa chỉ báo

Tổng quan

Chiến lược có tên "Jancok Strategycs v3" là chiến lược giao dịch theo xu hướng đa chỉ báo dựa trên đường trung bình động (MA), sự phân kỳ hội tụ đường trung bình động (MACD), chỉ số sức mạnh tương đối (RSI) và dải trung bình thực (ATR). Ý tưởng chính của chiến lược là sử dụng sự kết hợp của nhiều chỉ báo để đánh giá xu hướng thị trường và giao dịch theo hướng xu hướng. Đồng thời, chiến lược cũng áp dụng phương pháp cắt lỗ và chốt lời động, cùng với quản lý rủi ro dựa trên ATR để kiểm soát rủi ro và tối ưu hóa lợi nhuận.

Nguyên lý chiến lược

Chiến lược sử dụng bốn chỉ báo sau để đánh giá xu hướng thị trường:

- Đường trung bình động (MA): Tính toán đường trung bình động ngắn hạn (9 kỳ) và dài hạn (21 kỳ). Khi đường trung bình ngắn hạn cắt lên trên đường trung bình dài hạn, cho thấy xu hướng tăng; khi đường trung bình ngắn hạn cắt xuống dưới đường trung bình dài hạn, cho thấy xu hướng giảm.

- Sự phân kỳ hội tụ đường trung bình động (MACD): Tính toán đường MACD và đường tín hiệu. Khi đường MACD cắt lên trên đường tín hiệu, cho thấy xu hướng tăng; khi đường MACD cắt xuống dưới đường tín hiệu, cho thấy xu hướng giảm.

- Chỉ số sức mạnh tương đối (RSI): Tính toán RSI 14 kỳ. Khi RSI lớn hơn 70, thị trường có thể quá mua; khi RSI nhỏ hơn 30, thị trường có thể quá bán.

- Dải trung bình thực (ATR): Tính toán ATR 14 kỳ, dùng để đo lường biến động thị trường và thiết lập điểm cắt lỗ/chốt lời.

Logic giao dịch của chiến lược như sau:

- Khi đường trung bình ngắn hạn cắt lên trên đường trung bình dài hạn, đường MACD cắt lên trên đường tín hiệu, khối lượng giao dịch lớn hơn đường trung bình động của nó, và biến động thấp hơn ngưỡng, mở lệnh mua (long).

- Khi đường trung bình ngắn hạn cắt xuống dưới đường trung bình dài hạn, đường MACD cắt xuống dưới đường tín hiệu, khối lượng giao dịch lớn hơn đường trung bình động của nó, và biến động thấp hơn ngưỡng, mở lệnh bán (short).

- Điểm cắt lỗ và chốt lời được thiết lập động dựa trên ATR. Điểm cắt lỗ là 2 lần ATR, điểm chốt lời là 4 lần ATR.

- Có thể chọn sử dụng cắt lỗ trailing dựa trên ATR, với mức cắt lỗ trailing là 2,5 lần ATR.

Ưu điểm của chiến lược

- Kết hợp nhiều chỉ báo để đánh giá xu hướng, tăng độ chính xác của việc xác định xu hướng.

- Cắt lỗ và chốt lời động, tự động điều chỉnh theo biến động thị trường, kiểm soát rủi ro tốt hơn và tối ưu hóa lợi nhuận.

- Đưa vào bộ lọc khối lượng và biến động, tránh giao dịch khi thanh khoản thấp và biến động cao, giảm tín hiệu nhiễu.

- Có thể chọn cắt lỗ trailing, giữ lại nhiều lợi nhuận hơn khi xu hướng tiếp diễn.

Rủi ro của chiến lược

- Trong thị trường đi ngang hoặc khi xu hướng đảo chiều, có thể phát sinh tín hiệu giả, dẫn đến thua lỗ.

- Việc thiết lập tham số có ảnh hưởng lớn đến hiệu suất chiến lược, cần tối ưu hóa cho từng thị trường và tài sản khác nhau.

- Tối ưu hóa quá mức tham số có thể dẫn đến overfitting, hoạt động kém trong giao dịch thực tế.

- Khi xảy ra biến động bất thường hoặc sự kiện thiên nga đen, chiến lược có thể chịu tổn thất lớn.

Hướng tối ưu hóa chiến lược

- Đưa vào thêm nhiều chỉ báo, như Bollinger Bands, Stochastic, v.v., để nâng cao độ chính xác xác định xu hướng.

- Tối ưu hóa lựa chọn tham số, sử dụng các phương pháp như thuật toán di truyền, tìm kiếm lưới, để tìm ra tổ hợp tham số tối ưu.

- Đối với các thị trường và tài sản khác nhau, thiết lập tham số và quy tắc khác nhau, tăng khả năng thích ứng của chiến lược.

- Thêm quản lý vị thế, điều chỉnh động quy mô vị thế dựa trên sức mạnh xu hướng thị trường và rủi ro tài khoản.

- Thiết lập giới hạn drawdown tối đa, khi tài khoản đạt drawdown tối đa, tạm dừng giao dịch hoặc giảm quy mô vị thế để kiểm soát rủi ro.

Tổng kết

"Jancok Strategycs v3" là một chiến lược theo xu hướng dựa trên sự kết hợp nhiều chỉ báo, sử dụng các chỉ báo như đường trung bình động, MACD, RSI và ATR để đánh giá xu hướng thị trường, và áp dụng các biện pháp quản lý rủi ro như cắt lỗ chốt lời động và cắt lỗ trailing để kiểm soát rủi ro và tối ưu hóa lợi nhuận. Ưu điểm của chiến lược này bao gồm độ chính xác cao trong việc xác định xu hướng, quản lý rủi ro linh hoạt và khả năng thích ứng tốt. Tuy nhiên, cũng tồn tại một số rủi ro nhất định, như tín hiệu giả, độ nhạy của tham số và sự kiện thiên nga đen. Trong tương lai, có thể nâng cao hiệu suất và độ ổn định của chiến lược bằng cách đưa vào thêm chỉ báo, tối ưu hóa lựa chọn tham số, thêm quản lý vị thế và thiết lập giới hạn drawdown tối đa.

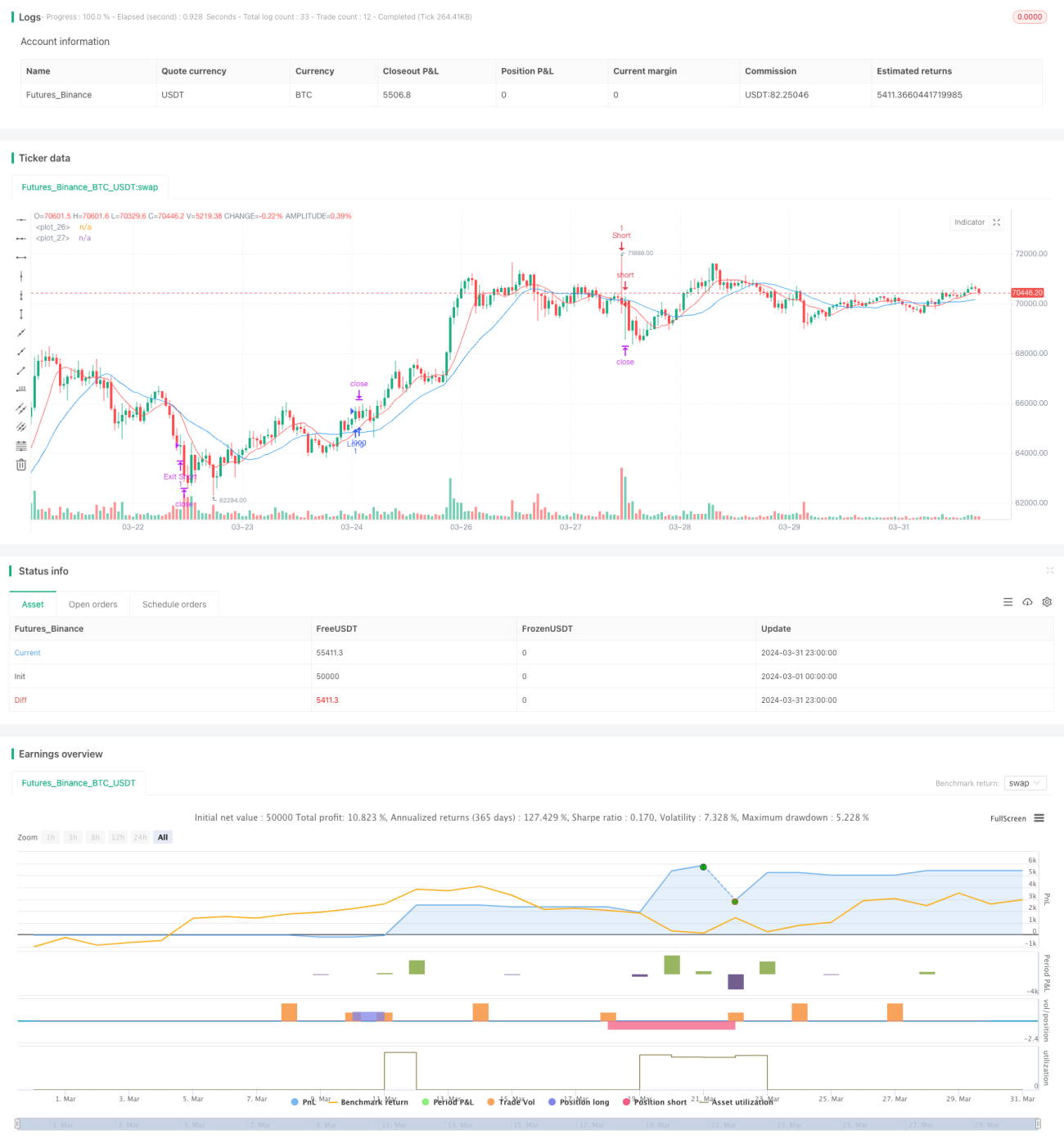

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © financialAccou42381

//@version=5- 1