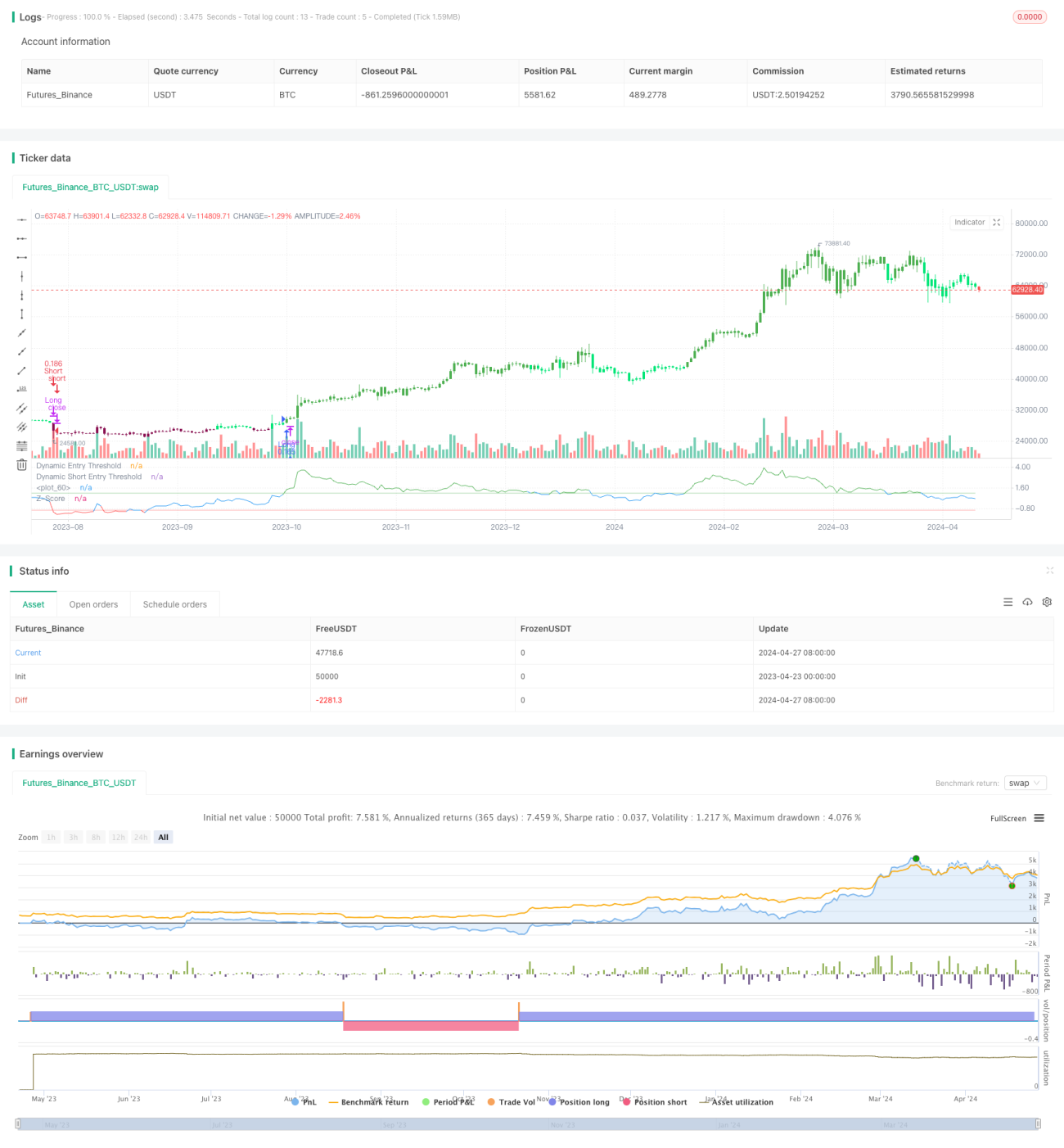

Chiến lược theo dõi xu hướng dựa trên giá trị Z

Tổng quan

"Chiến lược giao dịch theo xu hướng dựa trên Z-score" sử dụng chỉ số thống kê Z-score, đo lường mức độ chênh lệch của giá so với đường trung bình động, lấy độ lệch chuẩn làm thước đo chuẩn hóa, để nắm bắt các cơ hội xu hướng. Chiến lược này nổi tiếng với sự đơn giản và hiệu quả, đặc biệt phù hợp với các thị trường nơi giá thường có xu hướng quay về giá trị trung bình. Không giống như các hệ thống phức tạp phụ thuộc vào nhiều chỉ báo, "Chiến lược Z-score xu hướng" tập trung vào các biến động giá rõ ràng, có ý nghĩa thống kê, rất phù hợp với các nhà giao dịch ưa thích phương pháp tinh gọn, dựa trên dữ liệu.

Nguyên lý chiến lược

Cốt lõi của chiến lược này là tính toán Z-score. Z-score được tính bằng cách lấy chênh lệch giữa giá hiện tại và đường trung bình động hàm mũ (EMA) có độ dài do người dùng xác định, sau đó chia cho độ lệch chuẩn của giá cùng độ dài đó:

z = (x - μ) / σ

Trong đó, x là giá hiện tại, μ là giá trị trung bình EMA, σ là độ lệch chuẩn.

Tín hiệu giao dịch được tạo ra dựa trên việc Z-score vượt qua các ngưỡng định trước:

- Vào lệnh mua: Khi Z-score vượt lên trên ngưỡng dương.

- Thoát lệnh mua: Khi Z-score vượt xuống dưới ngưỡng âm.

- Vào lệnh bán: Khi Z-score vượt xuống dưới ngưỡng âm.

- Thoát lệnh bán: Khi Z-score vượt lên trên ngưỡng dương.

Ưu điểm của chiến lược

- Đơn giản và hiệu quả: Chiến lược chỉ phụ thuộc vào một vài tham số, dễ hiểu và dễ thực hiện, đồng thời rất hiệu quả trong việc nắm bắt các cơ hội xu hướng.

- Cơ sở thống kê: Z-score là một công cụ thống kê đã được kiểm chứng, cung cấp nền tảng lý thuyết vững chắc cho chiến lược.

- Tính linh hoạt cao: Bằng cách điều chỉnh các tham số như ngưỡng, chu kỳ tính EMA và độ lệch chuẩn, chiến lược có thể linh hoạt thích ứng với các phong cách giao dịch và điều kiện thị trường khác nhau.

- Tín hiệu rõ ràng: Các tín hiệu giao dịch dựa trên việc Z-score vượt ngưỡng rất đơn giản, rõ ràng, tạo điều kiện cho việc ra quyết định và thực hiện nhanh chóng.

Rủi ro của chiến lược

- Nhạy cảm với tham số: Việc thiết lập tham số không phù hợp (ví dụ ngưỡng quá cao hoặc quá thấp) có thể dẫn đến tín hiệu giao dịch sai lệch, bỏ lỡ cơ hội hoặc gây thua lỗ.

- Nhận diện xu hướng: Trong thị trường dao động hoặc đi ngang, chiến lược có thể gặp nhiều tín hiệu giả, hiệu suất kém.

- Hiệu ứng trễ: Là một chiến lược theo xu hướng, các tín hiệu vào và thoát lệnh đều có độ trễ nhất định, có thể bỏ lỡ thời điểm tốt nhất.

Các rủi ro trên có thể được kiểm soát và giảm thiểu thông qua việc phân tích thị trường liên tục, tối ưu hóa tham số và thực hiện thận trọng dựa trên kết quả backtest.

Hướng tối ưu hóa chiến lược

- Ngưỡng động: Đưa vào ngưỡng động liên quan đến biến động, có thể thích ứng hiệu quả với các trạng thái thị trường khác nhau, nâng cao chất lượng tín hiệu.

- Kết hợp chỉ báo: Kết hợp các chỉ báo kỹ thuật khác như RSI, MACD để xác nhận lại tín hiệu giao dịch, tăng độ tin cậy.

- Quản lý vị thế: Đưa vào cơ chế kiểm soát vị thế như ATR, giảm vị thế kịp thời trong thị trường dao động, tăng vị thế kịp thời trong thị trường xu hướng, tối ưu hóa tỷ lệ lợi nhuận/rủi ro.

- Đa khung thời gian: Tính Z-score trên nhiều khung thời gian khác nhau, nắm bắt các xu hướng ở các cấp độ khác nhau, làm phong phú thêm chiều hướng của chiến lược.

Tổng kết

"Chiến lược giao dịch theo xu hướng dựa trên Z-score" với đặc điểm đơn giản, ổn định và linh hoạt, mang lại góc nhìn độc đáo để nắm bắt các cơ hội xu hướng. Thông qua việc thiết lập tham số hợp lý, quản lý rủi ro thận trọng và tối ưu hóa liên tục, chiến lược này hứa hẹn trở thành công cụ đắc lực cho các nhà giao dịch định lượng, tiến bước vững chắc trong thị trường biến động.

/*backtest

start: 2023-04-23 00:00:00

end: 2024-04-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy employs a statistical approach by using a Z-score, which measures the deviation of the price from its moving average normalized by the standard deviation.- 1