Chiến lược giao cắt giữa giá trung bình gia quyền khối lượng và chỉ số sức mạnh tương đối

Tổng Quan

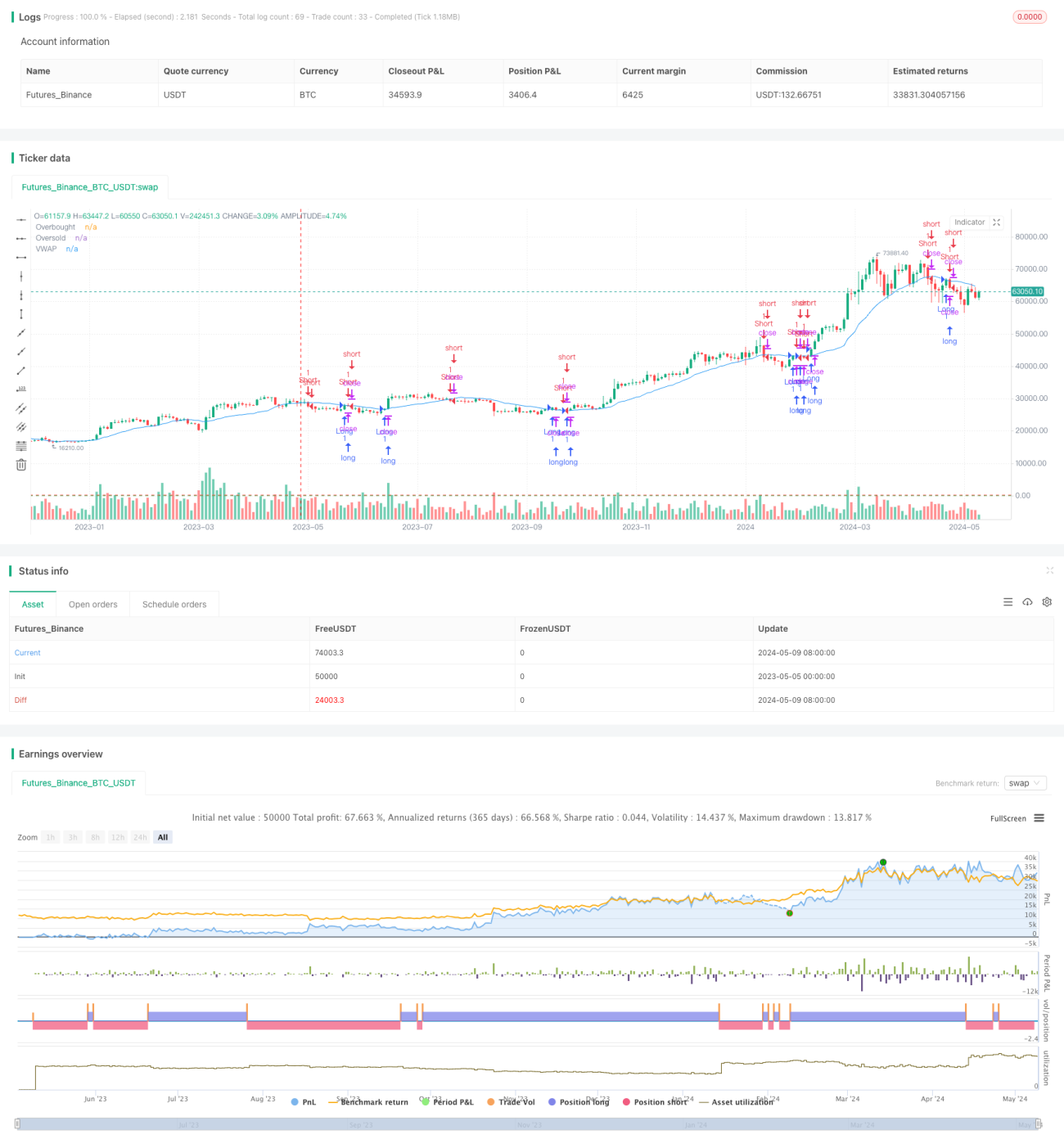

Chiến lược này dựa trên sự giao cắt của hai đường VWAP với các chu kỳ khác nhau, kết hợp với chỉ báo RSI để xác nhận tín hiệu giao dịch. Khi giá phá vỡ lên trên đường VWAP và RSI cao hơn mức quá bán, tín hiệu mua được tạo ra; khi giá phá vỡ xuống dưới đường VWAP và RSI thấp hơn mức quá mua, tín hiệu bán được tạo ra. Chiến lược này nhằm mục đích bắt kịp các đợt phá vỡ giá so với VWAP, đồng thời sử dụng chỉ báo RSI để lọc các tín hiệu phá vỡ giả tiềm năng.

Nguyên Lý Chiến Lược

- Tính toán giá trị VWAP trong một chu kỳ nhất định. VWAP là giá trung bình gia quyền theo khối lượng, phản ánh chi phí nắm giữ trung bình của những người tham gia thị trường trong một khoảng thời gian.

- Tính toán chỉ báo RSI. RSI đo lường sức mạnh tương đối của giá trong một khoảng thời gian, được sử dụng để xác định xem thị trường đang quá mua hay quá bán.

- Khi giá đóng cửa phá vỡ lên trên đường VWAP và RSI cao hơn mức quá bán (mặc định là 30), tín hiệu mua được tạo ra.

- Khi giá đóng cửa phá vỡ xuống dưới đường VWAP và RSI thấp hơn mức quá mua (mặc định là 70), tín hiệu bán được tạo ra.

- Khi đang nắm giữ vị thế mua, nếu giá đóng cửa phá vỡ xuống dưới đường VWAP hoặc RSI cao hơn mức quá mua, thì đóng vị thế.

- Khi đang nắm giữ vị thế bán, nếu giá đóng cửa phá vỡ lên trên đường VWAP hoặc RSI thấp hơn mức quá bán, thì đóng vị thế.

Ưu Điểm Của Chiến Lược

- Kết hợp thông tin về giá và khối lượng. VWAP xem xét cả giá và khối lượng, phản ánh xu hướng thị trường một cách toàn diện hơn.

- Sử dụng chỉ báo RSI để xác nhận xu hướng và lọc các tín hiệu giả. RSI giúp đánh giá độ tin cậy của các đợt phá vỡ, giảm thiểu sai sót.

- Chiến lược phá vỡ dễ hiểu và dễ thực hiện. Chiến lược này có logic rõ ràng, phù hợp cho người mới bắt đầu học và sử dụng.

- Áp dụng được cho nhiều khung thời gian. Bằng cách điều chỉnh chu kỳ tính toán VWAP và RSI, chiến lược này có thể phù hợp với các phong cách giao dịch và thị trường khác nhau.

Rủi Ro Của Chiến Lược

- Việc lựa chọn tham số cho VWAP và RSI ảnh hưởng đến hiệu suất của chiến lược. Thiết lập tham số không phù hợp có thể dẫn đến giao dịch quá thường xuyên hoặc bỏ lỡ cơ hội.

- Trong thị trường không có xu hướng rõ ràng hoặc có độ biến động thấp, chiến lược này có thể tạo ra nhiều tín hiệu giả.

- Chiến lược này chưa xem xét đến quản lý rủi ro, như cắt lỗ và kiểm soát vị thế. Trong ứng dụng thực tế cần kết hợp các biện pháp quản lý rủi ro.

- Chiến lược phá vỡ dễ bị thua lỗ trong thị trường đi ngang. Khi giá dao động quanh VWAP, chiến lược này có thể giao dịch thường xuyên và dẫn đến thua lỗ.

Hướng Tối Ưu Hóa Chiến Lược

- Giới thiệu VWAP và RSI đa khung thời gian. Bằng cách kết hợp các chỉ báo với chu kỳ khác nhau để tăng độ tin cậy và tính ổn định của tín hiệu.

- Thêm các chỉ báo xác nhận xu hướng, như đường trung bình động hoặc ADX. Chỉ giao dịch theo hướng xu hướng rõ ràng có thể cải thiện tỷ lệ thắng và tỷ lệ lợi nhuận/rủi ro.

- Tối ưu hóa quy tắc vào và thoát lệnh. Ví dụ: yêu cầu giá vượt quá VWAP một tỷ lệ nhất định khi phá vỡ, hoặc sử dụng ATR làm bộ lọc.

- Kết hợp với các chỉ báo kỹ thuật khác, như Bollinger Bands hoặc chỉ báo động lượng. Việc xác nhận chung từ nhiều chỉ báo có thể nâng cao chất lượng tín hiệu.

- Thêm quản lý rủi ro, như cắt lỗ và kiểm soát vị thế động. Thiết lập hợp lý mức cắt lỗ có thể giảm rủi ro cho mỗi giao dịch, điều chỉnh vị thế động có thể nâng cao hiệu quả sử dụng vốn.

Tổng Kết

Chiến lược giao cắt giữa giá trung bình gia quyền theo khối lượng và chỉ số sức mạnh tương đối là một phương pháp giao dịch đơn giản và dễ sử dụng, thu lợi nhuận tiềm năng bằng cách bắt kịp các đợt phá vỡ giá so với VWAP. Tuy nhiên, chiến lược này cũng tồn tại các vấn đề như tối ưu tham số, hoạt động kém trong thị trường đi ngang, thiếu quản lý rủi ro. Bằng cách giới thiệu phân tích đa khung thời gian, kết hợp với các chỉ báo kỹ thuật khác, tối ưu hóa quy tắc vào/ra lệnh và thêm kiểm soát rủi ro, có thể nâng cao hơn nữa tính ổn định và tính thực tiễn của chiến lược. Nhà giao dịch khi áp dụng chiến lược này cần điều chỉnh và tối ưu hóa phù hợp với phong cách giao dịch và đặc điểm thị trường của riêng mình.

- 1