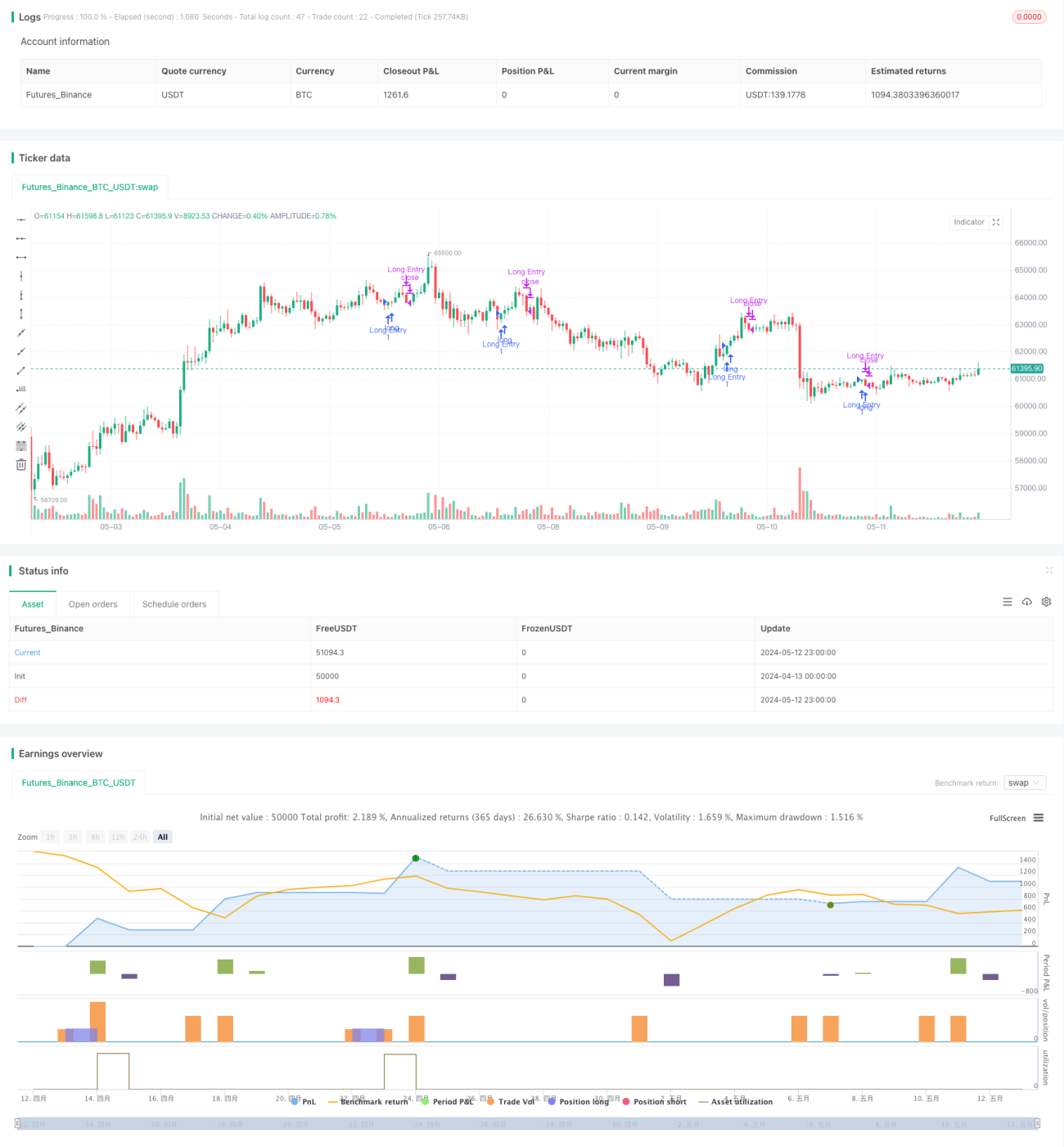

Tổng quan

Chiến lược này chủ yếu tìm kiếm các nến tăng không có bấc trên (râu trên) làm tín hiệu mua, và đóng vị thế khi giá phá vỡ đáy của nến trước đó. Chiến lược tận dụng đặc điểm bấc trên của nến tăng rất nhỏ, cho thấy lực mua mạnh mẽ và khả năng giá tiếp tục tăng cao. Đồng thời, đáy của nến trước đó được dùng làm điểm dừng lỗ để kiểm soát rủi ro hiệu quả.

Nguyên lý chiến lược

- Xác định xem nến hiện tại có phải là nến tăng hay không (giá đóng cửa cao hơn giá mở cửa)

- Tính tỷ lệ độ dài bấc trên so với độ dài thân nến hiện tại

- Nếu tỷ lệ bấc trên nhỏ hơn 5%, coi đó là nến tăng không có bấc trên hợp lệ và phát tín hiệu mua

- Ghi lại giá thấp nhất của nến trước đó sau khi mua làm điểm dừng lỗ

- Khi giá phá vỡ điểm dừng lỗ, đóng vị thế và thoát lệnh

Lợi thế của chiến lược

- Chọn nến tăng không có bấc trên để vào lệnh, xu hướng mạnh hơn, tỷ lệ thành công cao hơn

- Sử dụng đáy của nến trước đó làm điểm dừng lỗ, rủi ro có thể kiểm soát

- Logic đơn giản, dễ triển khai và tối ưu hóa

- Phù hợp sử dụng trong thị trường có xu hướng

Rủi ro của chiến lược

- Có thể xảy ra trường hợp sau tín hiệu mua, giá lùi ngay lập tức chạm dừng lỗ

- Đối với các công cụ biến động cao, điểm dừng lỗ có thể đặt quá gần giá mua, dẫn đến dừng lỗ sớm

- Thiếu mục tiêu lợi nhuận, khó nắm bắt thời điểm thoát lệnh tối ưu

Hướng tối ưu hóa chiến lược

- Có thể kết hợp với các chỉ báo khác như MA, MACD... để xác nhận độ mạnh của xu hướng, nâng cao hiệu quả tín hiệu vào lệnh

- Đối với các công cụ biến động cao, có thể đặt điểm dừng lỗ ở vị trí xa hơn, chẳng hạn như đáy của N nến trước đó, giảm tần suất dừng lỗ

- Đưa ra mục tiêu lợi nhuận, như N lần ATR hoặc phần trăm lợi nhuận, để khóa lợi nhuận kịp thời

- Cân nhắc thêm quản lý vị thế, như điều chỉnh kích thước vị thế dựa trên độ mạnh tín hiệu

Tổng kết

Chiến lược này chọn nến tăng không có bấc trên để vào lệnh và dùng đáy nến trước đó làm dừng lỗ, có thể thu lợi nhuận hiệu quả trong thị trường xu hướng. Tuy nhiên, chiến lược cũng có những hạn chế nhất định, như điểm dừng lỗ không linh hoạt, thiếu mục tiêu lợi nhuận. Có thể cải thiện bằng cách đưa vào các chỉ báo khác để lọc tín hiệu, tối ưu vị trí dừng lỗ và đặt mục tiêu lợi nhuận, giúp chiến lược trở nên mạnh mẽ và hiệu quả hơn.

Overview

The main idea of this strategy is to find bullish candles without upper wicks as buy signals and close positions when the price breaks below the low of the previous candle. The strategy utilizes the characteristic of bullish candles with very small upper wicks, indicating strong bullish momentum and a higher probability of continued price increases. At the same time, using the low of the previous candle as a stop-loss level can effectively control risk.

Strategy Principles

- Determine if the current candle is a bullish candle (close price higher than open price)

- Calculate the ratio of the current candle's upper wick length to its body length

- If the upper wick ratio is less than 5%, consider it a valid bullish candle without an upper wick and generate a buy signal

- Record the lowest price of the previous candle after buying as the stop-loss level

- When the price breaks below the stop-loss level, close the position and exit

Strategy Advantages

- Selecting bullish candles without upper wicks for entry, the trend strength is greater and the success rate is higher

- Using the low of the previous candle as the stop-loss level, risks are controllable

- Simple logic, easy to implement and optimize

- Suitable for use in trending markets

Strategy Risks

- There may be cases where a buy signal is followed by an immediate pullback triggering the stop-loss

- For highly volatile instruments, the stop-loss level may be set too close to the buy price, leading to premature stop-outs

- Lack of profit targets, making it difficult to grasp the optimal exit timing

Strategy Optimization Directions

- Combine with other indicators such as MA, MACD, etc., to confirm trend strength and improve the effectiveness of entry signals

- For highly volatile instruments, set the stop-loss level at a further position, such as the lowest point of the previous N candles, to reduce the stop-loss frequency

- Introduce profit targets, such as N times ATR or percentage gains, to lock in profits in a timely manner

- Consider adding position management, such as adjusting position size based on signal strength

Summary

This strategy captures profits effectively in trending markets by selecting bullish candles without upper wicks for entry and using the low of the previous candle for stop-loss. However, the strategy also has certain limitations, such as inflexible stop-loss placement and lack of profit targets. Improvements can be made by introducing other indicators to filter signals, optimizing stop-loss positions, and setting profit targets to make the strategy more robust and effective.

- 1