Chiến lược dừng lỗ theo ATR trong giao dịch theo xu hướng

Tổng quan

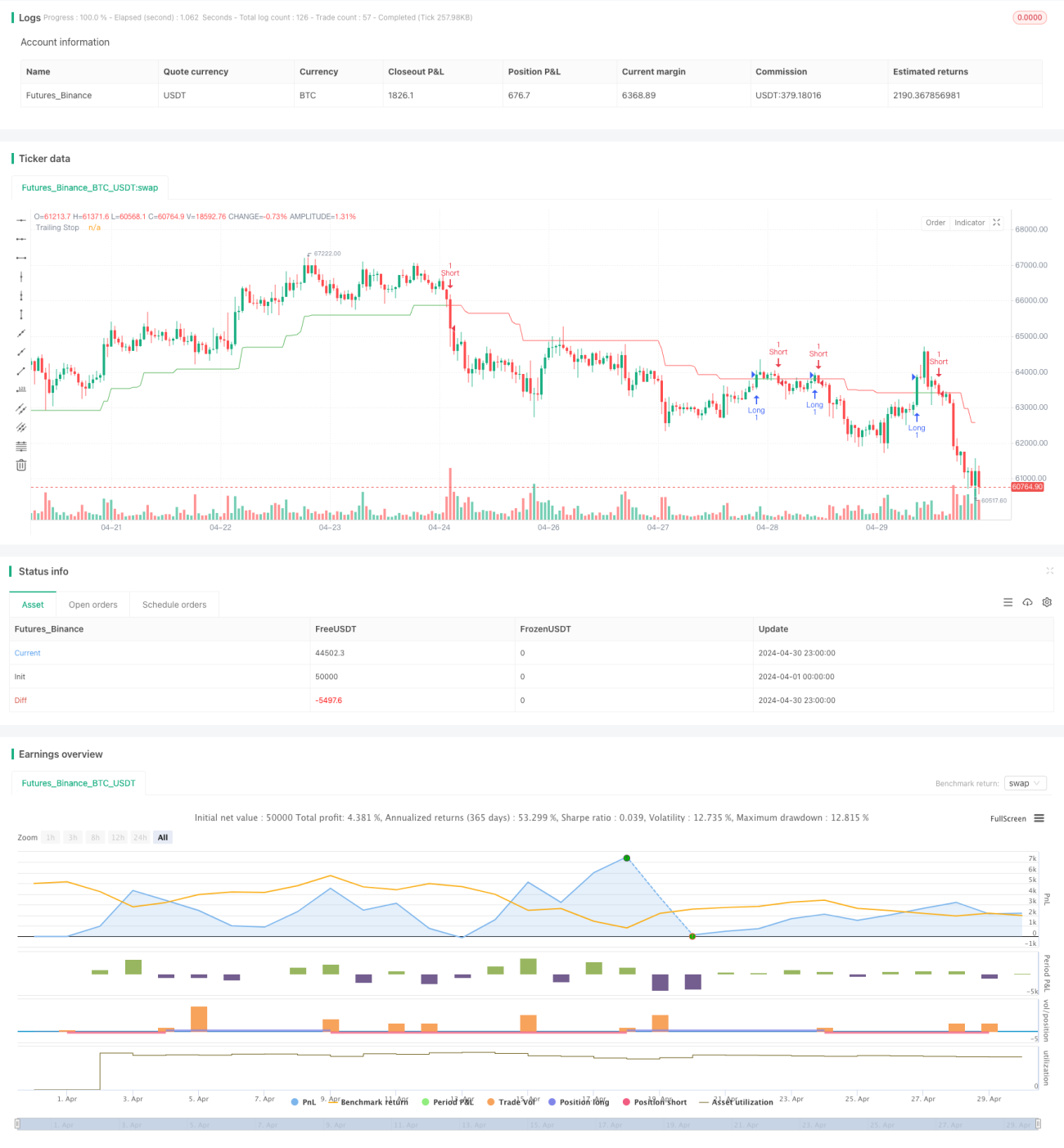

Chiến lược này sử dụng ATR (Average True Range) làm cơ sở cho trailing stop (TS), điều chỉnh vị trí dừng lỗ một cách linh hoạt để theo dõi xu hướng. Khi giá di chuyển theo hướng có lợi, vị trí dừng lỗ cũng được điều chỉnh theo, qua đó khóa lợi nhuận đã đạt được; khi giá di chuyển theo hướng bất lợi, vị trí dừng lỗ không thay đổi, một khi giá chạm mức dừng lỗ, sẽ đóng lệnh và cắt lỗ. Điểm mấu chốt của chiến lược nằm ở việc điều chỉnh động vị trí dừng lỗ, vừa có thể bảo vệ lợi nhuận đã đạt được, vừa cho phép lợi nhuận tiếp tục mở rộng khi xu hướng kéo dài.

Nguyên lý chiến lược

- Tính toán ATR, làm cơ sở cho trailing stop. ATR phản ánh mức độ biến động của thị trường, được dùng để đo lường biên độ giá trung bình.

- Dựa trên ATR và tham số KeyValue để tính khoảng cách dừng lỗ nLoss. KeyValue là bội số do người dùng tự xác định, nLoss là tích của KeyValue và ATR, biểu thị khoảng cách dừng lỗ gấp bao nhiêu lần ATR.

- Tính toán vị trí trailing stop động xATRTrailingStop. Khi nắm giữ vị thế mua, đặt nó bằng "giá trị lớn hơn giữa mức giá cao nhất của nến trước đó và (giá đóng cửa - nLoss)"; khi nắm giữ vị thế bán, đặt nó bằng "giá trị nhỏ hơn giữa mức giá thấp nhất của nến trước đó và (giá đóng cửa + nLoss)".

- Tạo tín hiệu mở lệnh. Khi giá đóng cửa vượt lên trên xATRTrailingStop, mua vào; khi giá đóng cửa phá xuống dưới xATRTrailingStop, bán ra.

Phân tích ưu điểm

- Vị trí dừng lỗ được điều chỉnh động theo biến động giá, vừa khóa được lợi nhuận, vừa cho phép lợi nhuận mở rộng khi xu hướng tiếp diễn.

- Vị trí dừng lỗ dựa trên ATR, có thể phản ánh khách quan mức độ biến động thị trường, linh hoạt và hiệu quả hơn so với mức dừng lỗ cố định do chủ quan đặt ra.

- Thông qua tham số KeyValue để khuếch đại ATR, người dùng có thể đặt khoảng cách dừng lỗ phù hợp dựa trên mức chấp nhận rủi ro của riêng mình, KeyValue lớn hơn sẽ tạo ra khoảng không dừng lỗ rộng hơn và tần suất cắt lỗ thấp hơn.

Phân tích rủi ro

- Chiến lược theo xu hướng hoạt động kém trong thị trường đi ngang (sideways), khi xu hướng một chiều không rõ ràng sẽ dẫn đến cắt lỗ liên tục, gây thất thoát vốn nhanh chóng.

- Thời điểm vào lệnh phụ thuộc vào tín hiệu giao nhau giữa giá đóng cửa và đường dừng lỗ động, trong thị trường đi ngang có thể xảy ra các lần cắt lỗ nhỏ liên tiếp.

- Chiến lược trailing stop không thể tránh khỏi các gap (khoảng trống giá) do tin tức xấu hoặc tốt cực lớn, tốc độ điều chỉnh vị trí dừng lỗ không theo kịp tốc độ biến động giá, dẫn đến tổn thất thực tế lớn hơn nhiều so với mức kiểm soát rủi ro dự kiến.

Hướng tối ưu hóa

- Có thể thêm các chỉ báo xác định xu hướng vào chiến lược, như hệ thống đường trung bình động (MA), chỉ báo động lượng (momentum), v.v., chỉ vào lệnh khi xu hướng rõ ràng, tránh giao dịch quá nhiều trong thị trường đi ngang.

- Có thể xem xét đưa ra chiến lược chốt lời, chẳng hạn như tính toán kích thước vị thế dựa trên công thức Kelly, đặt mức chốt lời theo điểm dừng lợi nhuận cố định (fixed profit target) hoặc chốt lời khi lợi nhuận bị rút lui một phần (trailing profit), để giảm khả năng lợi nhuận tiềm năng bị thoái lui vào cuối xu hướng.

- Đối với gap, có thể đặt giới hạn dừng lỗ tối đa, chẳng hạn như số tiền cố định hoặc tỷ lệ phần trăm cố định, một khi đạt đến giới hạn đó, bất kể vị trí dừng lỗ động ở đâu, đều cắt lỗ ngay lập tức.

Tổng kết

Chiến lược trailing stop dựa trên ATR có thể điều chỉnh linh hoạt vị trí dừng lỗ theo biên độ biến động giá, đạt hiệu quả tốt trong các thị trường có xu hướng. Tuy nhiên, chiến lược này cũng tồn tại các rủi ro như không xử lý được thị trường đi ngang, cắt lỗ quá thường xuyên và khó tránh khỏi các gap. Đối với những khiếm khuyết trên, có thể tối ưu hóa và cải thiện chiến lược từ các khía cạnh như xác định xu hướng, chiến lược chốt lời, giới hạn dừng lỗ tối đa, v.v. Thông qua những điều chỉnh này, kỳ vọng sẽ nâng cao khả năng thích ứng và lợi nhuận của chiến lược.

- 1