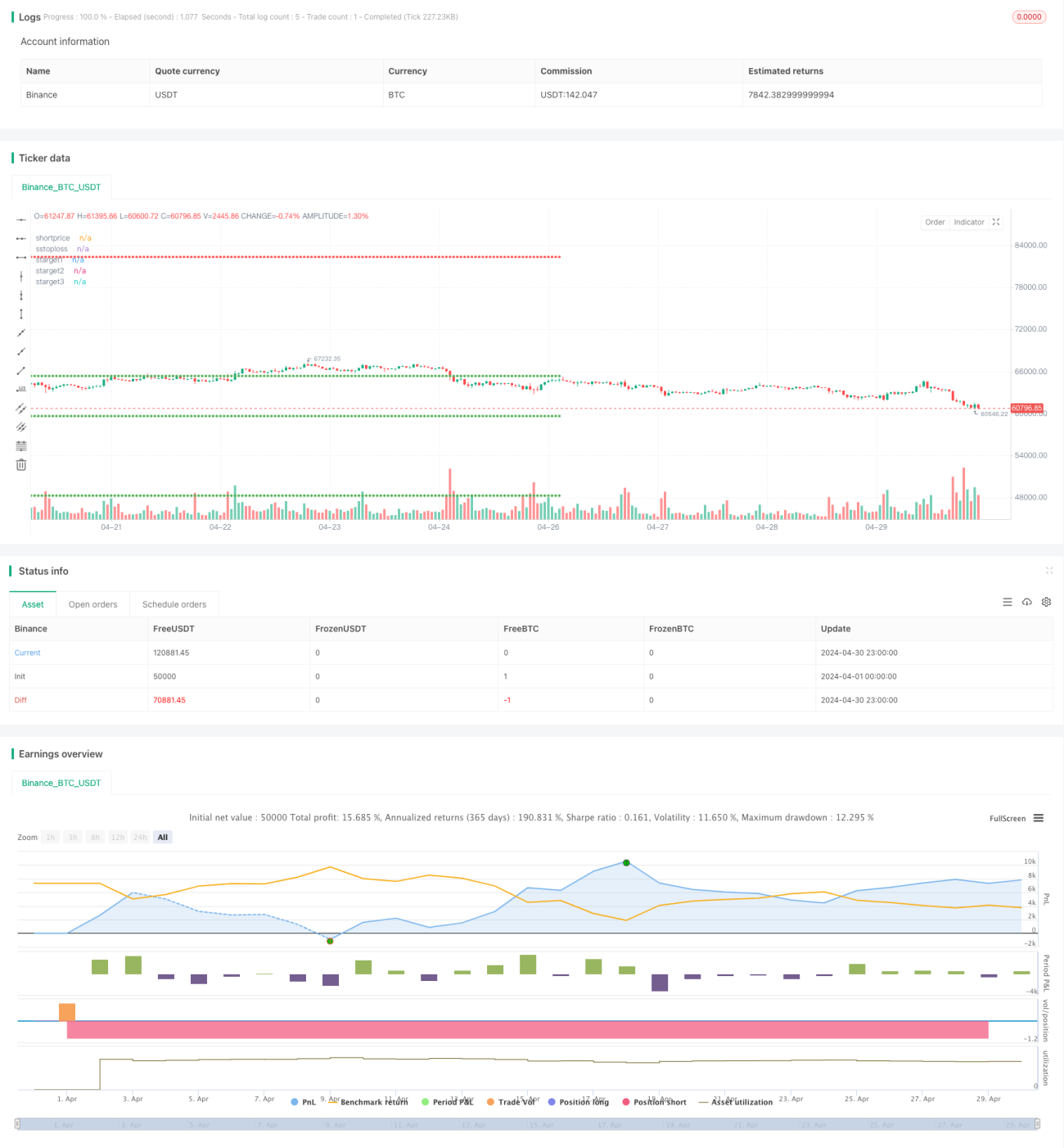

Chiến lược định lượng dựa trên PSAR và EMA

Tổng quan

Chiến lược định lượng này chủ yếu sử dụng tín hiệu giao cắt của chỉ báo Parabolic SAR (PSAR) và đường trung bình động hàm mũ (EMA), kết hợp với nhiều điều kiện tùy chỉnh để tạo ra tín hiệu mua và bán. Ý tưởng chính của chiến lược là: khi PSAR vượt lên trên EMA từ bên dưới và thỏa mãn các điều kiện nhất định thì phát sinh tín hiệu mua; khi PSAR phá vỡ xuống dưới EMA từ bên trên và thỏa mãn các điều kiện nhất định thì phát sinh tín hiệu bán. Đồng thời, chiến lược này cũng thiết lập các mức chốt lời và cắt lỗ để kiểm soát rủi ro.

Nguyên lý chiến lược

- Tính toán chỉ báo PSAR và EMA 30 chu kỳ

- Xác định mối quan hệ giao cắt giữa PSAR và EMA, đồng thời thiết lập các cờ tương ứng

- Kết hợp vị trí tương quan giữa PSAR và EMA, màu sắc của nến, v.v., xác định IGC (Ideal Green Candle) và IRC (Ideal Red Candle)

- Thông qua sự xuất hiện của IGC và IRC, xác định tín hiệu mua và bán

- Thiết lập các mức chốt lời và cắt lỗ: chốt lời lần lượt là 8%, 16% và 32% của giá mua; cắt lỗ là 16% của giá mua; đối với giá bán: chốt lời lần lượt là 8%, 16% và 32%; cắt lỗ là 16% của giá bán

- Dựa trên khung thời gian giao dịch và trạng thái vị thế, thực hiện các lệnh mua, bán hoặc đóng vị thế

Ưu điểm của chiến lược

- Kết hợp nhiều chỉ báo và điều kiện, nâng cao độ tin cậy của tín hiệu

- Thiết lập nhiều mức chốt lời và cắt lỗ, có thể linh hoạt kiểm soát rủi ro và lợi nhuận

- Đối với các điều kiện thị trường khác nhau, thiết lập các bộ lọc mua và bán, nâng cao khả năng thích ứng của chiến lược

- Mã được mô-đun hóa cao, dễ hiểu và dễ sửa đổi

Rủi ro của chiến lược

- Các tham số của chiến lược có thể không phù hợp với mọi môi trường thị trường, cần điều chỉnh theo tình hình thực tế

- Trong thị trường dao động, chiến lược này có thể phát sinh tín hiệu giao dịch thường xuyên, dẫn đến chi phí giao dịch tăng

- Chiến lược này thiếu khả năng đánh giá xu hướng thị trường, trong thị trường có xu hướng mạnh có thể bỏ lỡ cơ hội

- Việc thiết lập mức cắt lỗ có thể không hoàn toàn tránh được rủi ro từ các biến động cực đoan của thị trường

Hướng tối ưu hóa chiến lược

- Đưa vào thêm nhiều chỉ báo kỹ thuật hoặc chỉ báo tâm lý thị trường, nâng cao độ chính xác và độ tin cậy của tín hiệu

- Tối ưu hóa việc thiết lập mức chốt lời và cắt lỗ, có thể xem xét áp dụng chốt lời/cắt lỗ động hoặc dựa trên biến động (volatility)

- Đối với các trạng thái thị trường khác nhau, thiết lập các tham số và quy tắc giao dịch khác nhau, nâng cao khả năng thích ứng của chiến lược

- Thêm mô-đun quản lý vốn, dựa trên các yếu tố như tỷ lệ vốn chủ sở hữu (equity ratio balance) của tài khoản, điều chỉnh linh hoạt quy mô vị thế và mức độ rủi ro

Kết luận

Chiến lược định lượng này dựa trên các chỉ báo PSAR và EMA, thông qua nhiều điều kiện và quy tắc tùy chỉnh, tạo ra tín hiệu mua và bán. Chiến lược có tính thích ứng và linh hoạt nhất định, đồng thời cũng thiết lập các mức chốt lời và cắt lỗ để kiểm soát rủi ro. Tuy nhiên, việc thiết lập tham số và kiểm soát rủi ro của chiến lược vẫn còn không gian để tối ưu hóa. Nhìn chung, chiến lược này có thể được sử dụng như một mẫu cơ bản, thông qua tối ưu hóa và cải tiến thêm, có khả năng trở thành một chiến lược giao dịch ổn định.

- 1