Chiến lược kết hợp đơn giản: Điểm xoay Siêu xu hướng và Đường trung bình động hàm mũ kép

Tổng quan

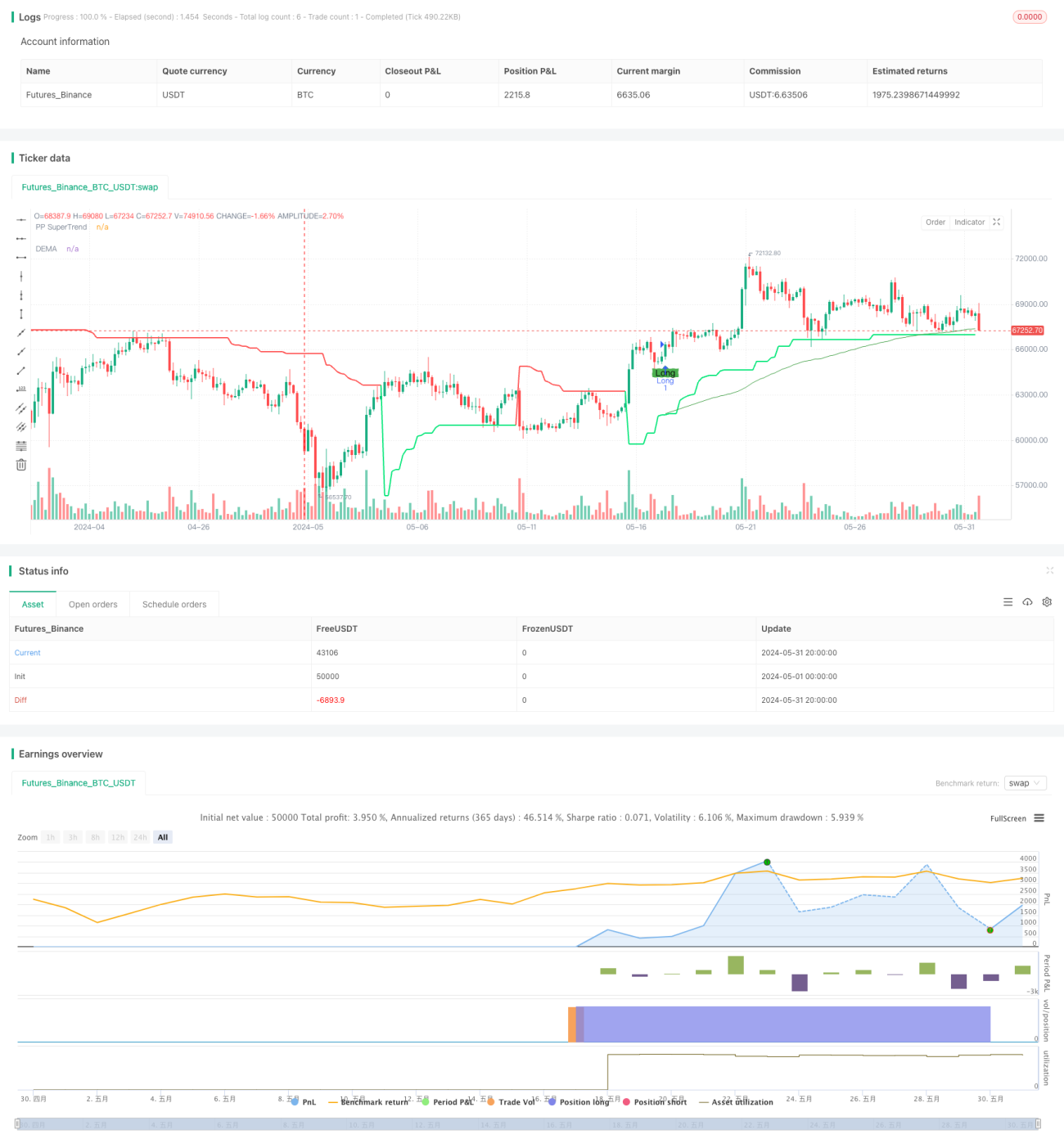

Chiến lược này kết hợp chỉ báo Pivot Point Super Trend và chỉ báo Đường trung bình động hàm mũ kép (DEMA), phân tích mối quan hệ vị trí giữa giá và hai chỉ báo này để xác định tín hiệu giao dịch. Khi giá phá vỡ chỉ báo Pivot Point Super Trend và cao hơn chỉ báo DEMA, tín hiệu mua (long) được phát sinh; khi giá phá vỡ xuống dưới chỉ báo Pivot Point Super Trend và thấp hơn chỉ báo DEMA, tín hiệu bán (short) được phát sinh. Chiến lược này có thể nắm bắt xu hướng trung và dài hạn của thị trường, đồng thời cũng có thể ứng phó với biến động giá trong ngắn hạn.

Nguyên lý chiến lược

- Tính toán chỉ báo Pivot Point Super Trend: Tính giá trị trung bình của giá cao nhất và giá thấp nhất trong một chu kỳ nhất định làm điểm trung tâm, sau đó tính dải trên và dải dưới dựa trên Dải biến động thực trung bình (ATR), tạo thành các mức hỗ trợ và kháng cự động.

- Tính toán chỉ báo DEMA: Đầu tiên tính đường trung bình động hàm mũ (EMA) của giá đóng cửa, sau đó tính EMA một lần nữa trên EMA đó, cuối cùng lấy hai lần EMA trừ đi DEMA để có chỉ báo DEMA cuối cùng.

- Phát sinh tín hiệu giao dịch: Khi giá đóng cửa phá vỡ dải trên của Pivot Point Super Trend và cao hơn chỉ báo DEMA, tín hiệu mua được phát sinh; khi giá đóng cửa phá vỡ dải dưới của Pivot Point Super Trend và thấp hơn chỉ báo DEMA, tín hiệu bán được phát sinh.

- Thiết lập cắt lỗ và chốt lời: Dựa trên giá trị pip (Pip Value) và số pip cắt lỗ (Stop Loss Pips) cũng như số pip chốt lời (Take Profit Pips) đã được thiết lập trước để tính toán giá cắt lỗ và giá chốt lời cụ thể.

Ưu điểm của chiến lược

- Khả năng bám xu hướng mạnh: Chỉ báo Pivot Point Super Trend có thể nắm bắt hiệu quả xu hướng thị trường, trong khi chỉ báo DEMA có thể loại bỏ nhiễu giá, cung cấp cơ sở đánh giá xu hướng mượt mà hơn. Sự kết hợp cả hai có thể nắm bắt chính xác xu hướng chính của thị trường.

- Khả năng thích ứng cao: Bằng cách điều chỉnh động các dải trên và dưới của chỉ báo Pivot Point Super Trend, có thể thích ứng với các điều kiện biến động thị trường khác nhau, nâng cao khả năng thích ứng của chiến lược.

- Khả năng kiểm soát rủi ro tốt: Đã thiết lập các mức cắt lỗ và chốt lời rõ ràng, có thể kiểm soát hiệu quả mức độ rủi ro của từng giao dịch, đồng thời cũng có thể kịp thời khóa lợi nhuận hiện có.

Rủi ro của chiến lược

- Rủi ro cài đặt tham số: Hiệu suất của chiến lược phụ thuộc vào cài đặt của nhiều tham số, chẳng hạn như chu kỳ Pivot Point, hệ số ATR, độ dài DEMA, v.v. Các tổ hợp tham số khác nhau có thể dẫn đến sự khác biệt lớn về hiệu suất chiến lược, cần lựa chọn và tối ưu hóa cẩn thận.

- Rủi ro thị trường dao động (sideway): Trong môi trường thị trường dao động, các tín hiệu giao dịch thường xuyên có thể dẫn đến giao dịch quá mức, làm tăng chi phí giao dịch và rủi ro trượt giá.

- Rủi ro đảo chiều xu hướng: Khi xu hướng thị trường đảo chiều, chiến lược có thể gặp thua lỗ liên tiếp, cần kết hợp với các phương pháp phân tích khác để điều chỉnh chiến lược kịp thời.

Hướng tối ưu hóa chiến lược

- Tối ưu hóa tham số: Thông qua kiểm tra tối ưu hóa tham số trên các khung thời gian và sản phẩm giao dịch khác nhau, tìm ra tổ hợp tham số tốt nhất, nâng cao tính ổn định và khả năng sinh lời của chiến lược.

- Lọc tín hiệu: Khi tín hiệu giao dịch phát sinh, có thể kết hợp với các chỉ báo kỹ thuật khác hoặc đặc điểm hành vi giá để xác nhận lần thứ hai, nâng cao độ tin cậy của tín hiệu, giảm thiểu tổn thất do tín hiệu giả.

- Quản lý vị thế: Dựa trên tình hình biến động thị trường và khả năng chịu rủi ro của tài khoản, điều chỉnh linh hoạt quy mô vị thế của từng giao dịch, kiểm soát tổng mức độ rủi ro.

- Tối ưu hóa kết hợp: Kết hợp chiến lược này với các chiến lược hoặc hệ thống giao dịch khác, thông qua việc phân tán rủi ro và tăng cường tính ổn định, nâng cao hiệu suất dài hạn của chiến lược.

Tổng kết

Chiến lược này, thông qua sự kết hợp giữa chỉ báo Pivot Point Super Trend và chỉ báo DEMA, có thể nắm bắt tốt xu hướng thị trường, đồng thời cũng có thể ứng phó với biến động ngắn hạn. Chiến lược có các ưu điểm như khả năng bám xu hướng mạnh, khả năng thích ứng cao, khả năng kiểm soát rủi ro tốt, nhưng cũng phải đối mặt với các rủi ro về cài đặt tham số, thị trường dao động và đảo chiều xu hướng. Thông qua các biện pháp như tối ưu hóa tham số, lọc tín hiệu, quản lý vị thế và tối ưu hóa kết hợp, có thể nâng cao hơn nữa tính ổn định và khả năng sinh lời của chiến lược, thích ứng tốt hơn với các môi trường thị trường khác nhau.

- 1