Chiến lược hồi quy trung bình

Tổng quan

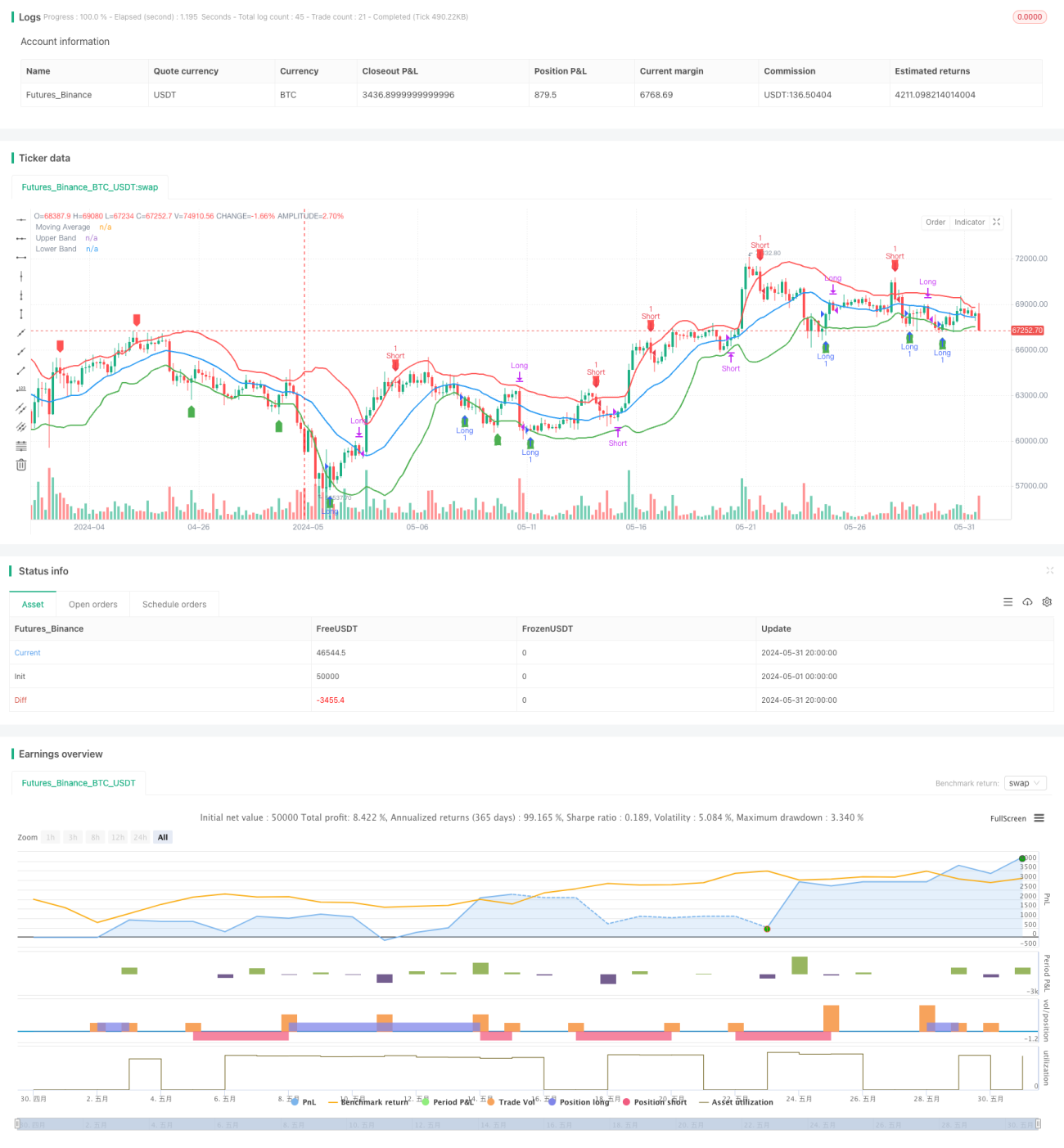

Chiến lược này dựa trên nguyên lý hồi quy trung bình, sử dụng độ lệch giá so với đường trung bình động để đưa ra quyết định giao dịch. Khi giá vượt lên trên dải trên, chiến lược bán khống; khi giá vượt xuống dưới dải dưới, chiến lược mua dài hạn; khi giá quay trở lại đường trung bình động, đóng vị thế. Cốt lõi của chiến lược này là giả định rằng giá luôn có xu hướng hồi quy về mức trung bình.

Nguyên lý chiến lược

- Tính đường trung bình động đơn giản (SMA) với chu kỳ xác định (mặc định 20) làm mức trung bình của giá.

- Tính độ lệch chuẩn (DEV) của giá, từ đó xây dựng dải trên và dải dưới. Dải trên là SMA cộng với bội số của độ lệch chuẩn (mặc định 1.5), dải dưới là SMA trừ đi bội số của độ lệch chuẩn.

- Khi giá phá vỡ lên trên dải trên, bán khống; khi giá phá vỡ xuống dưới dải dưới, mua dài hạn.

- Khi giá mua dài hạn cắt xuống dưới SMA, đóng vị thế mua; khi giá bán khống cắt lên trên SMA, đóng vị thế bán.

- Đánh dấu trên biểu đồ đường trung bình động, dải trên, dải dưới cũng như tín hiệu mua/bán.

Phân tích ưu điểm

- Chiến lược hồi quy trung bình dựa trên nguyên lý thống kê rằng giá luôn hồi quy về giá trị trung bình, về dài hạn có xác suất sinh lời nhất định.

- Việc thiết lập dải trên và dải dưới cung cấp điểm vào và ra rõ ràng, dễ thực hiện và quản lý.

- Logic chiến lược đơn giản, dễ hiểu và dễ triển khai.

- Phù hợp với các sản phẩm và khung thời gian có đặc tính hồi quy trung bình rõ rệt.

Phân tích rủi ro

- Khi xu hướng thị trường thay đổi, giá có thể lệch xa khỏi giá trị trung bình trong thời gian dài mà không hồi quy, dẫn đến chiến lược mất hiệu lực.

- Việc đặt bội số độ lệch chuẩn không phù hợp có thể khiến tần suất giao dịch quá cao hoặc quá thấp, ảnh hưởng đến lợi nhuận.

- Trong điều kiện thị trường cực đoan, biến động giá mạnh có thể khiến dải trên và dải dưới mất tác dụng.

- Nếu sản phẩm hoặc khung thời gian không có đặc tính hồi quy trung bình, chiến lược có thể không sinh lời.

Hướng tối ưu

- Tiến hành kiểm tra tối ưu hóa chu kỳ SMA và bội số độ lệch chuẩn để tìm tham số tốt nhất.

- Đưa vào chỉ báo xác định xu hướng, tránh giao dịch ngược xu hướng khi xu hướng rõ ràng.

- Ngoài độ lệch chuẩn, thêm các chỉ báo biến động như ATR để xây dựng dải động.

- Xem xét các chi phí giao dịch như trượt giá, phí giao dịch để đảm bảo tính thực tế của backtest.

- Thêm mô-đun quản lý rủi ro như stop loss, take profit, quản lý vị thế, v.v.

Tổng kết

Chiến lược hồi quy trung bình là một chiến lược giao dịch định lượng dựa trên nguyên lý thống kê, đưa ra quyết định giao dịch bằng cách xây dựng dải trên và dải dưới xung quanh giá trung bình. Chiến lược này có logic đơn giản, thực hiện rõ ràng, nhưng cần chú ý đến việc lựa chọn sản phẩm và tối ưu hóa tham số. Trong ứng dụng thực tế, cũng cần xem xét các yếu tố như xu hướng, chi phí giao dịch, kiểm soát rủi ro để nâng cao tính ổn định và khả năng sinh lời của chiến lược. Tóm lại, chiến lược hồi quy trung bình là một chiến lược phổ biến trong lĩnh vực giao dịch định lượng và đáng được nghiên cứu sâu.

- 1