Chiến lược đột phá động lượng thích ứng động

Tổng quan

Chiến lược đột phá động lượng thích ứng động là một chiến lược giao dịch định lượng cao cấp sử dụng chỉ báo động lượng thích ứng và nhận dạng mô hình nến. Chiến lược này điều chỉnh linh hoạt chu kỳ động lượng để thích ứng với biến động thị trường, kết hợp nhiều bộ lọc để xác định các cơ hội đột phá xu hướng có xác suất cao. Cốt lõi của chiến lược là nắm bắt sự thay đổi của động lượng thị trường, đồng thời sử dụng mô hình nhấn chìm làm tín hiệu vào lệnh nhằm nâng cao độ chính xác và khả năng sinh lời của giao dịch.

Nguyên lý chiến lược

-

Điều chỉnh chu kỳ động:

- Chiến lược sử dụng chỉ báo động lượng thích ứng, điều chỉnh linh hoạt chu kỳ tính toán dựa trên biến động thị trường.

- Trong thời kỳ biến động cao, chu kỳ rút ngắn để phản ứng nhanh với thay đổi thị trường; trong thời kỳ biến động thấp, chu kỳ kéo dài để tránh giao dịch quá mức.

- Phạm vi chu kỳ được đặt từ 10 đến 40, xác định trạng thái biến động thông qua chỉ báo ATR.

-

Tính toán và làm mịn động lượng:

- Sử dụng chu kỳ động để tính chỉ báo động lượng.

- Có thể lựa chọn có làm mịn EMA cho động lượng hay không, mặc định sử dụng EMA 7 chu kỳ.

-

Xác định hướng xu hướng:

- Xác định hướng xu hướng bằng cách tính độ dốc động lượng (chênh lệch giữa giá trị hiện tại và giá trị trước đó).

- Độ dốc dương biểu thị xu hướng tăng, độ dốc âm biểu thị xu hướng giảm.

-

Nhận dạng mô hình nhấn chìm:

- Sử dụng hàm tùy chỉnh để nhận dạng mô hình nhấn chìm tăng và giảm.

- Xem xét mối quan hệ giữa giá mở cửa và giá đóng cửa của nến hiện tại và nến trước đó.

- Đưa vào bộ lọc kích thước thân nến tối thiểu để nâng cao độ tin cậy của mô hình.

-

Tạo tín hiệu giao dịch:

- Tín hiệu Long: Mô hình nhấn chìm tăng + Độ dốc động lượng dương.

- Tín hiệu Short: Mô hình nhấn chìm giảm + Độ dốc động lượng âm.

-

Quản lý giao dịch:

- Vào lệnh khi nến tiếp theo mở cửa sau khi tín hiệu được xác nhận.

- Tự động đóng vị thế sau chu kỳ nắm giữ cố định (mặc định 3 nến).

Lợi thế của chiến lược

-

Khả năng thích ứng cao:

- Điều chỉnh linh hoạt chu kỳ động lượng, thích ứng với các môi trường thị trường khác nhau.

- Phản ứng nhanh trong thời kỳ biến động cao, tránh giao dịch quá mức trong thời kỳ biến động thấp.

-

Cơ chế xác nhận nhiều lớp:

- Kết hợp chỉ báo kỹ thuật (động lượng) và mô hình giá (nhấn chìm), nâng cao độ tin cậy của tín hiệu.

- Sử dụng bộ lọc độ dốc và kích thước thân nến, giảm tín hiệu nhiễu.

-

Thời điểm vào lệnh chính xác:

- Tận dụng mô hình nhấn chìm để bắt kịp các điểm đảo chiều xu hướng tiềm năng.

- Kết hợp với độ dốc động lượng, đảm bảo tham gia vào xu hướng mới nổi.

-

Quản lý rủi ro hợp lý:

- Chu kỳ nắm giữ cố định, tránh nắm giữ quá lâu dẫn đến sụt giảm.

- Bộ lọc kích thước thân nến, giảm sai sót do biến động nhỏ.

-

Linh hoạt và có thể tùy chỉnh:

- Nhiều tham số có thể điều chỉnh, dễ dàng tối ưu hóa cho các thị trường và khung thời gian khác nhau.

- Chức năng làm mịn EMA tùy chọn, cân bằng giữa độ nhạy và độ ổn định.

Rủi ro của chiến lược

-

Rủi ro đột phá giả:

- Có thể tạo ra nhiều tín hiệu đột phá giả trong thị trường đi ngang.

- Cách giảm thiểu: Thêm các chỉ báo xác nhận xu hướng bổ sung, như giao cắt đường trung bình động.

-

Vấn đề độ trễ:

- Sử dụng EMA làm mịn có thể gây ra độ trễ tín hiệu, bỏ lỡ điểm vào lệnh tối ưu.

- Cách giảm thiểu: Điều chỉnh chu kỳ EMA hoặc xem xét sử dụng phương pháp làm mịn nhạy hơn.

-

Hạn chế của cơ chế thoát lệnh cố định:

- Thoát lệnh theo chu kỳ cố định có thể kết thúc sớm xu hướng có lợi hoặc kéo dài thua lỗ.

- Cách giảm thiểu: Giới thiệu chốt lời và cắt lỗ động, như trailing stop hoặc thoát lệnh dựa trên biến động.

-

Phụ thuộc quá mức vào một khung thời gian:

- Chiến lược có thể bỏ qua xu hướng tổng thể của khung thời gian lớn hơn.

- Cách giảm thiểu: Đưa vào phân tích đa khung thời gian, đảm bảo hướng giao dịch phù hợp với xu hướng lớn hơn.

-

Nhạy cảm với tham số:

- Quá nhiều tham số có thể điều chỉnh có thể dẫn đến overfitting dữ liệu lịch sử.

- Cách giảm thiểu: Sử dụng tối ưu hóa từng bước và kiểm tra cross-sample để xác nhận độ ổn định của tham số.

Hướng tối ưu hóa chiến lược

-

Tích hợp đa khung thời gian:

- Đưa vào xác định xu hướng của khung thời gian lớn hơn, chỉ giao dịch theo hướng xu hướng chính.

- Lý do: Nâng cao tỷ lệ thành công tổng thể của giao dịch, tránh giao dịch ngược xu hướng lớn.

-

Chốt lời và cắt lỗ động:

- Thực hiện cắt lỗ động dựa trên ATR hoặc thay đổi động lượng.

- Sử dụng trailing stop để tối đa hóa lợi nhuận xu hướng.

- Lý do: Thích ứng với biến động thị trường, bảo vệ lợi nhuận, giảm sụt giảm.

-

Phân tích volume profile:

- Tích hợp volume profile, xác định các ngưỡng hỗ trợ và kháng cự chính.

- Lý do: Nâng cao độ chính xác của điểm vào lệnh, tránh giao dịch ở các vị trí đột phá không hiệu quả.

-

Tối ưu hóa bằng machine learning:

- Sử dụng thuật toán machine learning để điều chỉnh tham số động.

- Lý do: Đạt được khả năng thích ứng liên tục cho chiến lược, nâng cao độ ổn định dài hạn.

-

Tích hợp chỉ báo tâm lý:

- Đưa vào các chỉ báo tâm lý thị trường, như VIX hoặc biến động ngụ ý từ quyền chọn.

- Lý do: Điều chỉnh hành vi chiến lược khi tâm lý cực đoan, tránh giao dịch quá mức.

-

Phân tích tương quan:

- Xem xét sự di chuyển đồng bộ của nhiều tài sản liên quan.

- Lý do: Nâng cao độ tin cậy của tín hiệu, xác định xu hướng thị trường mạnh hơn.

Tổng kết

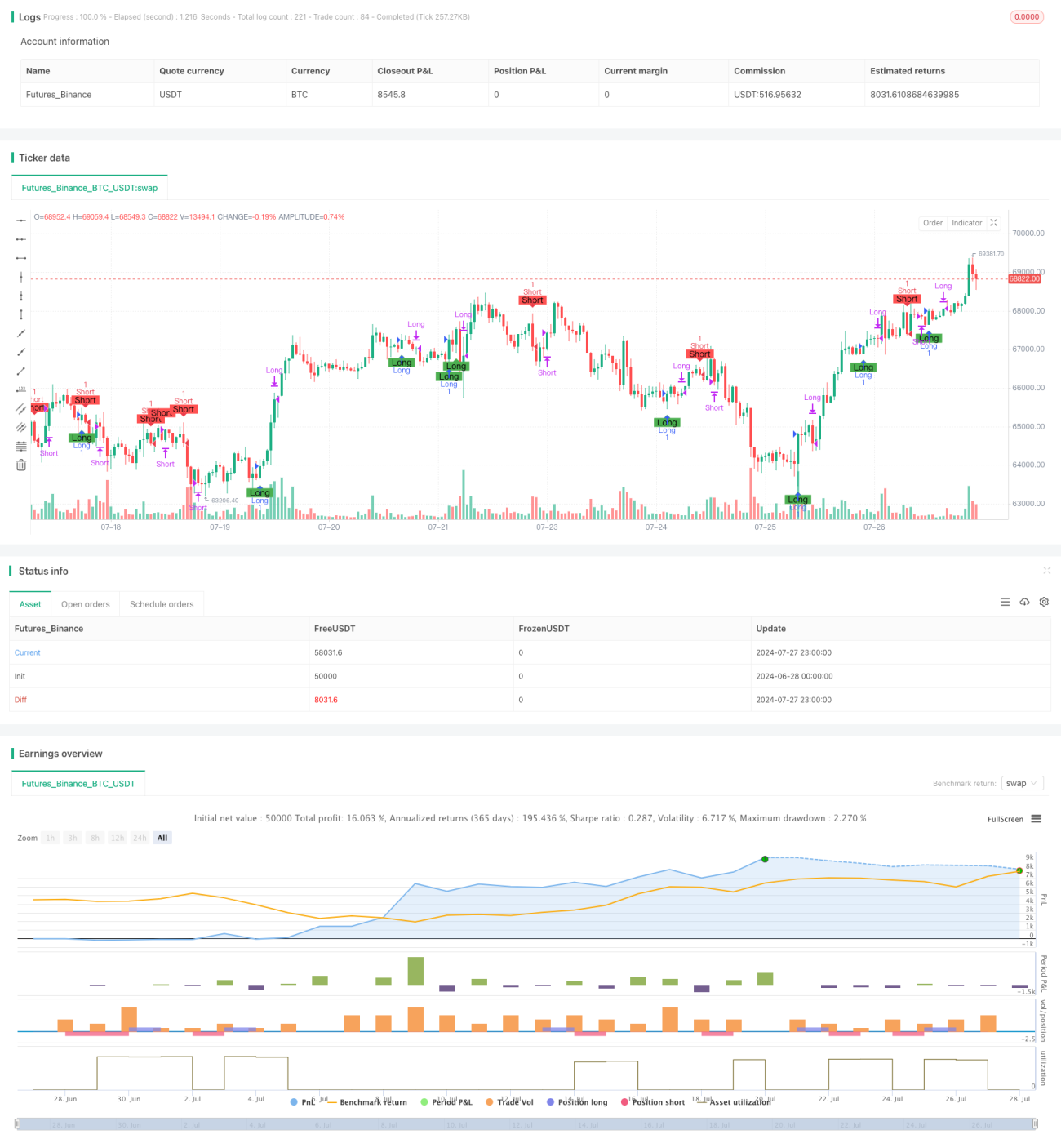

Chiến lược đột phá động lượng thích ứng động là một hệ thống giao dịch cao cấp kết hợp phân tích kỹ thuật và phương pháp định lượng. Bằng cách điều chỉnh linh hoạt chu kỳ động lượng, nhận dạng mô hình nhấn chìm và kết hợp nhiều bộ lọc, chiến lược này có thể thích ứng tự động để bắt kịp các cơ hội đột phá xu hướng có xác suất cao trong các môi trường thị trường khác nhau. Mặc dù tồn tại một số rủi ro cố hữu như đột phá giả và nhạy cảm với tham số, nhưng thông qua các hướng tối ưu hóa được đề xuất như phân tích đa khung thời gian, quản lý rủi ro động và ứng dụng machine learning, chiến lược có tiềm năng nâng cao hơn nữa độ ổn định và khả năng sinh lời. Nhìn chung, đây là một chiến lược định lượng có tư duy rõ ràng và logic chặt chẽ, cung cấp cho nhà giao dịch một công cụ mạnh mẽ để nắm bắt động lượng thị trường và sự thay đổi xu hướng.

/*backtest

start: 2024-06-28 00:00:00

end: 2024-07-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ironperol

//@version=5

strategy("Adaptive Momentum Strategy", overlay=true, margin_long=100, margin_short=100)- 1