Chiến lược nắm giữ qua đêm theo xu hướng tăng giảm đa thị trường dựa trên chỉ báo EMA

Chiến lược này là một chiến lược giao dịch qua đêm dựa trên chỉ báo kỹ thuật EMA, nhằm nắm bắt các cơ hội giao dịch trước khi thị trường đóng cửa và sau khi mở cửa. Thông qua kiểm soát thời gian chính xác và bộ lọc chỉ báo kỹ thuật, chiến lược thực hiện giao dịch thông minh trong các môi trường thị trường khác nhau.

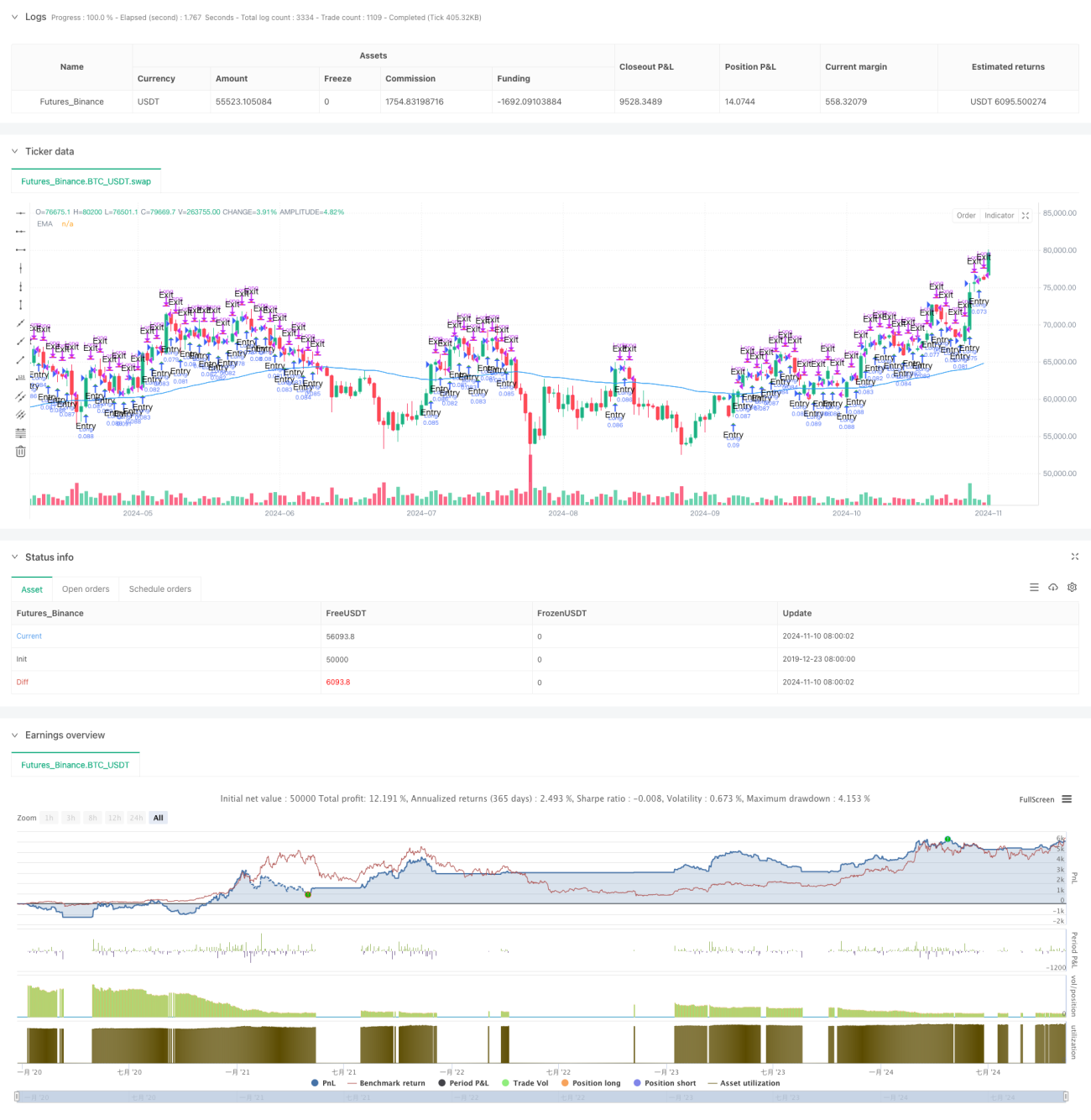

Tổng quan chiến lược

Chiến lược chủ yếu thu lợi nhuận bằng cách vào lệnh tại thời điểm cụ thể trước khi thị trường đóng cửa và thoát lệnh tại thời điểm cụ thể sau khi mở cửa phiên tiếp theo. Kết hợp chỉ báo EMA làm xác nhận xu hướng, tìm kiếm cơ hội giao dịch trên nhiều thị trường toàn cầu. Chiến lược cũng tích hợp chức năng giao dịch tự động, cho phép vận hành không cần giám sát.

Nguyên lý chiến lược

- Kiểm soát thời gian: Dựa trên thời gian giao dịch của từng thị trường, vào lệnh cố định trước khi đóng cửa và thoát lệnh cố định sau khi mở cửa.

- Bộ lọc EMA: Sử dụng chỉ báo EMA tùy chọn để xác nhận tín hiệu vào lệnh.

- Lựa chọn thị trường: Hỗ trợ thích ứng thời gian giao dịch của ba thị trường lớn: Mỹ, châu Á, châu Âu.

- Bảo vệ cuối tuần: Buộc đóng vị thế trước khi đóng cửa phiên thứ Sáu, tránh rủi ro nắm giữ qua cuối tuần.

Ưu điểm chiến lược

- Thích ứng đa thị trường: Có thể linh hoạt điều chỉnh thời gian giao dịch theo đặc điểm của từng thị trường.

- Kiểm soát rủi ro toàn diện: Bao gồm cơ chế bảo vệ đóng vị thế cuối tuần.

- Mức độ tự động hóa cao: Hỗ trợ kết nối giao diện giao dịch tự động.

- Tham số linh hoạt có thể điều chỉnh: Thời gian giao dịch và tham số chỉ báo kỹ thuật đều có thể tùy chỉnh.

- Xem xét chi phí giao dịch: Bao gồm thiết lập phí hoa hồng và trượt giá.

Rủi ro chiến lược

- Rủi ro biến động thị trường: Nắm giữ qua đêm có thể đối mặt với rủi ro gap.

- Phụ thuộc vào thời gian: Hiệu quả chiến lược bị ảnh hưởng bởi lựa chọn khung thời gian thị trường.

- Hạn chế của chỉ báo kỹ thuật: Chỉ báo EMA đơn lẻ có thể xuất hiện độ trễ.

Khuyến nghị: Đặt stop loss, bổ sung thêm xác nhận từ nhiều chỉ báo kỹ thuật.

Hướng tối ưu hóa chiến lược

- Bổ sung thêm tổ hợp nhiều chỉ báo kỹ thuật.

- Đưa vào cơ chế lọc biến động.

- Tối ưu hóa lựa chọn thời gian vào và thoát lệnh.

- Thêm chức năng điều chỉnh tham số thích ứng.

- Tăng cường module kiểm soát rủi ro.

Tổng kết

Chiến lược này, thông qua kiểm soát thời gian chính xác và bộ lọc chỉ báo kỹ thuật, đã xây dựng một hệ thống giao dịch qua đêm đáng tin cậy. Thiết kế chiến lược đã xem xét toàn diện các nhu cầu thực chiến, bao gồm các yếu tố như thích ứng đa thị trường, kiểm soát rủi ro, giao dịch tự động, mang lại giá trị thực tiễn cao. Thông qua việc liên tục tối ưu và hoàn thiện, chiến lược này có tiềm năng đạt được lợi nhuận ổn định trong giao dịch thực tế.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-11 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// This strategy, titled "Overnight Market Entry Strategy with EMA Filter," is designed for entering long positions shortly before - 1