Chiến lược giao dịch thông minh RSI với dừng lỗ động

Tổng quan

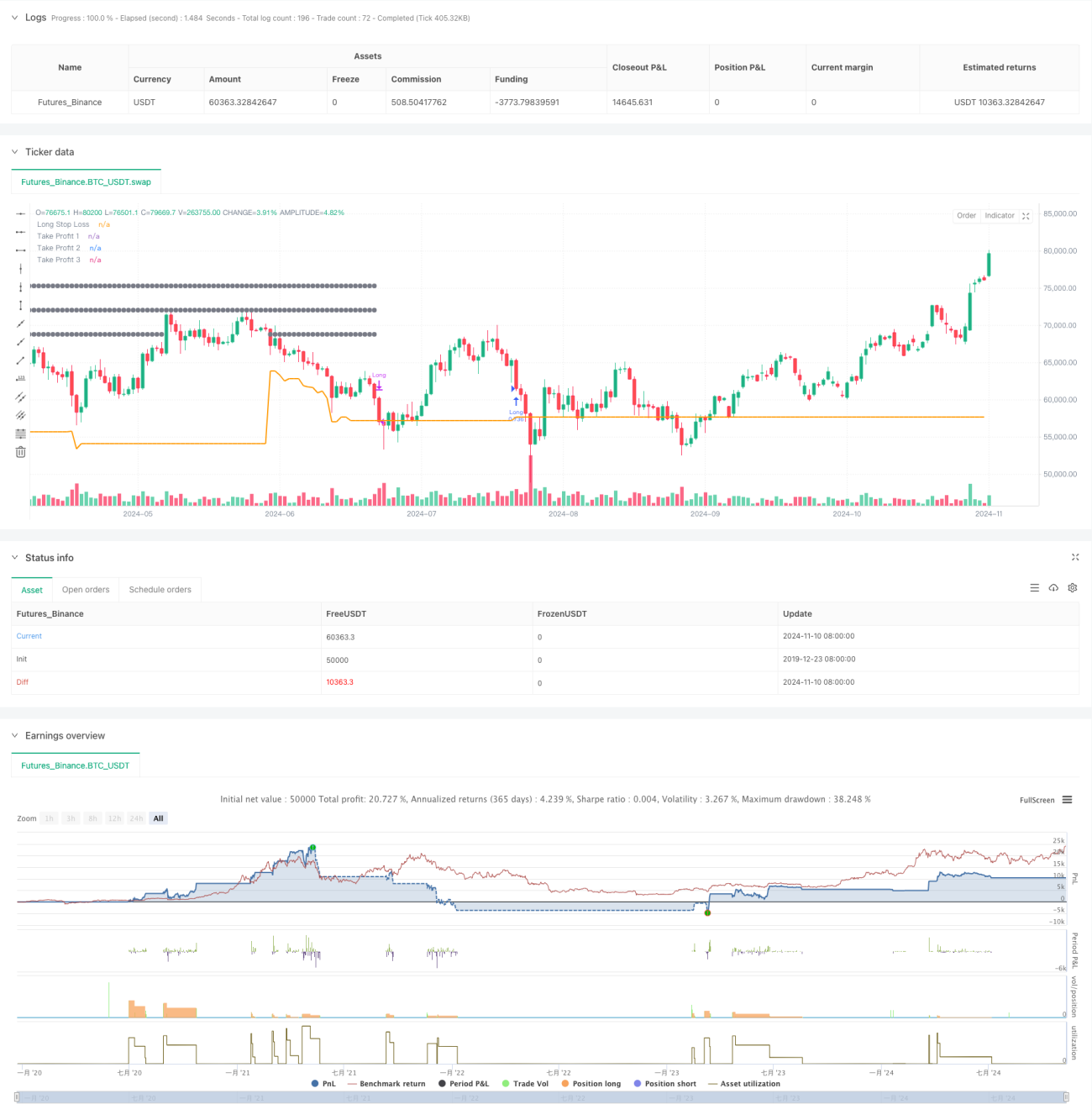

Chiến lược này là một hệ thống giao dịch cắt lỗ động dựa trên chỉ báo RSI, kết hợp với đường trung bình SMA và chỉ báo biên độ ATR để tối ưu hóa các quyết định giao dịch. Chiến lược sử dụng kế hoạch chốt lời đa cấp, thông qua phương pháp đóng vị thế theo dạng kim tự tháp để tối đa hóa lợi nhuận, đồng thời áp dụng cắt lỗ động dựa trên ATR để kiểm soát rủi ro. Chiến lược có khả năng thích ứng cao, có thể tự động điều chỉnh các tham số giao dịch theo điều kiện biến động của thị trường.

Nguyên lý chiến lược

Chiến lược chủ yếu dựa vào vùng quá bán của RSI (RSI < 30) làm tín hiệu mở vị thế, đồng thời yêu cầu giá nằm trên đường trung bình động 200 kỳ để đảm bảo xu hướng tăng. Hệ thống sử dụng ba mục tiêu chốt lời (5%, 10%, 15%) kết hợp với cắt lỗ động dựa trên ATR. Cụ thể:

- Điều kiện vào lệnh: RSI dưới 30 và giá nằm trên SMA200

- Quản lý vị thế: Sử dụng 75% vốn cho một lần mở vị thế

- Thiết lập cắt lỗ: Cắt lỗ động dựa trên 1.5 lần giá trị ATR

- Chiến lược chốt lời: Thiết lập ba mức chốt lời lần lượt tại 5%, 10%, 15%, đóng vị thế theo tỷ lệ 33%, 66%, 100% tương ứng

Ưu điểm chiến lược

- Quản lý rủi ro động: Thích ứng với biến động thị trường thông qua ATR

- Chốt lời theo từng phần: Giảm nhiễu tâm lý, tăng xác suất có lợi nhuận

- Xác nhận xu hướng: Sử dụng đường trung bình để lọc tín hiệu nhiễu

- Quản lý vốn: Kiểm soát vị thế theo tỷ lệ phần trăm, phù hợp với quy mô tài khoản khác nhau

- Tối ưu hoa hồng: Tính đến chi phí giao dịch, gần với giao dịch thực tế hơn

Rủi ro chiến lược

- Độ trễ của đường trung bình có thể dẫn đến chậm vào lệnh

- RSI quá bán không nhất thiết đại diện cho sự đảo chiều

- Vị thế với tỷ lệ lớn có thể gây ra drawdown đáng kể

- Chốt lời từng phần thường xuyên có thể làm tăng chi phí giao dịch

Đề xuất quản lý các rủi ro này bằng cách điều chỉnh tham số và thêm bộ lọc.

Hướng tối ưu hóa chiến lược

- Thêm tín hiệu xác nhận khối lượng giao dịch

- Đưa vào chỉ báo sức mạnh xu hướng

- Tối ưu hóa phân bổ tỷ lệ chốt lời

- Thêm bộ lọc chu kỳ thời gian

- Cân nhắc bổ sung quản lý vị thế thích ứng với biến động

Kết luận

Chiến lược này xây dựng một hệ thống giao dịch tương đối hoàn chỉnh thông qua việc kết hợp các chỉ báo kỹ thuật và quản lý rủi ro động. Ưu điểm của nó là khả năng thích ứng cao, rủi ro có thể kiểm soát, tuy nhiên vẫn cần tối ưu hóa tham số dựa trên điều kiện thị trường thực tế. Chiến lược phù hợp với nhà đầu tư trung và dài hạn, có thể được sử dụng như một điểm khởi đầu tốt cho giao dịch hệ thống.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-11 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA/4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © wielkieef

//@version=5- 1