Chiến lược điều chỉnh vị thế thích ứng động đa chỉ báo dựa trên độ biến động ATR

Tổng quan

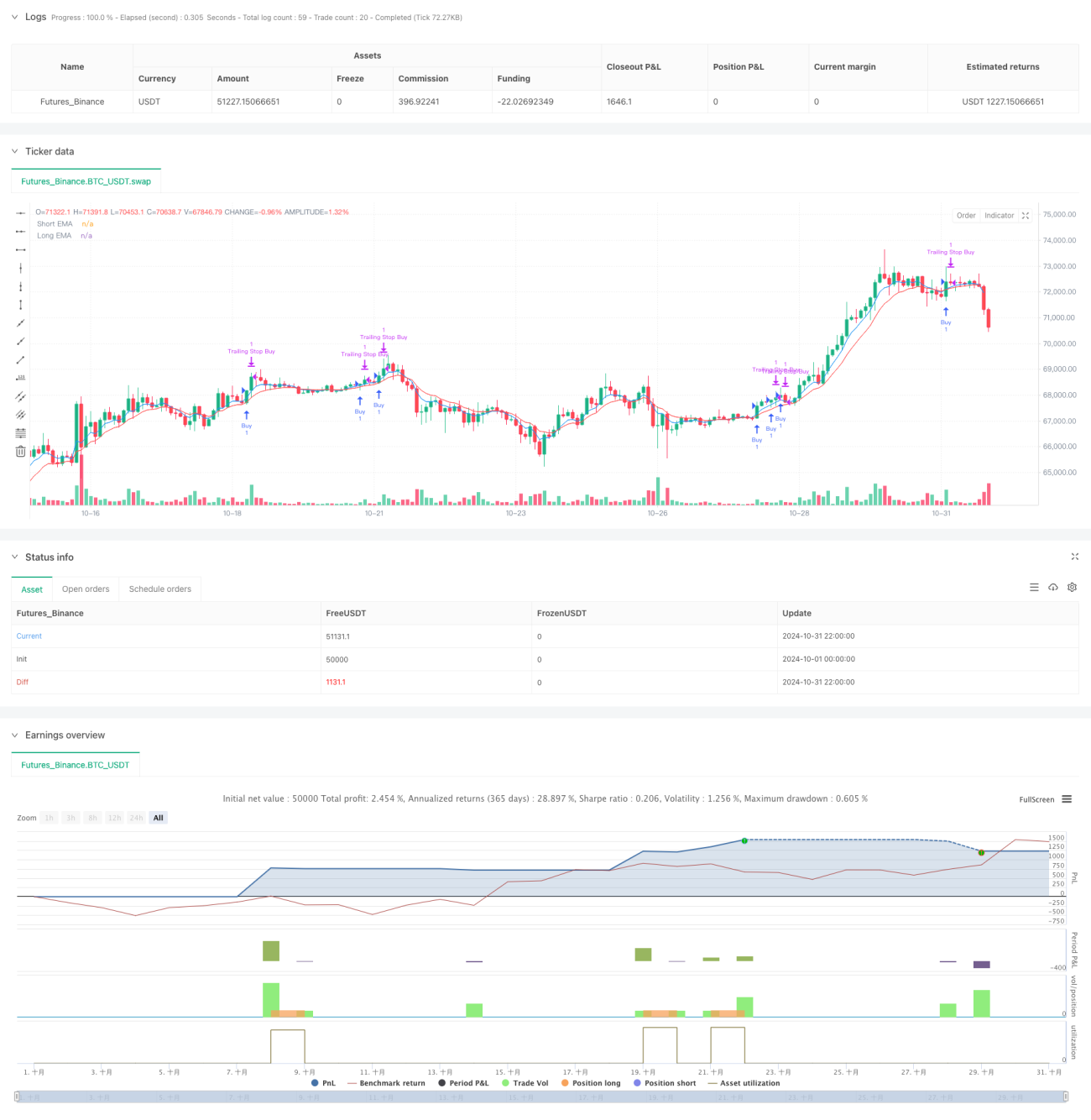

Chiến lược này là một chiến lược giao dịch định lượng dựa trên nhiều chỉ báo kỹ thuật và quản lý rủi ro động. Nó kết hợp nhiều chiều như theo dõi xu hướng EMA, biến động ATR, quá mua/quá bán RSI và nhận dạng mô hình nến, thông qua việc điều chỉnh vị thế thích ứng và cắt lỗ động để cân bằng lợi nhuận và rủi ro. Chiến lược sử dụng chốt lời theo từng phần và cắt lỗ di động để bảo vệ lợi nhuận.

Nguyên lý chiến lược

Chiến lược chủ yếu thực hiện giao dịch thông qua các khía cạnh sau:

- Sử dụng giao cắt của đường EMA 5 kỳ và 10 kỳ để xác định hướng xu hướng

- Sử dụng chỉ báo RSI để xác định vùng quá mua/quá bán, tránh mua đuổi bán đáy

- Sử dụng chỉ báo ATR để điều chỉnh động vị trí cắt lỗ và kích thước vị thế

- Kết hợp với các mô hình nến (nhấn chìm, búa, sao băng) làm tín hiệu hỗ trợ vào lệnh

- Áp dụng cơ chế bù trượt giá động dựa trên ATR

- Lọc tín hiệu giả thông qua xác nhận khối lượng giao dịch

Lợi thế của chiến lược

- Xác nhận chéo nhiều tín hiệu, tăng độ tin cậy giao dịch

- Quản lý rủi ro động, tự động điều chỉnh theo biến động thị trường

- Chiến lược chốt lời theo từng phần, hợp lý khóa một phần lợi nhuận

- Sử dụng cắt lỗ di động, bảo vệ lợi nhuận đã có

- Đặt giới hạn cắt lỗ hàng ngày, kiểm soát mức độ rủi ro

- Bù trượt giá động, tăng tỷ lệ khớp lệnh

Rủi ro của chiến lược

- Nhiều chỉ báo có thể dẫn đến tín hiệu chậm trễ

- Giao dịch thường xuyên có thể tạo ra chi phí cao

- Trong thị trường dao động có thể bị cắt lỗ thường xuyên

- Nhận dạng mô hình nến có yếu tố chủ quan

- Tối ưu hóa tham số có thể dẫn đến quá khớp dữ liệu

Hướng tối ưu hóa chiến lược

- Đưa vào đánh giá chu kỳ biến động thị trường, điều chỉnh tham số động

- Thêm bộ lọc cường độ xu hướng, giảm tín hiệu giả

- Tối ưu hóa thuật toán quản lý vị thế, nâng cao hiệu quả sử dụng vốn

- Bổ sung thêm các chỉ báo tâm lý thị trường

- Phát triển hệ thống tối ưu hóa tham số thích ứng

Tổng kết

Đây là một hệ thống chiến lược hoàn chỉnh kết hợp nhiều chỉ báo kỹ thuật, thông qua quản lý rủi ro động và xác nhận tín hiệu đa lớp để nâng cao tính ổn định giao dịch. Lợi thế cốt lõi của chiến lược nằm ở khả năng thích ứng và hệ thống kiểm soát rủi ro hoàn thiện, nhưng vẫn cần được kiểm chứng đầy đủ và tối ưu hóa liên tục trong giao dịch thực tế.

- 1