Tổng quan

Chiến lược này là một hệ thống giao dịch mở cửa thị trường dựa trên nhiều chỉ báo kỹ thuật, tập trung vào phiên giao dịch mở cửa của thị trường Đức và Mỹ. Chiến lược sử dụng Bollinger Bands để xác định giai đoạn tích lũy, kết hợp đường trung bình động hàm mũ ngắn hạn và dài hạn để xác nhận xu hướng, sử dụng chỉ báo sức mạnh tương đối và chỉ báo hướng xu hướng để lọc tín hiệu giao dịch, cuối cùng áp dụng chỉ báo true range trung bình để quản lý vị thế một cách linh hoạt.

Nguyên lý chiến lược

Chiến lược sử dụng Bollinger Bands 14 chu kỳ (độ lệch chuẩn 1,5 lần) để xác định các giai đoạn biến động thấp, khi giá tiến gần đến dải giữa của Bollinger Bands được coi là tích lũy. Đồng thời sử dụng đường trung bình động hàm mũ 10 chu kỳ và 200 chu kỳ để xác nhận xu hướng tăng, yêu cầu giá nằm trên cả hai đường trung bình. Sử dụng RSI 7 chu kỳ để đảm bảo thị trường không bị quá bán (>30), ADX 7 chu kỳ để xác nhận sức mạnh xu hướng (>10). Chiến lược còn phân tích các đỉnh của 20 nến gần nhất để tìm vùng kháng cự, yêu cầu ít nhất hai lần chạm. Khi phá vỡ vùng kháng cự này và đáp ứng các điều kiện khác sẽ vào lệnh, sử dụng dừng lỗ 2 lần ATR và chốt lời 4 lần ATR.

Ưu điểm chiến lược

- Nhiều chỉ báo kỹ thuật xác nhận chéo, giảm hiệu quả các tín hiệu nhiễu

- Sử dụng dừng lỗ và chốt lời động dựa trên ATR, thích nghi với biến động thị trường

- Tập trung vào cơ hội biến động cao trong phiên mở cửa

- Nắm bắt xu hướng mạnh thông qua mô hình tích lũy – phá vỡ

- Cơ chế quản lý rủi ro hoàn chỉnh

Rủi ro chiến lược

- Nhiều chỉ báo có thể dẫn đến bỏ lỡ một số cơ hội giao dịch

- Biến động mạnh trong phiên mở cửa có thể kích hoạt dừng lỗ

- Đảo chiều nhanh của thị trường có thể gây ra tổn thất lớn

Khuyến nghị sử dụng quản lý vị thế hợp lý, thực hiện nghiêm ngặt chiến lược dừng lỗ, tránh giao dịch quá mức.

Hướng tối ưu hóa chiến lược

- Có thể điều chỉnh các tham số chỉ báo tùy theo đặc điểm thị trường khác nhau

- Cân nhắc thêm chỉ báo khối lượng để xác nhận tính hiệu quả của phá vỡ

- Đưa vào nhiều chỉ báo kỹ thuật hơn để tăng độ tin cậy của tín hiệu

- Tối ưu hóa thời điểm vào lệnh, giảm tác động của trượt giá

- Hoàn thiện cơ chế chốt lời và dừng lỗ, nâng cao tỷ lệ lợi nhuận/rủi ro

Tổng kết

Chiến lược này sử dụng phương pháp phân tích kỹ thuật đa chiều để nắm bắt cơ hội giao dịch trong phiên mở cửa, áp dụng quản lý rủi ro động với dừng lỗ và chốt lời. Chiến lược có logic rõ ràng, quản lý rủi ro hoàn chỉnh, mang tính thực tiễn cao. Thông qua tối ưu hóa và điều chỉnh liên tục, có kỳ vọng nâng cao hiệu suất của chiến lược.

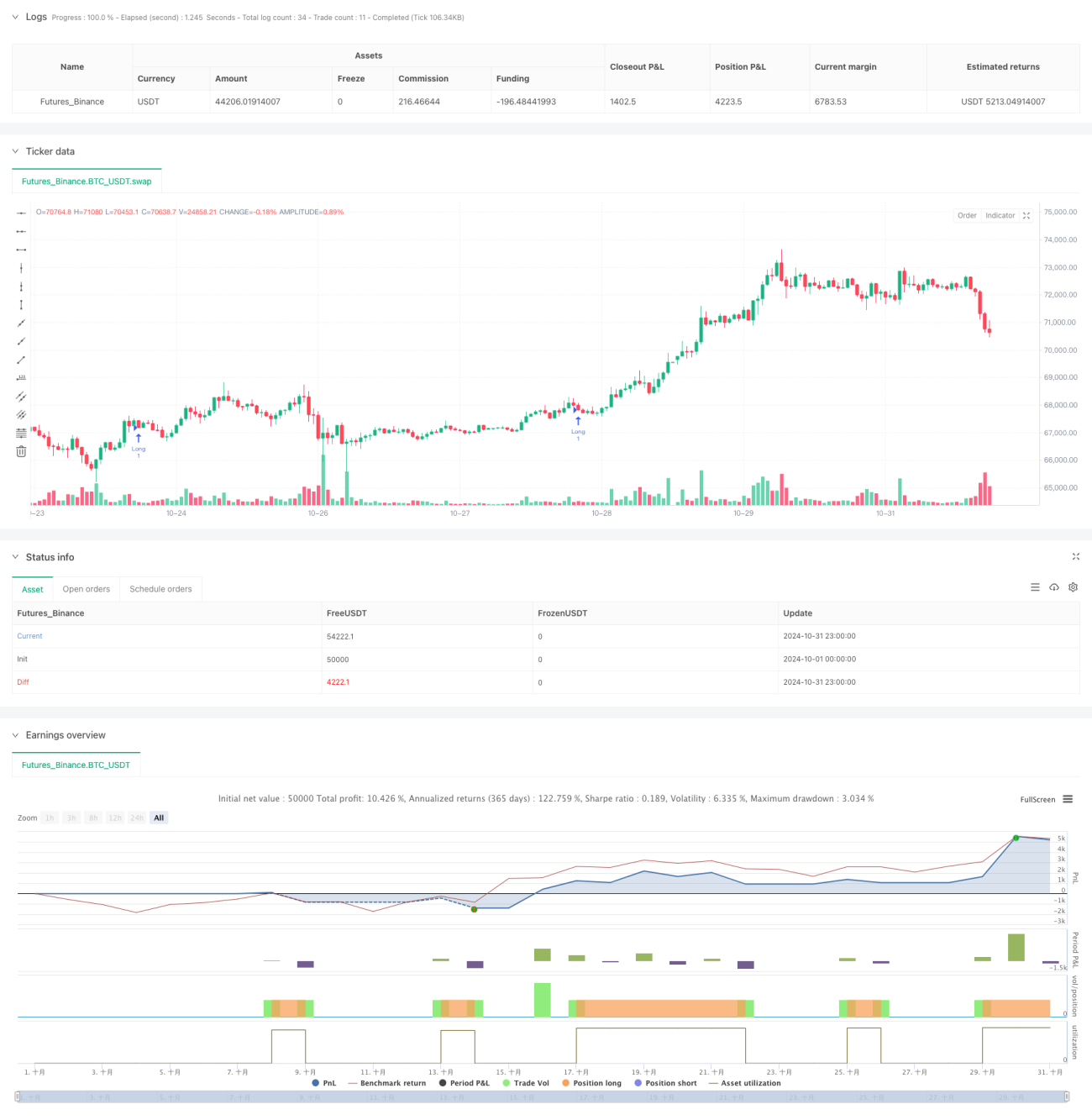

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Post-Open Long Strategy with ATR-based Stop Loss and Take Profit (Separate Alerts)", overlay=true)

// Parametri per Bande di Bollinger ed EMA- 1