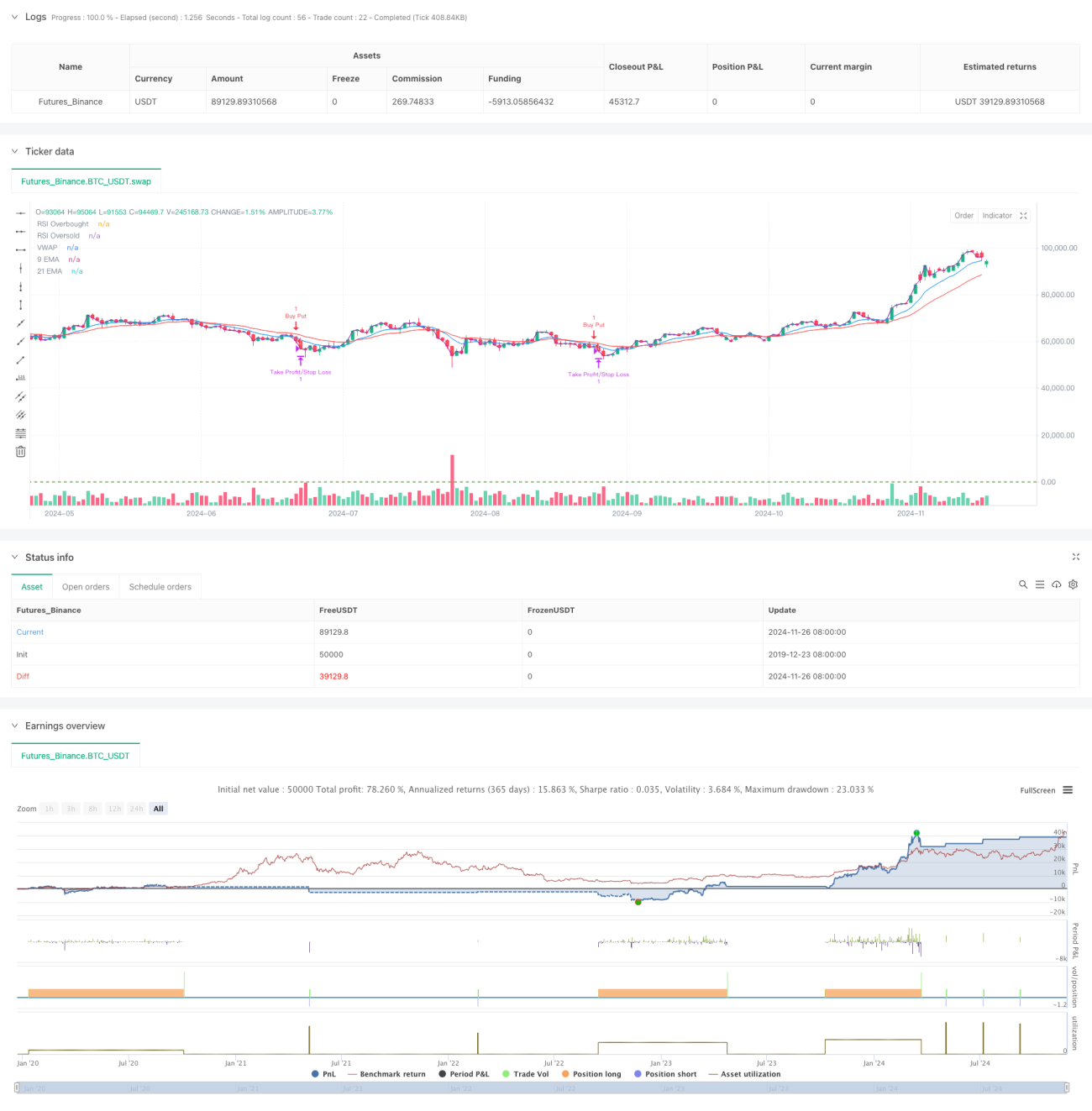

Tổng quan

Chiến lược này là một hệ thống giao dịch tần suất cao dựa trên nhiều chỉ báo kỹ thuật, sử dụng khung thời gian 5 phút, kết hợp hệ thống đường trung bình, chỉ báo động lượng và phân tích khối lượng. Chiến lược điều chỉnh linh hoạt để thích ứng với biến động thị trường, sử dụng xác nhận nhiều tín hiệu nhằm nâng cao độ chính xác và độ tin cậy của giao dịch. Cốt lõi của chiến lược là kết hợp các chỉ báo kỹ thuật đa chiều để bắt kịp xu hướng thị trường ngắn hạn, đồng thời sử dụng cắt lỗ động để kiểm soát rủi ro.

Nguyên lý chiến lược

Chiến lược sử dụng hệ thống hai đường trung bình (EMA 9 chu kỳ và 21 chu kỳ) làm công cụ đánh giá xu hướng chính, kết hợp chỉ báo RSI để xác nhận động lượng. Khi giá nằm trên cả hai đường trung bình và RSI trong khoảng 40–65, hệ thống sẽ tìm kiếm cơ hội mua (long); khi giá nằm dưới cả hai đường trung bình và RSI trong khoảng 35–60, hệ thống sẽ tìm kiếm cơ hội bán (short). Đồng thời, chiến lược đưa vào cơ chế xác nhận khối lượng, yêu cầu khối lượng hiện tại phải lớn hơn 1,2 lần khối lượng trung bình động 20 chu kỳ. Việc sử dụng VWAP còn giúp đảm bảo hướng giao dịch phù hợp với xu hướng chủ đạo trong ngày.

Ưu điểm của chiến lược

- Cơ chế xác nhận nhiều tín hiệu giúp nâng cao đáng kể độ tin cậy của giao dịch.

- Cài đặt chốt lời và cắt lỗ động thích ứng với các điều kiện thị trường khác nhau.

- Sử dụng ngưỡng RSI khá thận trọng, tránh giao dịch ở vùng cực đoan.

- Cơ chế xác nhận khối lượng lọc hiệu quả các tín hiệu giả.

- Việc sử dụng VWAP giúp đảm bảo hướng giao dịch phù hợp với dòng vốn chính.

- Hệ thống đường trung bình phản ứng nhanh thích hợp để bắt kịp các cơ hội thị trường ngắn hạn.

Rủi ro của chiến lược

- Trong thị trường đi ngang dao động có thể tạo ra các tín hiệu giả thường xuyên.

- Các ràng buộc nhiều điều kiện có thể khiến bỏ lỡ một số cơ hội giao dịch.

- Giao dịch tần suất cao có thể phải đối mặt với chi phí giao dịch cao.

- Có thể phản ứng chậm khi thị trường đảo chiều nhanh.

- Yêu cầu cao về tính tức thời của dữ liệu thị trường.

Hướng tối ưu hóa chiến lược

- Đưa vào cơ chế điều chỉnh tham số thích ứng, cho phép chiến lược điều chỉnh linh hoạt các tham số chỉ báo theo trạng thái thị trường.

- Bổ sung module nhận diện môi trường thị trường, áp dụng các chiến lược giao dịch khác nhau trong các điều kiện thị trường khác nhau.

- Tối ưu hóa điều kiện lọc khối lượng, có thể xem xét sử dụng khối lượng tương đối hoặc phân tích profile khối lượng.

- Hoàn thiện cơ chế cắt lỗ, có thể thêm chức năng trailing stop.

- Thêm bộ lọc thời gian giao dịch, tránh các phiên biến động mạnh vào đầu giờ và cuối giờ.

Tổng kết

Chiến lược này thông qua sự kết hợp của nhiều chỉ báo kỹ thuật đã xây dựng một hệ thống giao dịch tương đối hoàn chỉnh. Ưu điểm của chiến lược nằm ở cơ chế xác nhận tín hiệu đa chiều và phương pháp kiểm soát rủi ro động. Mặc dù tồn tại một số rủi ro tiềm ẩn, nhưng thông qua việc tối ưu hóa tham số hợp lý và quản lý rủi ro, chiến lược vẫn có giá trị ứng dụng tốt. Khuyến nghị nhà giao dịch nên tiến hành backtest đầy đủ trước khi sử dụng thực tế và điều chỉnh tham số phù hợp theo tình hình thị trường cụ thể.

- 1