Tổng quan

Chiến lược này là một hệ thống giao dịch thích ứng kết hợp theo dõi xu hướng cổ điển với đường trung bình động kép và quản lý rủi ro động dựa trên ATR. Chiến lược cung cấp hai chế độ giao dịch: Chế độ cơ bản sử dụng giao cắt đường trung bình động kép đơn giản để theo dõi xu hướng, chế độ nâng cao bổ sung bộ lọc xu hướng khung thời gian cao hơn và cơ chế dừng lỗ động dựa trên ATR. Chiến lược cho phép chuyển đổi giữa hai chế độ dễ dàng thông qua menu thả xuống đơn giản, vừa đáp ứng tính dễ sử dụng cho người mới bắt đầu, vừa đáp ứng nhu cầu kiểm soát rủi ro của các nhà giao dịch giàu kinh nghiệm.

Nguyên lý chiến lược

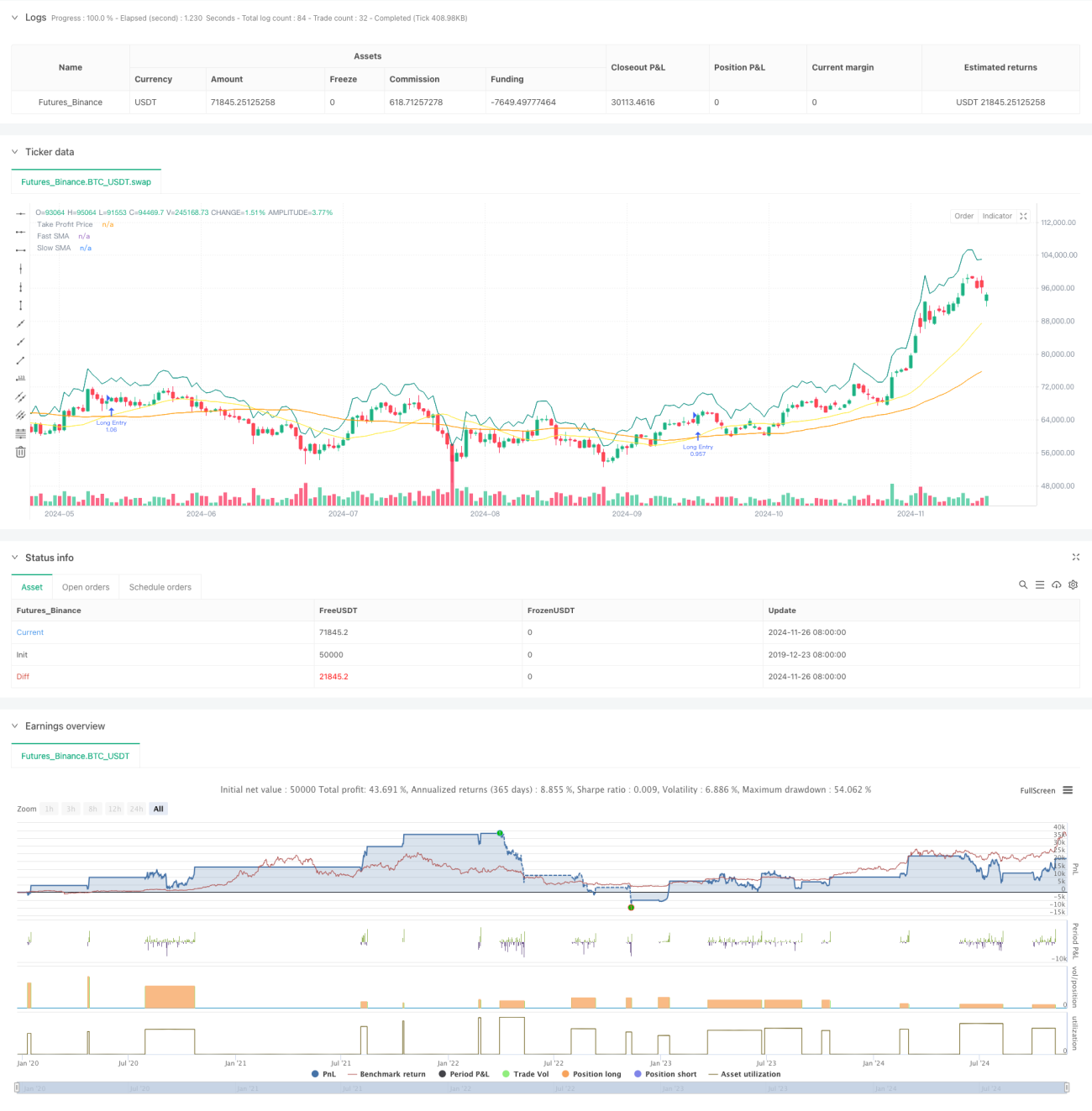

Chiến lược 1 (Chế độ cơ bản) sử dụng hệ thống đường trung bình động kép 21 và 49 ngày. Khi đường trung bình động nhanh cắt lên trên đường trung bình động chậm, tín hiệu mua được tạo ra. Mục tiêu lợi nhuận có thể được đặt dưới dạng phần trăm hoặc số điểm, đồng thời cung cấp chức năng dừng lỗ di động tùy chọn để chốt lợi nhuận. Chiến lược 2 (Chế độ nâng cao) bổ sung bộ lọc xu hướng khung ngày trên cơ sở hệ thống đường trung bình động kép, chỉ cho phép vào lệnh khi giá nằm trên đường trung bình động của khung thời gian cao hơn. Đồng thời, giới thiệu cơ chế dừng lỗ động dựa trên ATR 14 kỳ, khoảng cách dừng lỗ tự động điều chỉnh theo biến động thị trường và cung cấp chức năng chốt lời một phần để bảo vệ lợi nhuận đã đạt được.

Ưu điểm chiến lược

- Chiến lược có tính thích ứng cao, có thể linh hoạt chuyển đổi dựa trên trình độ kinh nghiệm của nhà giao dịch và điều kiện thị trường.

- Phân tích đa khung thời gian trong chế độ nâng cao giúp cải thiện chất lượng tín hiệu.

- Dừng lỗ động ATR có thể thích ứng với các điều kiện biến động thị trường khác nhau.

- Cơ chế chốt lời một phần cân bằng giữa bảo vệ lợi nhuận và duy trì xu hướng.

- Tham số cấu hình linh hoạt, dễ dàng tối ưu hóa dựa trên đặc điểm thị trường khác nhau.

Rủi ro chiến lược

- Hệ thống đường trung bình động kép có thể tạo ra các tín hiệu giả thường xuyên trong thị trường đi ngang.

- Bộ lọc xu hướng có thể gây ra độ trễ tín hiệu, bỏ lỡ một số cơ hội giao dịch.

- Dừng lỗ ATR có thể không kịp thời khi biến động thay đổi đột ngột.

- Chốt lời một phần có thể thoát lệnh quá sớm, ảnh hưởng đến lợi nhuận từ xu hướng lớn.

Hướng tối ưu hóa chiến lược

- Có thể thêm bộ lọc khối lượng và chỉ báo biến động để giảm tín hiệu giả.

- Cân nhắc đưa cơ chế tham số thích ứng động, tự động điều chỉnh chu kỳ đường trung bình động dựa trên trạng thái thị trường.

- Tối ưu hóa chu kỳ tính toán ATR để cân bằng độ nhạy và độ ổn định.

- Thêm mô-đun nhận dạng trạng thái thị trường để tự động chọn chế độ chiến lược tối ưu.

- Giới thiệu thêm các tùy chọn dừng lỗ khác như dừng lỗ theo dõi, dừng lỗ theo thời gian, v.v.

Kết luận

Đây là một hệ thống chiến lược giao dịch được thiết kế hợp lý và đầy đủ chức năng. Bằng cách kết hợp theo dõi xu hướng với đường trung bình động kép và quản lý rủi ro ATR, chiến lược vừa đảm bảo độ tin cậy vừa cung cấp quản lý rủi ro tốt. Thiết kế hai chế độ đáp ứng nhu cầu của các nhà giao dịch ở các cấp độ khác nhau, và cài đặt tham số phong phú cung cấp không gian tối ưu hóa đầy đủ. Khuyến nghị nhà giao dịch bắt đầu với các tham số thận trọng trong giao dịch thực tế, từ từ điều chỉnh và tối ưu hóa để đạt hiệu quả tốt nhất.

- 1