Chiến lược phát hiện khoảng trống giá trị hợp lý nâng cao dựa trên quản lý rủi ro động và chốt lời cố định

Tổng quan

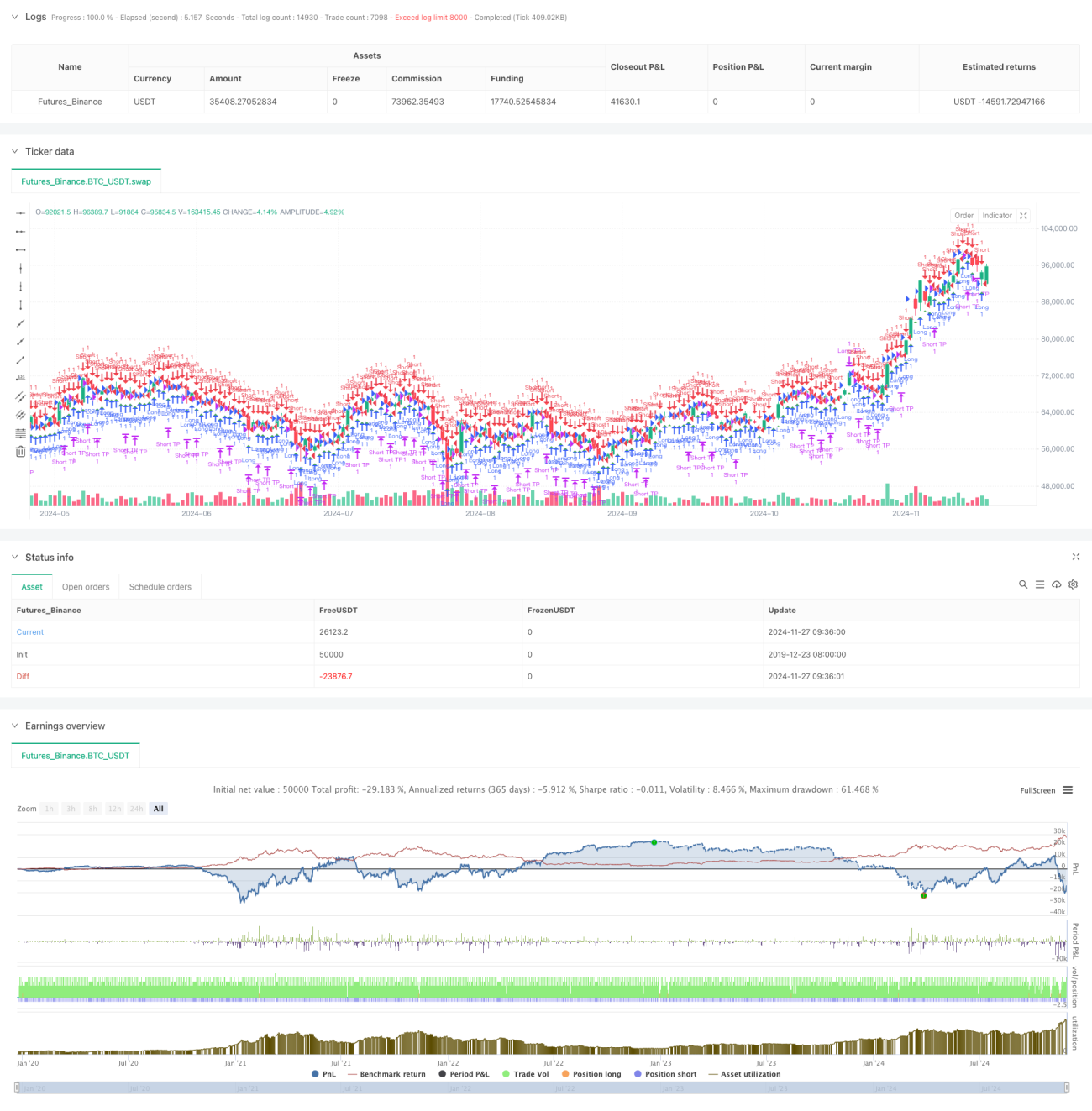

Đây là một chiến lược giao dịch dựa trên khoảng trống giá trị hợp lý (FVG), kết hợp quản lý rủi ro động và mục tiêu lợi nhuận cố định. Chiến lược này hoạt động trên khung thời gian 15 phút, xác định các khoảng trống giá trên thị trường để nắm bắt cơ hội giao dịch tiềm năng. Theo dữ liệu backtest, trong giai đoạn từ tháng 11/2023 đến tháng 8/2024, chiến lược này đạt tỷ suất lợi nhuận ròng 284,40%, thực hiện tổng cộng 153 giao dịch, với tỷ lệ thắng 71,24% và hệ số lợi nhuận 2,422.

Nguyên lý chiến lược

Cốt lõi của chiến lược là xác định khoảng trống giá trị hợp lý thông qua việc theo dõi mối quan hệ giá giữa ba nến liên tiếp. Cụ thể:

- Điều kiện hình thành FVG tăng: Khi giá cao nhất của nến hiện tại thấp hơn giá thấp nhất của hai nến trước đó

- Điều kiện hình thành FVG giảm: Khi giá thấp nhất của nến hiện tại cao hơn giá cao nhất của hai nến trước đó

- Tín hiệu vào lệnh được kiểm soát bởi tham số ngưỡng FVG, chỉ kích hoạt khi kích thước khoảng trống vượt quá một tỷ lệ phần trăm nhất định của giá

- Kiểm soát rủi ro sử dụng tỷ lệ cố định (1%) trên vốn chủ sở hữu tài khoản làm mức cắt lỗ

- Mục tiêu lợi nhuận được đặt ở mức điểm cố định (50 điểm)

Ưu điểm chiến lược

- Quản lý rủi ro khoa học và hợp lý: Sử dụng cắt lỗ theo tỷ lệ vốn chủ sở hữu tài khoản, cho phép kiểm soát rủi ro động

- Quy tắc giao dịch rõ ràng: Sử dụng mục tiêu lợi nhuận cố định, tránh phán đoán chủ quan

- Hiệu suất vượt trội: Tỷ lệ thắng cao và hệ số lợi nhuận cho thấy chiến lược có độ ổn định tốt

- Cách thực hiện đơn giản: Logic mã rõ ràng, dễ hiểu và dễ bảo trì

- Khả năng thích ứng cao: Có thể điều chỉnh tham số để phù hợp với các điều kiện thị trường khác nhau

Rủi ro chiến lược

- Rủi ro biến động thị trường: Trong thị trường biến động cao, mục tiêu lợi nhuận cố định điểm có thể không đủ linh hoạt

- Rủi ro trượt giá: Giao dịch thường xuyên có thể dẫn đến chi phí trượt giá cao

- Phụ thuộc vào tham số: Hiệu suất chiến lược phụ thuộc mạnh vào cài đặt ngưỡng FVG

- Rủi ro phá vỡ giả: Một số tín hiệu FVG có thể là phá vỡ giả, cần thêm chỉ báo xác nhận

- Rủi ro quản lý vốn: Cắt lỗ theo tỷ lệ cố định khi thua lỗ liên tiếp có thể khiến vốn giảm nhanh

Hướng tối ưu hóa chiến lược

- Đưa vào chỉ báo biến động thị trường để điều chỉnh mục tiêu lợi nhuận động

- Thêm bộ lọc xu hướng, tránh giao dịch trong thị trường đi ngang

- Phát triển cơ chế xác nhận đa khung thời gian

- Tối ưu hóa thuật toán quản lý vị thế, đưa vào hệ thống vị thế linh hoạt

- Thêm bộ lọc thời gian giao dịch, tránh các khung giờ biến động cao

- Phát triển hệ thống chấm điểm cường độ tín hiệu, sàng lọc các cơ hội giao dịch chất lượng cao

Tổng kết

Chiến lược này kết hợp lý thuyết khoảng trống giá trị hợp lý và phương pháp quản lý rủi ro khoa học, đã thể hiện hiệu quả giao dịch tốt. Tỷ lệ thắng cao và hệ số lợi nhuận ổn định của chiến lược cho thấy nó có giá trị thực chiến. Thông qua các hướng tối ưu hóa được đề xuất, chiến lược còn có không gian để cải thiện hơn nữa. Khuyến nghị nhà giao dịch nên thực hiện tối ưu hóa tham số và kiểm tra backtest đầy đủ trước khi sử dụng trong giao dịch thực tế.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-28 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Fair Value Gap Strategy with % SL and Fixed TP", overlay=true, initial_capital=500, default_qty_type=strategy.fixed, default_qty_value=1)

// Parameters- 1