Chiến lược sụt giảm thị trường cực đoan dựa trên độ lệch thống kê

Tổng quan

Chiến lược này giao dịch dựa trên các đặc điểm thống kê khi thị trường giảm cực đoan. Thông qua phân tích thống kê mức sụt giảm (drawdown), sử dụng độ lệch chuẩn để đo lường mức độ cực đoan của biến động thị trường, và mua vào khi thị trường giảm vượt quá phạm vi bình thường. Ý tưởng cốt lõi của chiến lược là nắm bắt cơ hội siêu giảm do tâm lý hoảng loạn của thị trường gây ra, xác định cơ hội đầu tư từ hành vi phi lý của thị trường thông qua phương pháp thống kê toán học.

Nguyên lý chiến lược

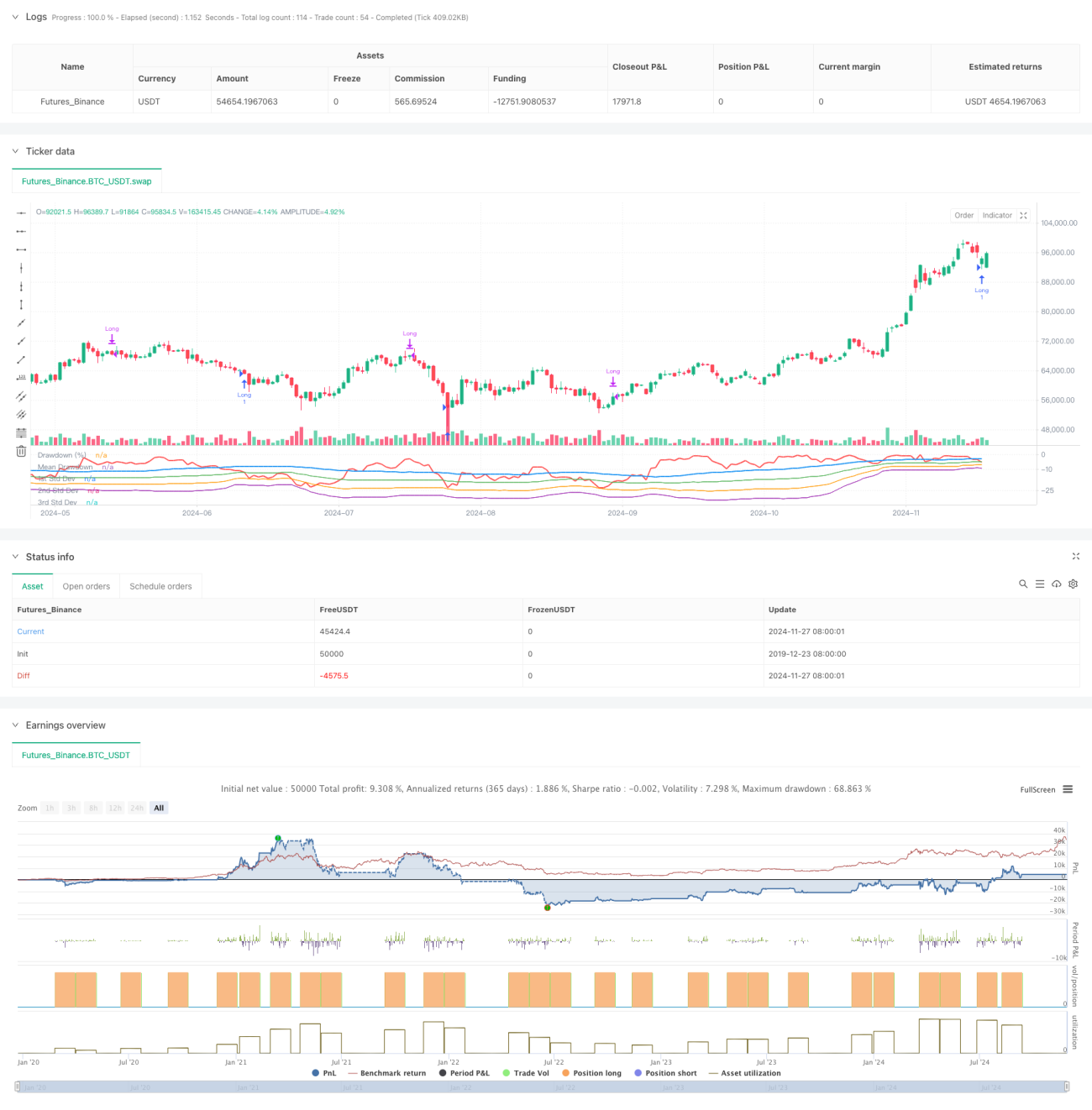

Chiến lược sử dụng cửa sổ thời gian trượt để tính toán mức sụt giảm tối đa của giá và các đặc điểm thống kê của mức sụt giảm. Đầu tiên, tính giá cao nhất trong 50 chu kỳ trước, sau đó tính tỷ lệ phần trăm sụt giảm của giá đóng cửa hiện tại so với giá cao nhất. Tiếp theo, tính giá trị trung bình và độ lệch chuẩn của mức sụt giảm, đặt ngưỡng kích hoạt là -1 lần độ lệch chuẩn. Khi mức sụt giảm của thị trường vượt quá giá trị trung bình trừ đi số lần độ lệch chuẩn đã thiết lập, điều này cho thấy thị trường có thể đã siêu giảm, lúc này vào vị thế mua. Sau 35 chu kỳ nắm giữ, tự động đóng vị thế. Chiến lược cũng vẽ đường cong sụt giảm và các đường mức độ lệch chuẩn một lần, hai lần và ba lần để trực quan đánh giá mức độ siêu giảm của thị trường.

Ưu điểm của chiến lược

- Chiến lược dựa trên nguyên tắc thống kê, có nền tảng lý thuyết vững chắc. Sử dụng độ lệch chuẩn để đo lường mức độ cực đoan của biến động thị trường, phương pháp khách quan và khoa học.

- Chiến lược có thể hiệu quả nắm bắt các cơ hội đầu tư trong giai đoạn thị trường hoảng loạn. Vào lệnh khi thị trường giảm phi lý, phù hợp với triết lý đầu tư giá trị.

- Sử dụng cách đóng vị thế theo chu kỳ cố định, tránh bỏ lỡ cơ hội phục hồi do trailing stop.

- Các tham số của chiến lược có khả năng điều chỉnh cao, có thể linh hoạt thiết lập theo các môi trường thị trường và đặc điểm sản phẩm giao dịch khác nhau.

- Các chỉ số sụt giảm và độ lệch chuẩn được tính toán đơn giản, logic chiến lược rõ ràng, dễ hiểu và dễ thực hiện.

Rủi ro của chiến lược

- Thị trường có thể tiếp tục giảm, dẫn đến việc chiến lược vào lệnh thường xuyên nhưng đều thua lỗ. Khuyến nghị thiết lập giới hạn số lượng vị thế tối đa.

- Đóng vị thế theo chu kỳ cố định có thể bỏ lỡ không gian tăng giá lớn hơn. Có thể xem xét thêm phương pháp đóng vị thế theo dõi xu hướng.

- Đặc điểm thống kê của mức sụt giảm có thể thay đổi theo môi trường thị trường. Khuyến nghị cập nhật định kỳ thiết lập tham số.

- Chiến lược chưa xem xét các thông tin thị trường khác như khối lượng giao dịch. Khuyến nghị kết hợp nhiều chỉ báo để xác nhận chéo.

- Trong môi trường thị trường biến động mạnh, độ lệch chuẩn có thể bị méo mó. Khuyến nghị thiết lập các biện pháp kiểm soát rủi ro.

Hướng tối ưu hóa chiến lược

- Đưa vào chỉ báo khối lượng giao dịch để xác nhận mức độ hoảng loạn của thị trường.

- Thêm chỉ báo xu hướng để tránh vào lệnh thường xuyên trong xu hướng giảm.

- Tối ưu hóa cơ chế đóng vị thế, điều chỉnh thời gian nắm giữ linh hoạt dựa trên diễn biến thị trường.

- Thêm thiết lập cắt lỗ để kiểm soát rủi ro cho từng giao dịch.

- Xem xét sử dụng tham số thích ứng để nâng cao khả năng thích ứng của chiến lược với sự thay đổi của thị trường.

Tổng kết

Chiến lược này nắm bắt cơ hội siêu giảm của thị trường thông qua phương pháp thống kê, có nền tảng lý thuyết tốt và giá trị ứng dụng. Logic chiến lược đơn giản và rõ ràng, các tham số có khả năng điều chỉnh cao, phù hợp để sử dụng làm chiến lược cơ bản để mở rộng và tối ưu hóa. Bằng cách thêm các chỉ báo kỹ thuật khác và các biện pháp kiểm soát rủi ro, có thể cải thiện thêm tính ổn định và khả năng sinh lời của chiến lược. Trong giao dịch thực tế, khuyến nghị kết hợp với môi trường thị trường và đặc điểm sản phẩm giao dịch, thiết lập tham số một cách thận trọng và thực hiện kiểm soát rủi ro tốt.

- 1