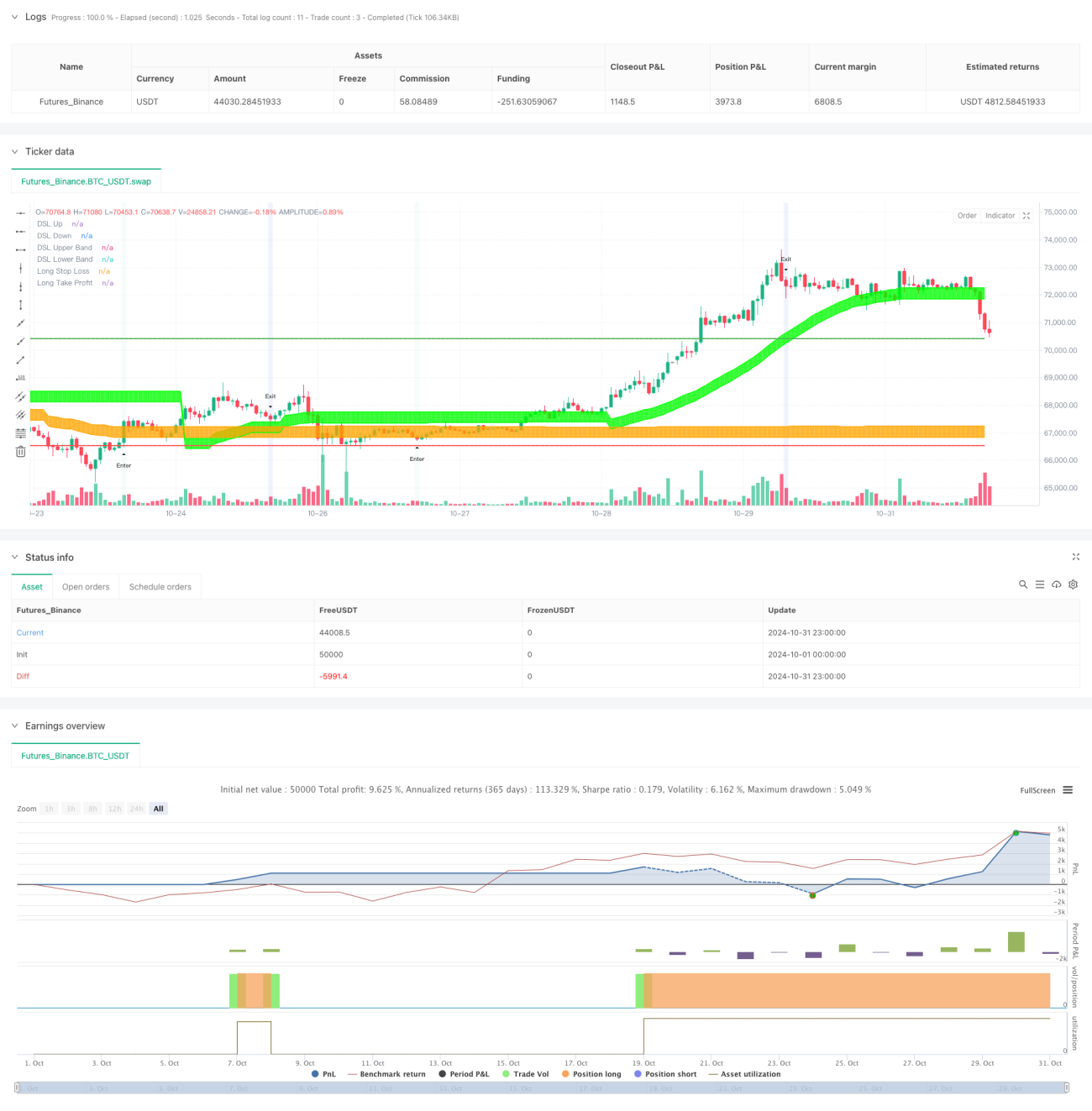

Tổng quan

Chiến lược này là một hệ thống giao dịch tổng hợp kết hợp Đường tín hiệu động (DSL), chỉ báo biến động và động lượng. Thông qua các ngưỡng động và dải biến động thích ứng, chiến lược này nhận diện hiệu quả xu hướng thị trường, sử dụng các chỉ báo động lượng để lọc tín hiệu, từ đó nắm bắt thời điểm giao dịch chính xác. Hệ thống có cơ chế quản lý rủi ro hoàn chỉnh, bao gồm cắt lỗ động và thiết lập mục tiêu lợi nhuận dựa trên tỷ lệ lợi nhuận/rủi ro.

Nguyên lý chiến lược

Logic cốt lõi của chiến lược được xây dựng trên ba thành phần chính:

Đầu tiên là hệ thống đường tín hiệu động, tính toán các đường biên trên và dưới động dựa trên đường trung bình động. Các đường biên này tự động điều chỉnh vị trí dựa trên các đỉnh và đáy gần đây của thị trường, thực hiện theo dõi xu hướng thích ứng. Hệ thống cũng kết hợp chỉ báo ATR để xây dựng các dải biến động động, dùng để xác nhận sức mạnh xu hướng và đặt vị trí cắt lỗ.

Thứ hai là hệ thống phân tích động lượng, sử dụng chỉ báo RSI được tối ưu hóa bằng Đường trung bình động hàm mũ không trễ (ZLEMA). Bằng cách áp dụng khái niệm đường tín hiệu động cho RSI, hệ thống có thể xác định chính xác hơn vùng quá mua/quá bán và tạo ra tín hiệu đột phá động lượng.

Thứ ba là cơ chế tích hợp tín hiệu. Tín hiệu giao dịch chỉ được kích hoạt khi đồng thời thỏa mãn cả hai điều kiện: xác nhận xu hướng và đột phá động lượng. Vào lệnh mua (long) yêu cầu giá phá vỡ dải trên và duy trì phía trên dải, đồng thời RSI phá vỡ đường tín hiệu động bên dưới. Tín hiệu bán (short) yêu cầu các điều kiện ngược lại đồng thời thỏa mãn.

Ưu điểm chiến lược

- Tính thích ứng cao: Các đường tín hiệu động và dải biến động tự động điều chỉnh theo điều kiện thị trường, giúp chiến lược thích nghi với các môi trường thị trường khác nhau.

- Lọc tín hiệu giả: Yêu cầu xác nhận kép từ xu hướng và động lượng giúp giảm đáng kể xác suất tín hiệu giả.

- Quản lý rủi ro hoàn chỉnh: Tích hợp cắt lỗ động dựa trên ATR và thiết lập mục tiêu lợi nhuận dựa trên tỷ lệ lợi nhuận/rủi ro, thực hiện kiểm soát rủi ro có hệ thống.

- Linh hoạt và có thể tùy chỉnh: Các tham số của chiến lược có thể được tối ưu hóa và điều chỉnh cho các thị trường và khung thời gian khác nhau.

Rủi ro chiến lược

- Rủi ro đảo chiều xu hướng: Trong các đảo chiều thị trường mạnh, việc điều chỉnh của các đường tín hiệu động có thể không kịp thời, dẫn đến sụt giảm lớn.

- Rủi ro thị trường dao động: Trong thị trường dao động trong biên độ, các đột phá thường xuyên có thể dẫn đến nhiều lần cắt lỗ.

- Nhạy cảm với tham số: Hiệu suất chiến lược khá nhạy cảm với việc thiết lập tham số, tham số không phù hợp có thể ảnh hưởng đến kết quả chiến lược.

Hướng tối ưu hóa chiến lược

- Nhận diện môi trường thị trường: Có thể thêm cơ chế phân loại môi trường thị trường, sử dụng các tham số khác nhau trong các trạng thái thị trường khác nhau.

- Tối ưu hóa tham số động: Giới thiệu cơ chế điều chỉnh tham số thích ứng, tự động tối ưu hóa các tham số đường tín hiệu và dải biến động dựa trên biến động thị trường.

- Phân tích đa khung thời gian: Tích hợp tín hiệu từ nhiều khung thời gian để tăng độ tin cậy của quyết định giao dịch.

- Thích ứng biến động: Điều chỉnh mức cắt lỗ và tỷ lệ lợi nhuận/rủi ro trong các giai đoạn biến động cao để cải thiện lợi nhuận điều chỉnh theo rủi ro của chiến lược.

Tổng kết

Chiến lược này thông qua sự kết hợp sáng tạo giữa đường tín hiệu động và chỉ báo động lượng, đã thực hiện việc nắm bắt hiệu quả xu hướng thị trường. Cơ chế quản lý rủi ro hoàn chỉnh và hệ thống lọc tín hiệu giúp nó có giá trị ứng dụng thực tiễn mạnh mẽ. Thông qua tối ưu hóa liên tục và điều chỉnh tham số, chiến lược dự kiến có thể duy trì hiệu suất ổn định trong các môi trường thị trường khác nhau. Mặc dù có một số điểm rủi ro nhất định, nhưng thông qua việc thiết lập tham số hợp lý và các biện pháp kiểm soát rủi ro, những rủi ro này có thể được kiểm soát.

- 1