Chiến lược thích ứng hỗn hợp đường trung bình động kép và sức mạnh tương đối

Tổng quan

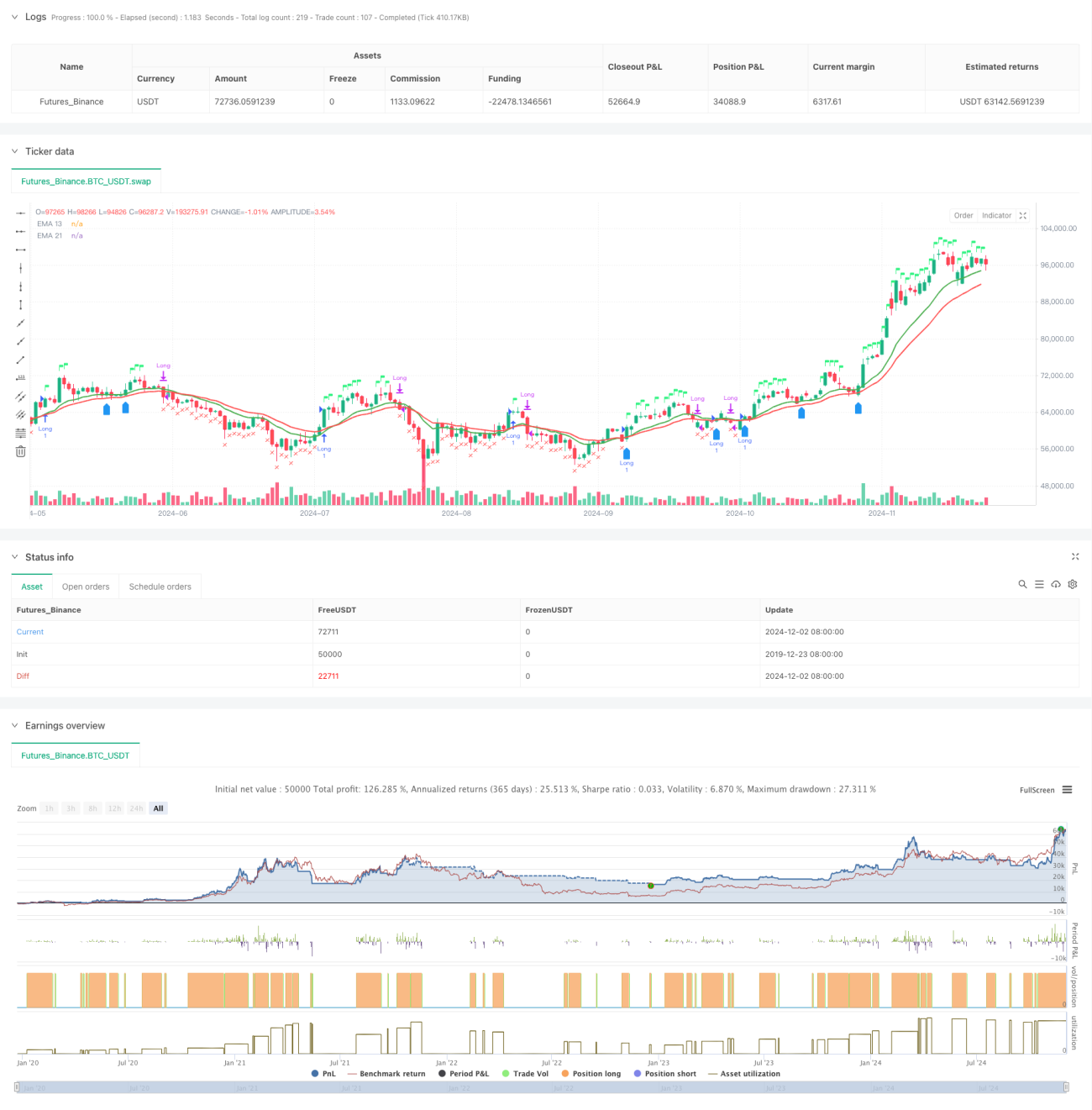

Chiến lược này là một hệ thống giao dịch tổng hợp kết hợp hệ thống đường trung bình động kép, chỉ số sức mạnh tương đối (RSI) và phân tích sức mạnh tương đối (RS). Chiến lược xác nhận xu hướng thông qua giao cắt của đường trung bình động hàm mũ (EMA) 13 ngày và 21 ngày, đồng thời kết hợp RSI và giá trị RS so với chỉ số chuẩn để xác nhận tín hiệu giao dịch, tạo ra cơ chế ra quyết định giao dịch đa chiều. Chiến lược này cũng bao gồm cơ chế kiểm soát rủi ro dựa trên đỉnh 52 tuần và đánh giá điều kiện tái nhập lệnh.

Nguyên lý chiến lược

Chiến lược sử dụng cơ chế xác nhận tín hiệu đa tầng:

- Tín hiệu vào lệnh cần đồng thời thỏa mãn các điều kiện sau:

- EMA13 cắt lên trên EMA21 hoặc giá cao hơn EMA13

- RSI lớn hơn 60

- Sức mạnh tương đối (RS) dương

- Điều kiện thoát lệnh bao gồm:

- Giá phá vỡ xuống dưới EMA21

- RSI dưới 50

- RS chuyển sang âm

- Điều kiện tái nhập lệnh:

- Giá cắt lên trên EMA13 và EMA13 lớn hơn EMA21

- RS duy trì dương

- Hoặc giá phá vỡ đỉnh tuần trước

Ưu điểm chiến lược

- Cơ chế xác nhận tín hiệu đa tầng giảm rủi ro phá vỡ giả

- Kết hợp phân tích sức mạnh tương đối, sàng lọc hiệu quả các mã mạnh

- Áp dụng cơ chế điều chỉnh chu kỳ thời gian thích ứng

- Có hệ thống kiểm soát rủi ro hoàn chỉnh

- Bao gồm cơ chế tái nhập lệnh thông minh

- Cung cấp trực quan hóa trạng thái giao dịch theo thời gian thực

Rủi ro chiến lược

- Thị trường đi ngang có thể tạo ra giao dịch thường xuyên

- Phụ thuộc vào nhiều chỉ báo có thể dẫn đến độ trễ tín hiệu

- Ngưỡng RSI cố định có thể không phù hợp với mọi môi trường thị trường

- Tính toán sức mạnh tương đối phụ thuộc vào độ chính xác của chỉ số chuẩn

- Mức cắt lỗ đỉnh 52 tuần có thể quá lỏng lẻo

Hướng tối ưu hóa chiến lược

- Đưa vào ngưỡng RSI thích ứng

- Tối ưu hóa logic đánh giá điều kiện tái nhập lệnh

- Bổ sung phân tích khối lượng giao dịch

- Hoàn thiện cơ chế chốt lời cắt lỗ

- Thêm bộ lọc biến động

- Tối ưu hóa chu kỳ tính toán sức mạnh tương đối

Tổng kết

Chiến lược này xây dựng một hệ thống giao dịch toàn diện bằng cách kết hợp phân tích kỹ thuật và phân tích sức mạnh tương đối. Cơ chế xác nhận tín hiệu đa tầng và hệ thống kiểm soát rủi ro khiến nó có tính ứng dụng cao. Thông qua các hướng tối ưu hóa được đề xuất, chiến lược còn có không gian cải thiện thêm. Việc triển khai thành công chiến lược đòi hỏi nhà giao dịch phải có hiểu biết sâu sắc về thị trường và điều chỉnh tham số phù hợp với đặc điểm của từng loại tài sản giao dịch cụ thể.

- 1