Chiến lược tăng cường xu hướng định lượng nhiều lớp AO

Tổng quan

Chiến lược này là một hệ thống giao dịch đa tầng dựa trên động lực và theo dõi xu hướng. Nó xác định nhiều cơ hội giao dịch có xác suất cao bằng cách kết hợp chỉ số Williams Shark, chỉ số Williams Split, chỉ số Magic Shock (AO) và chỉ số Moving Average (EMA). Chiến lược sử dụng cơ chế đầu tư phân tầng vốn, tăng dần khi xu hướng tăng lên, có thể giữ tối đa 5 vị trí cùng một lúc, mỗi vị trí sử dụng 10% vốn.

Nguyên tắc chiến lược

Chiến lược sử dụng nhiều cơ chế lọc để đảm bảo tính chính xác của hướng giao dịch. Đầu tiên, đánh giá xu hướng dài hạn thông qua EMA, chỉ tìm kiếm nhiều cơ hội khi giá nằm trên EMA. Tiếp theo, đánh giá xu hướng ngắn hạn thông qua sự kết hợp của chỉ số Williams Shark và Split, xác nhận xu hướng tăng lên khi đột phá Split trên xảy ra trên đường răng của cá mập. Cuối cùng, sau khi xác nhận xu hướng, chiến lược tìm kiếm chỉ số AO để thực hiện nhiều tín hiệu "bông" như là thời điểm cụ thể.

Lợi thế chiến lược

- Cơ chế lọc nhiều lớp có hiệu quả trong việc giảm nhiễu tín hiệu giả

- Khoa học quản lý tài chính, sử dụng phương pháp gia tăng dần dần

- Tính năng theo xu hướng cho phép nó nắm bắt các xu hướng lớn

- Không có điểm dừng cố định, nhưng đánh giá xu hướng kết thúc bằng các chỉ số kỹ thuật

- Hệ thống có khả năng cấu hình tốt, dễ dàng điều chỉnh các tham số theo các điều kiện thị trường khác nhau

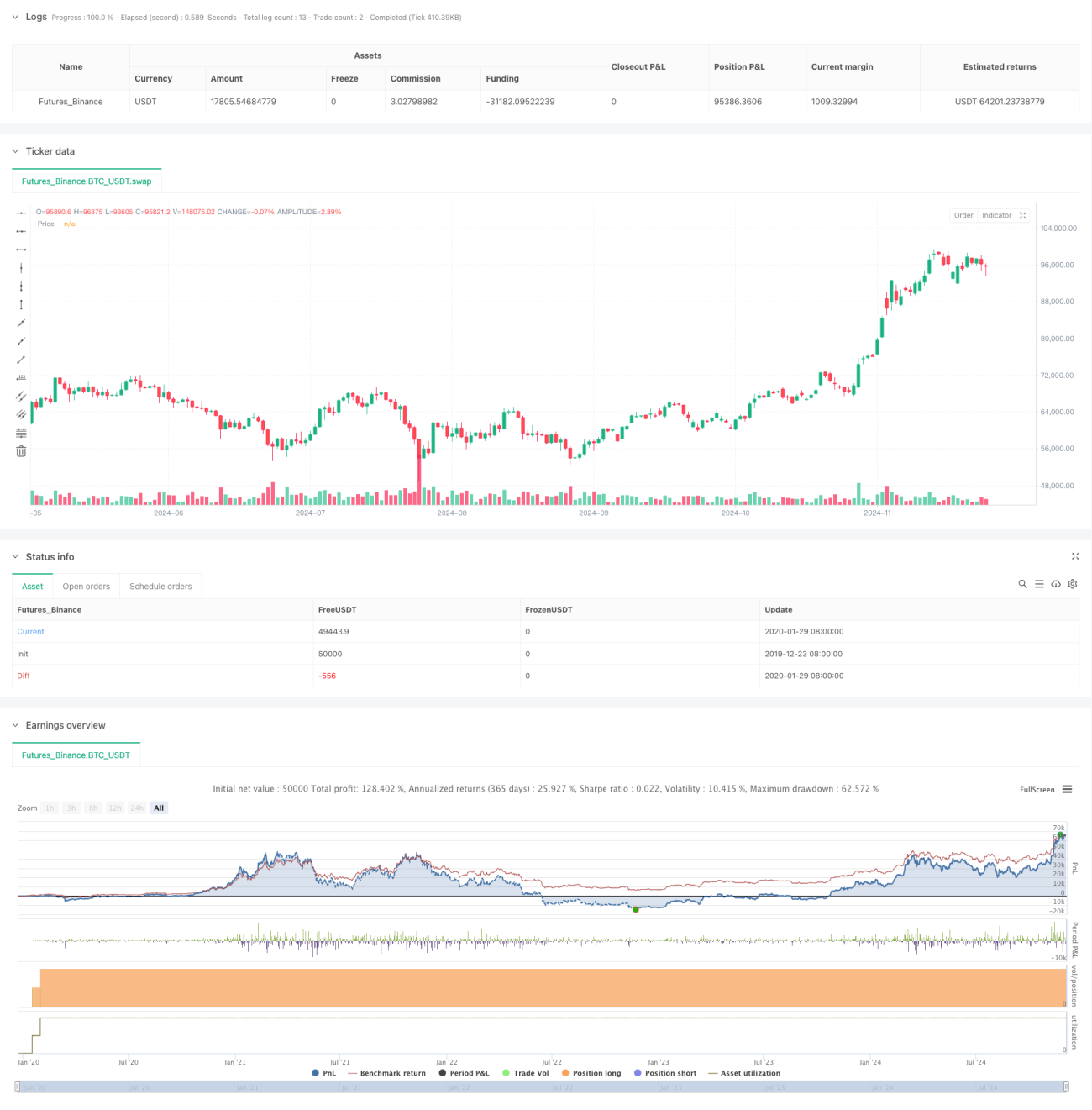

- Kết quả khảo sát cho thấy có yếu tố lợi nhuận tốt và lợi nhuận trung bình.

Rủi ro chiến lược

- Các tín hiệu giả liên tục có thể xuất hiện trong thị trường bất ổn

- Một sự thoái lui lớn hơn có thể xảy ra khi xu hướng đảo ngược

- Điều kiện lọc nhiều lần có thể làm mất cơ hội giao dịch

- Trong quản lý tài chính, việc gia tăng liên tục có thể mang lại rủi ro khi biến động mạnh

- Lựa chọn tham số EMA có ảnh hưởng lớn đến hiệu suất chiến lược

Để giảm bớt những rủi ro này, chúng tôi khuyên bạn nên:

- Tối ưu hóa các tham số trong các môi trường thị trường khác nhau

- Xem xét thêm bộ lọc tỷ lệ dao động

- Thiết lập các điều kiện gia tăng nghiêm ngặt hơn

- Thiết lập giới hạn rút tối đa

Hướng tối ưu hóa chiến lược

- Tham gia ATR để lọc tỷ lệ dao động

- Thêm phân tích khối lượng giao dịch để cải thiện độ tin cậy của tín hiệu

- Phát triển cơ chế thích ứng cho các tham số động

- Cải thiện hệ thống ngăn chặn, thu lợi nhuận đúng lúc khi xu hướng giảm

- Thêm mô-đun nhận dạng trạng thái thị trường, sử dụng các tham số khác nhau trong các môi trường thị trường khác nhau

Tóm tắt

Đây là một chiến lược theo dõi xu hướng được thiết kế hợp lý, thông qua việc sử dụng nhiều chỉ số kỹ thuật kết hợp, trong khi đảm bảo tính an toàn, đạt được hiệu suất lợi nhuận tốt. Điểm sáng tạo của chiến lược là cơ chế xác nhận xu hướng nhiều cấp và phương pháp quản lý tiền theo cấp độ. Mặc dù có một số nơi cần tối ưu hóa, nhưng nói chung là một hệ thống giao dịch đáng thử.

- 1