Tổng quan

Chiến lược này là một hệ thống giao dịch tiên tiến dựa trên phân tích điểm pivot, xác định các điểm ngoặt tiềm năng trong xu hướng thông qua việc nhận diện các điểm đảo chiều then chốt trên thị trường. Chiến lược áp dụng phương pháp "pivot của pivot" sáng tạo, kết hợp với chỉ số biến động ATR để quản lý vị thế, tạo thành một hệ thống giao dịch hoàn chỉnh. Chiến lược này phù hợp với nhiều thị trường và có thể tối ưu hóa tham số dựa trên đặc điểm của từng thị trường.

Nguyên lý chiến lược

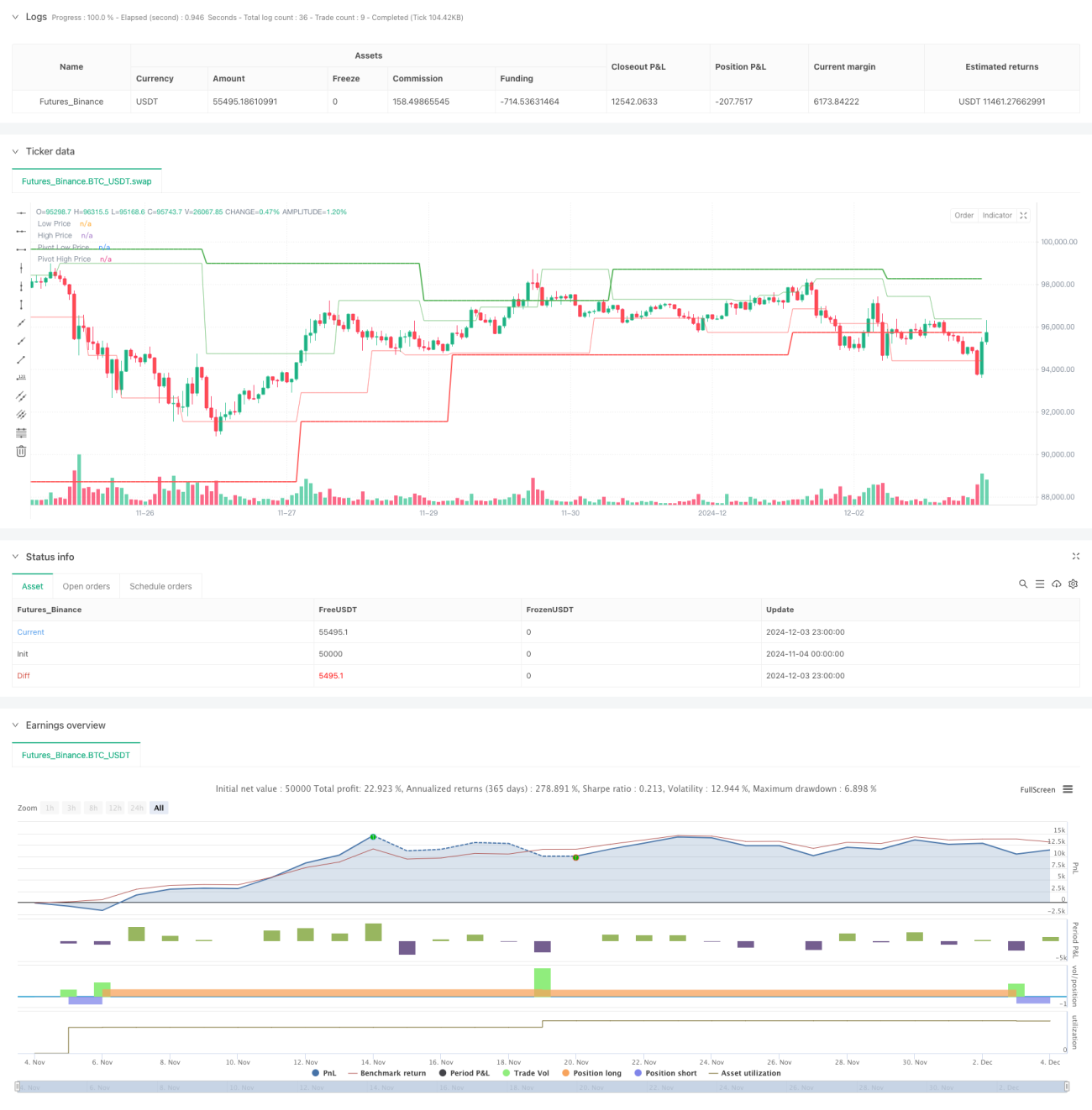

Cốt lõi của chiến lược là xác định cơ hội đảo chiều thị trường thông qua phân tích điểm pivot hai cấp độ. Cấp độ đầu tiên là các điểm cao/thấp cơ bản, cấp độ thứ hai là các điểm ngoặt đáng kể được lọc từ các điểm pivot cấp độ một. Khi giá phá vỡ các mức then chốt này, hệ thống sẽ tạo ra tín hiệu giao dịch. Đồng thời, chiến lược sử dụng chỉ số ATR để đo lường biến động thị trường, từ đó xác định vị trí cắt lỗ, chốt lời và quy mô vị thế.

Ưu điểm chiến lược

- Tính thích ứng cao: Chiến lược có thể thích ứng với các môi trường thị trường khác nhau thông qua việc điều chỉnh tham số phù hợp với các mức độ biến động khác nhau.

- Quản lý rủi ro toàn diện: Sử dụng ATR để thiết lập cắt lỗ động, tự động điều chỉnh biện pháp bảo vệ theo biến động thị trường.

- Xác nhận đa cấp: Thông qua phân tích điểm pivot hai cấp, giảm thiểu rủi ro phá vỡ giả.

- Quản lý vị thế linh hoạt: Điều chỉnh linh hoạt quy mô vị thế dựa trên quy mô tài khoản và biến động thị trường.

- Quy tắc vào lệnh rõ ràng: Có cơ chế xác nhận tín hiệu rõ ràng, giảm thiểu phán đoán chủ quan.

Rủi ro chiến lược

- Rủi ro trượt giá: Có thể gặp trượt giá lớn trong thị trường biến động mạnh.

- Rủi ro phá vỡ giả: Thị trường dao động có thể tạo ra tín hiệu sai.

- Rủi ro đòn bẩy quá mức: Sử dụng đòn bẩy không phù hợp có thể dẫn đến thua lỗ nghiêm trọng.

- Rủi ro tối ưu hóa tham số: Tối ưu hóa quá mức có thể dẫn đến quá khớp (overfitting).

Hướng tối ưu hóa chiến lược

- Lọc tín hiệu: Có thể thêm bộ lọc xu hướng, chỉ giao dịch theo hướng của xu hướng chính.

- Tham số động: Tự động điều chỉnh tham số điểm pivot dựa trên trạng thái thị trường.

- Khung thời gian đa dạng: Tăng cường xác nhận đa khung thời gian để nâng cao độ chính xác.

- Cắt lỗ thông minh: Phát triển chiến lược cắt lỗ thông minh hơn, như cắt lỗ bám theo (trailing stop).

- Kiểm soát rủi ro: Bổ sung thêm các biện pháp kiểm soát rủi ro, như phân tích tương quan.

Tổng kết

Đây là một chiến lược giao dịch đảo chiều xu hướng được thiết kế hoàn chỉnh, xây dựng một hệ thống giao dịch vững chắc thông qua phân tích điểm pivot hai cấp và quản lý biến động ATR. Ưu điểm của chiến lược nằm ở tính thích ứng cao và quản lý rủi ro toàn diện, nhưng nhà giao dịch vẫn cần thận trọng khi sử dụng đòn bẩy và liên tục tối ưu hóa tham số. Thông qua các hướng tối ưu hóa được đề xuất, chiến lược còn có tiềm năng cải thiện. Chiến lược này phù hợp cho các nhà giao dịch ưa thích sự ổn định, là một hệ thống giao dịch đáng để nghiên cứu và thực hành chuyên sâu.

/*backtest

start: 2024-11-04 00:00:00

end: 2024-12-04 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Pivot of Pivot Reversal Strategy [MAD]", shorttitle="PoP Reversal Strategy", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=3)

// Inputs with Tooltips- 1